Millimeter Wave Technology Market Summary

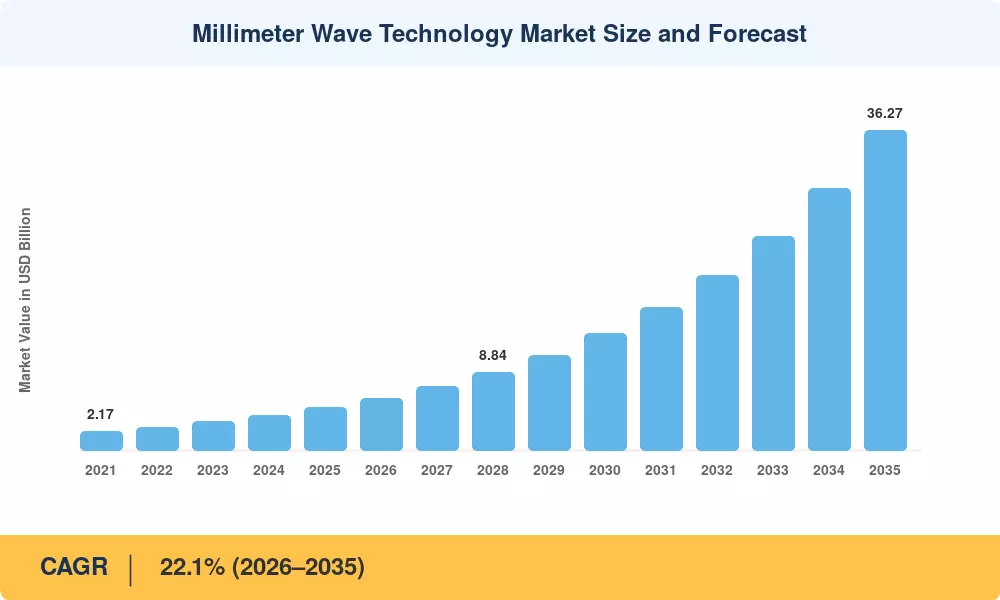

The Millimeter Wave Technology Market reached an estimated USD 4.83 billion in 2025 and is projected to grow from USD 6.02 billion in 2026 to USD 36.27 billion by 2035, registering a CAGR of 22.1% during the forecast period. Two converging forces sustain this trajectory: aggressive 5G mid-band and high-band spectrum auctions across 35+ countries and a parallel push from defense ministries allocating over USD 6.8 billion annually to next-generation radar procurement [1]. The combination of commercial wireless densification and military sensing modernization has created a dual-track capital expenditure cycle rarely seen in RF component markets.

Legacy microwave backhaul links below 15 GHz are gradually being replaced with mmWave point-to-point systems with 10X throughput gain at similar deployment cost. The U.S. CHIPS and Science Act has invested about USD 2.4 billion in compound semiconductor production, including gallium-nitride-on-silicon-carbide wafer lines, which are integral for high-frequency power amplifiers [2]. Meanwhile, European defense agencies are co-investing with telecom incumbents to dual-purpose 60 GHz and 77 GHz hardware originally built for civilian broadband into battlefield communication and vehicular radar platforms.

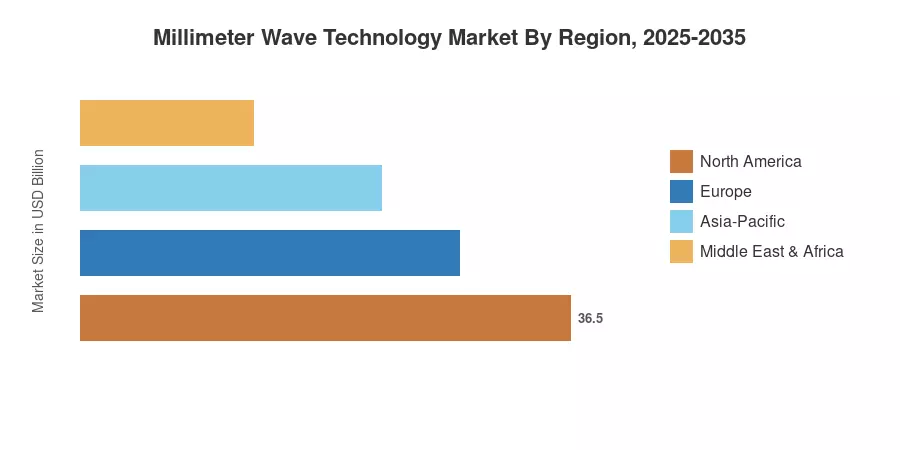

Asia-Pacific is estimated to be the largest Millimeter Wave Technology Market with a share of around 44.8% of the revenue in 2025. This is mainly due to the deployment of over 3.8 million 5G base stations in China and early commercial 28 GHz rollouts in South Korea [3]. The second is North America with a share of around 28.5%, supported by FCC spectrum easing and CHIPS Act financing for semiconductors. Europe is the second fastest growing mature economy, with Horizon Europe research expenditures inside the EU supporting the development of sub-THz components. The Millimeter Wave Technology Market is at the nexus of wireless evolution and national security investment as early 6G research initiatives build up over the decade.

Key Report Takeaways

• By Component

- Antennas and Transceivers accounted for approximately 34.8% of the Millimeter Wave Technology Market revenue in 2025, reflecting sustained demand for phased-array front-end modules in base-station and satellite terminals.

- Imaging Sensors are forecast to expand at a 27.1% CAGR through the study period, fueled by adoption in airport security screening and non-invasive medical diagnostics.

• By Licensing Model

- The Fully/Partly Licensed segment held an estimated 83.5% share of the Millimeter Wave Technology Market in 2025, underscoring operator preference for interference-managed spectrum.

• By Frequency Band

- The 95–300 GHz band is projected to grow at a 23.9% CAGR as sub-terahertz research and high-resolution imaging gain traction.

• By Application

- Telecom Infrastructure captured roughly 48.9% of the Millimeter Wave Technology Market revenue in 2025, driven by small-cell backhaul and fixed wireless access build-outs.

- Automotive ADAS and V2X represent the fastest-growing application segment at a 28.3% CAGR through 2035.

• By Region

- Asia-Pacific occupied an estimated 44.8% share of the Millimeter Wave Technology Market in 2025.

- North America contributed approximately 28.5% of global revenue, supported by spectrum auctions and semiconductor investment incentives.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a triangulated methodology combining bottom-up component shipment volumes, top-down spectrum investment trackers, and validated operator capital-expenditure disclosures across 48 countries. Historical figures reflect audited revenue from RF front-end module vendors, antenna OEMs, and system integrators. At the same time, forecast values incorporate announced spectrum roadmaps, defense procurement pipelines, and automotive OEM design-win timelines.