Mobile Accessories Market Summary

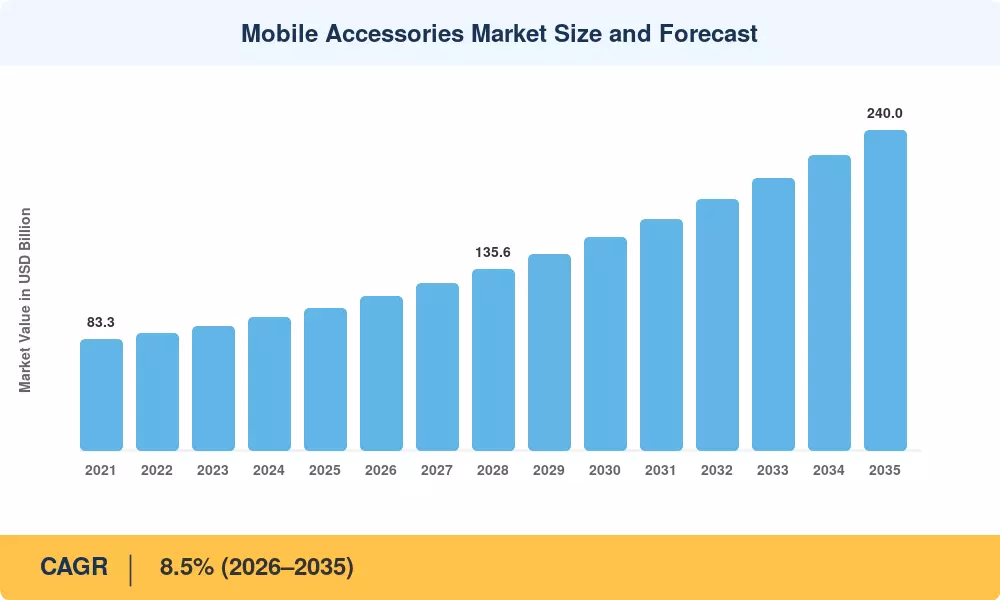

The Mobile Accessories Market reached an estimated USD 106.20 Billion in 2025 and is projected to climb from USD 115.20 Billion in 2026 to USD 240.00 Billion by 2035, expanding at a CAGR of 8.5% during the forecast period. Two forces are converging to accelerate spending: the European Union's universal USB-C charging mandate—effective since late 2024—has collapsed connector fragmentation and emboldened consumers to invest in higher-value accessories without fear of obsolescence, while smartphone installed bases exceeding 5 billion units globally have decoupled accessory demand from handset upgrade cycles [1][2].

A sweeping technology transition is reshaping the Mobile Accessories Market from the component level up. Legacy copper-coil chargers and passive protective cases are giving way to gallium nitride (GaN) power adapters that deliver 65 W in packages smaller than a matchbox, Qi2 magnetic alignment systems that eliminate the guesswork of wireless charging, and AI-enabled earbuds that offer real-time language translation. GaN charger shipments alone surpassed 200 million units in 2024, and global investment in next-generation accessory silicon exceeded USD 3.8 Billion across venture and corporate R&D channels [3][4].

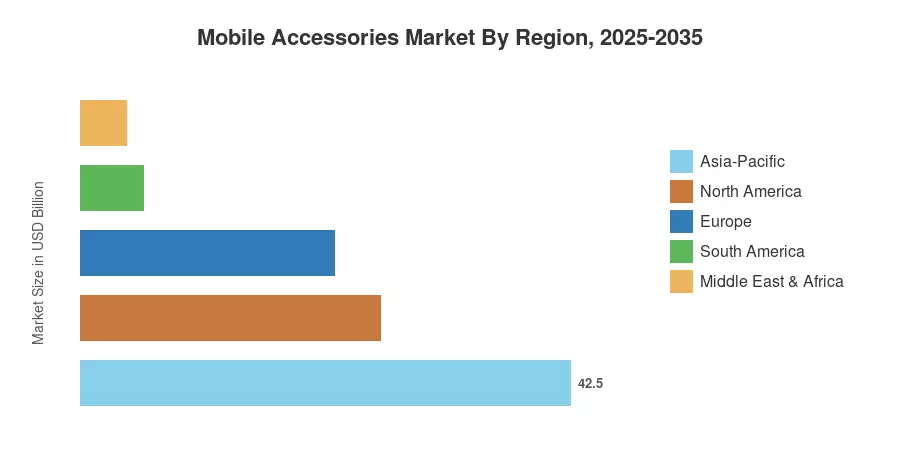

Asia-Pacific commands roughly 42.5% of the Mobile Accessories Market, anchored by China's manufacturing density and India's surging first-time smartphone adoption. The Middle East & Africa region is the fastest-growing geography, forecast to register a CAGR of approximately 8.4% through 2035, driven by near-universal smartphone penetration in Gulf Cooperation Council states. North America remains the second-largest market, contributing about 26.0% of global revenue on the strength of premium pricing and ecosystem-led purchasing. As 5G rollouts mature and wearable integration deepens, the Mobile Accessories Market is set for a sustained upward trajectory well into the next decade.

Key Report Takeaways

• By Product Type

- Protective cases accounted for approximately 28.2% of Mobile Accessories Market revenue in 2025, reflecting persistent demand for drop-proof and antimicrobial designs.

- Wireless chargers are expected to register a CAGR of 7.5% through 2035 as Qi2 adoption accelerates across OEM ecosystems.

• By Distribution Channel

- Online retail captured roughly 57.9% of Mobile Accessories Market sales in 2025, benefiting from direct-to-consumer models that bypass traditional margin drag.

- Offline retail continues to anchor experiential purchasing, particularly in premium-tier accessories priced above USD 51.

• By Region

- Asia-Pacific led the Mobile Accessories Market with a 42.5% share in 2025, supported by concentrated manufacturing and rising domestic consumption.

- The Middle East & Africa is poised for the highest regional CAGR at 8.4% through 2035.

- North America held the second-largest share at 26.0%, driven by ecosystem lock-in and premium price points.

Mobile Accessories Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from trade-association shipment data, customs filings, and company revenue disclosures, while the forecast model combines top-down macroeconomic inputs (smartphone installed base, per-capita accessory spending) with bottom-up SKU-level pricing and channel-mix analysis. All figures are expressed in USD Billion at constant 2025 exchange rates.