Molecular Diagnostics Market Summary

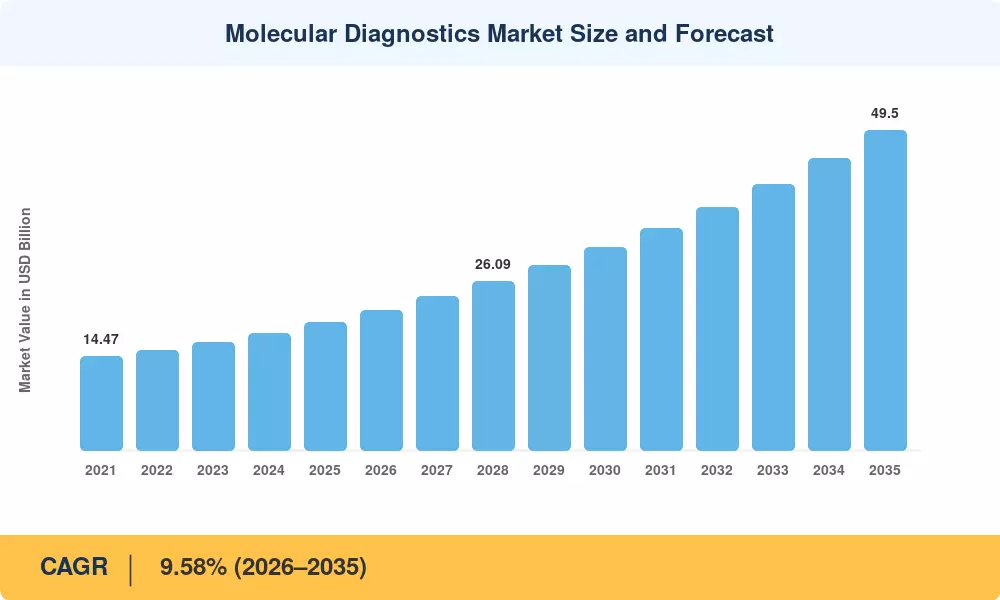

The Global Molecular Diagnostics Market size was valued at USD 19.82 Billion in 2025, and the market is projected to grow from USD 21.72 Billion in 2026 to USD 49.50 Billion by 2035, registering a CAGR of 9.58% during the forecast period 2026–2035. This trajectory is anchored in two converging forces: the expansion of reimbursement frameworks for genomic profiling in oncology and the establishment of clearer regulatory pathways for laboratory-developed tests under the FDA's proposed rule finalized in 2024 [1]. Together, these policy moves are pulling precision medicine out of the research setting and embedding it in routine clinical workflows.

A sweeping technology shift underpins this growth. Legacy culture-based pathogen identification and single-analyte immunoassays are steadily giving way to multiplex syndromic panels and rapid sequencing platforms. Whole-genome sequencing costs have dropped below USD 200 per sample, prompting the FDA to issue breakthrough device designations for several rapid-turnaround platforms [2]. Pharmaceutical companies are investing heavily in vertical integration, building in-house genomic services divisions that feed companion diagnostic pipelines directly into their drug-development programs.

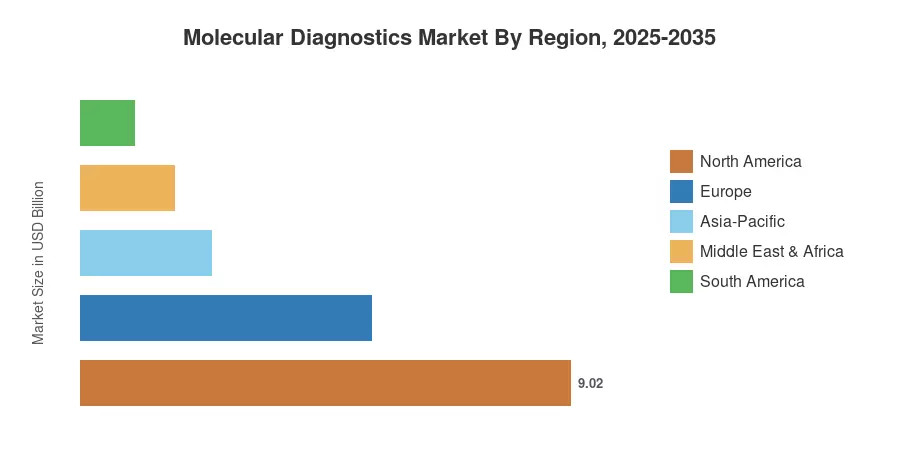

North America commands roughly 45.50% of the Molecular Diagnostics Market, buoyed by payer coverage mandates and a dense network of reference laboratories. Asia-Pacific is the fastest-growing region, with a projected CAGR of 12.21%, driven by government-led screening initiatives in China and India. Europe holds the second-largest share at approximately 27%, though the EU's In Vitro Diagnostic Regulation (IVDR) is compressing margins for smaller manufacturers and consolidating demand around integrated platforms [3]. The decade ahead will hinge on how quickly decentralized testing models reach retail clinics and resource-limited settings worldwide.

Key Report Takeaways

• By Technology

- Polymerase chain reaction captured a 46.27% share of the Molecular Diagnostics Market in 2025, reinforcing its position as the dominant testing platform across clinical laboratories.

- Next-generation sequencing is anticipated to grow at a 12.49% CAGR through 2035, driven by falling per-run costs and expanding oncology panels.

• By Application

- Infectious disease testing accounted for 64.21% of total revenue in 2025, reflecting sustained demand for respiratory and sexually transmitted infection panels.

- Oncology applications are projected to expand at a 10.93% CAGR, fueled by liquid biopsy adoption and companion diagnostic mandates from regulators.

• By Region

- North America led the Molecular Diagnostics Market with a 45.50% revenue share in 2025, supported by broad commercial payer reimbursement for genomic tests.

- The Asia-Pacific region is expected to post the highest CAGR of 12.21% through 2035 as national health programs in China and India scale molecular screening infrastructure.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on primary interviews with laboratory directors, procurement leads at hospital networks, and published regulatory filings, triangulated against company revenue disclosures and trade-association datasets. Historical figures reflect reported revenues; forecast figures apply a bottom-up build by technology segment and region, calibrated to macro indicators including healthcare expenditure growth and diagnostic test-volume trends.