Mining Explosives Market Summary

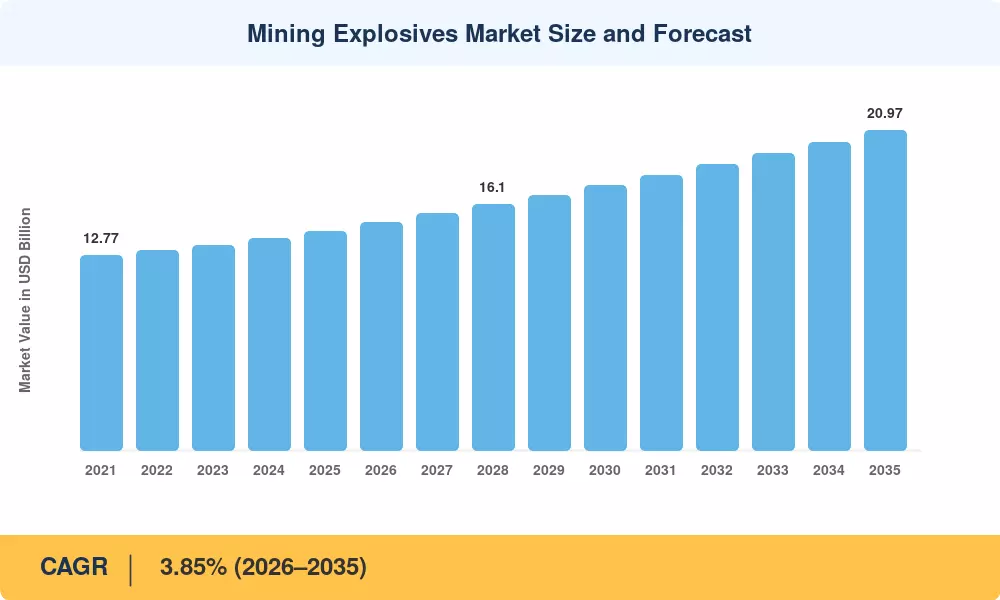

The mining explosives market reached USD 14.38 billion in 2025 and is projected to grow from USD 14.93 billion in 2026 to USD 20.97 billion by 2035, registering a CAGR of 3.85% during the forecast period (2026–2035). Two converging forces drive this trajectory: governments worldwide are accelerating critical-mineral extraction programs to supply lithium, cobalt, and rare-earth elements needed for battery gigafactories, while simultaneously committing over USD 1.2 trillion to infrastructure renewal programs that require large-scale quarrying [1]. These policy catalysts create durable demand for commercial blasting products across both surface and underground operations.

Technology is reshaping how operators consume explosives. Conventional shock-tube and fuse-based initiation is giving way to electronic detonator systems that offer millisecond-level timing precision, reducing ground vibration by up to 40% and improving fragmentation consistency [2]. Concurrently, mine-site emulsion plants are replacing pre-packaged cartridge supply chains, enabling operators to manufacture sensitized product at the bench and cut logistics costs by an estimated 15–20% per blast cycle [3]. Several tier-one producers have invested over USD 500 million collectively since 2022 in digital blast-design platforms that integrate drill-pattern data, geology models, and real-time detonation analytics.

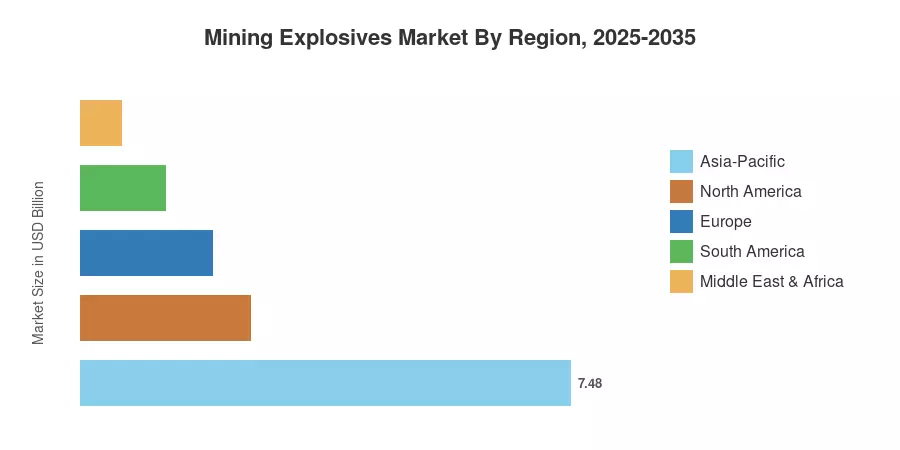

Asia-Pacific dominates the Mining Explosives Market with roughly 52% of global value, anchored by China's thermal-coal output and India's expanding limestone-quarrying sector. The Middle East & Africa region is the fastest-growing geography, posting a projected CAGR of 4.31%, propelled by Saudi Arabia's Vision 2030 mining diversification and accelerating critical-mineral exploration across sub-Saharan Africa. North America holds the second-largest share at approximately 18%, supported by copper and gold expansions in Nevada and British Columbia. As decarbonization agendas intensify demand for transition metals, the Mining Explosives Market is poised for sustained mid-single-digit growth through 2035.

Key Report Takeaways

• By Explosive Type

- Bulk explosives commanded approximately 69% of the Mining Explosives Market share in 2025, driven by large-scale open-pit operations favoring emulsion-based products.

- Packaged explosives are forecast to advance at a 4.25% CAGR between 2026 and 2035, supported by growth in narrow-vein underground mining.

• By Initiation System

- Electronic detonators held roughly 42% of the initiation-system segment in 2025, reflecting operators' shift toward precision timing.

- Non-electric initiation systems remain the volume leader but face share erosion as regulatory vibration limits tighten globally.

• By Application

- Coal mining accounted for approximately 62% of the Mining Explosives Market in 2025, though its share is expected to plateau as thermal-coal output declines in OECD nations.

- Quarry and construction aggregates are set to grow at a 4.37% CAGR through 2035, fueled by global infrastructure spending.

• By Region

- Asia-Pacific held about 52% of the global Mining Explosives Market value in 2025.

- The Middle East & Africa region is expected to grow at a 4.31% CAGR through 2035.

Mining Explosives Market Size and Forecast (2021–2035)

Market Research Future's market-size estimates combine primary interviews with explosive manufacturers, distributors, and mine operators alongside secondary data from national mining statistics bureaus, import-export databases, and published company revenues. Historical figures (2021–2024) reflect actual reported shipments; the base year (2025) is estimated from trailing-twelve-month data, and the forecast (2026–2035) applies a compound methodology validated against regional production indices.