Nitric Acid Market Summary

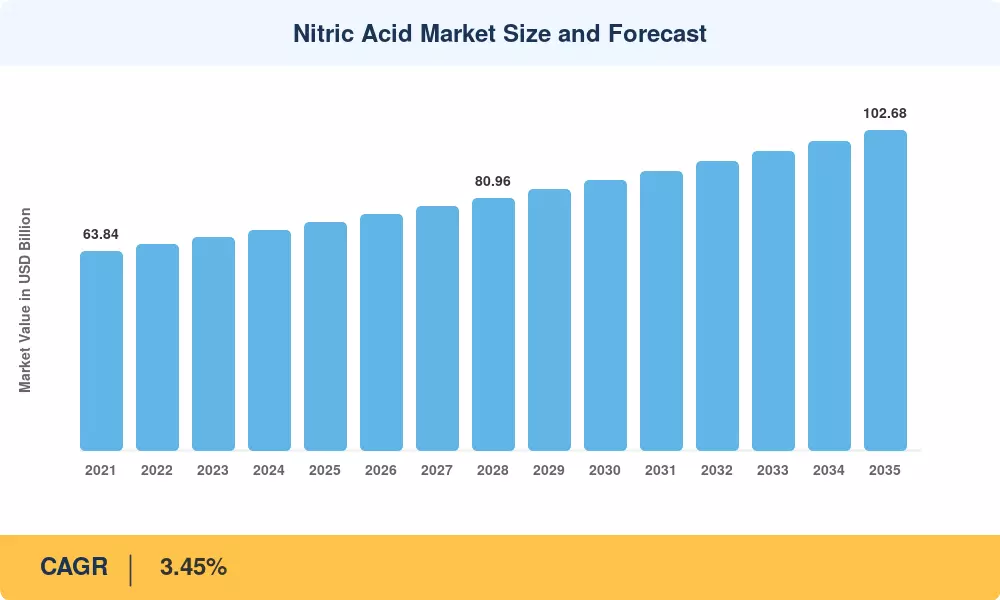

The Nitric Acid Market reached an estimated 73.12 million tons in 2025 and is projected to grow from 75.48 million tons in 2026 to 102.68 million tons by 2035, registering a CAGR of 3.45% during the forecast period. This expansion is underpinned by two converging forces: rising global fertilizer consumption driven by food-security mandates across South and Southeast Asia, and the European Union's Carbon Border Adjustment Mechanism (CBAM), which is redirecting capital toward low-carbon ammonium nitrate production facilities within EU borders [2]. Together, these catalysts are reshaping both the volume trajectory and the geographic investment mix of the Nitric Acid Market.

Production technique changes from generation to generation. Old single-pressure Ostwald facilities, many of which were built in the 1980s, are being replaced with dual-pressure and medium-pressure designs that reduce nitrogen oxide emissions by up to 90% and improve energy recovery. The European Commission’s Industrial Emissions Directive amendment (2024) requires all new acid plants to meet best-available-technique (BAT) standards by 2028, driving an estimated EUR 4.2 billion in total retrofit and greenfield investment throughout the continent [3]. At the same time, new-build plants are increasingly adopting catalytic abatement technologies based on tertiary N₂O breakdown, reducing the carbon intensity of each tonne of acid produced.

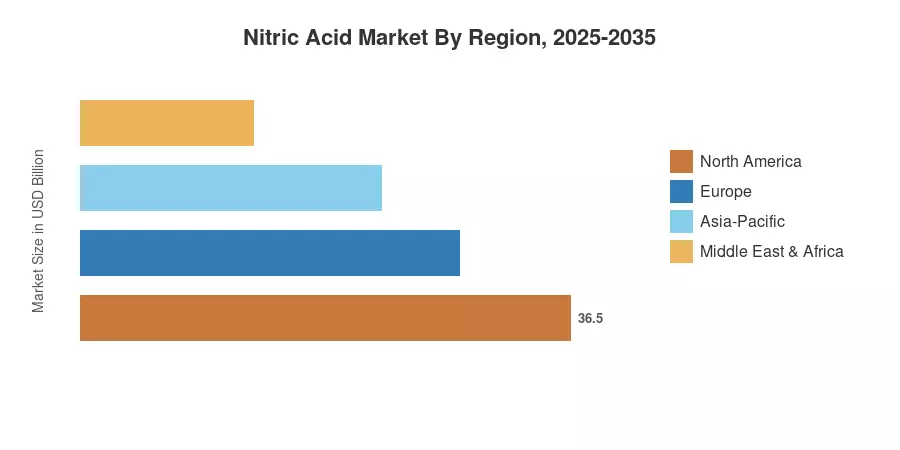

Asia-Pacific dominates the Nitric Acid Market and is the leading consuming region, holding over 63% of the global volume. The area is also the fastest expanding, with a CAGR of 3.49% through 2035, supported by India’s expansion of urea subsidies and China’s ongoing change from coal-based to natural-gas-based ammonia feedstock. Europe is the second largest market with a share of around 19%, followed by North America. With the tightening of decarbonization rules and the growing demand for agricultural chemical ingredients, the competition will be increasingly in favor of those producers who can ensure low-cost feedstock availability or have confirmed low-carbon certifications.

Key Report Takeaways

• By Concentration

- Weak nitric acid captured 62% of the global Nitric Acid Market volume share in 2025, reflecting entrenched demand from fertilizer chemicals blending operations

- Concentrated nitric acid is forecast to expand at a 3.92% CAGR through 2035, driven by rising polyamide 6,6 and industrial oxidizing agents applications

- Fuming and red fuming grades account for less than 4% of total volume but serve critical aerospace and explosive manufacturing chemicals requirements

• By End-User Industry

- Fertilizers dominated the Nitric Acid Market in 2025 with a 74% revenue share, anchored by ammonium nitrate production for calcium ammonium nitrate (CAN) blends

- Explosives registered the fastest segment growth at a 4.25% CAGR, fueled by mining expansion across Asia-Pacific and Latin America

- Chemical manufacturing accounted for USD 3.8 billion in 2025, with inorganic acid compounds and metal treatment chemicals driving specialty demand

• By Regional

- Asia-Pacific accounted for 63% of the Nitric Acid Market size in 2025 and leads growth through 2035

- Europe is advancing at a 2.91% CAGR, shaped by CBAM-driven domestic production shifts

- North America contributed approximately 12% of global volume in 2025

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up production capacity audits across 42 countries with top-down demand modeling calibrated against trade-flow databases (UN Comtrade, ITC TradeMap) and validated through primary interviews with 85+ industry participants. Historical volumes (2021–2024) rely on published plant-level output data; forecast volumes (2026–2035) apply regression-adjusted demand elasticities for fertilizer chemicals, explosive manufacturing chemicals, and chemical processing acids end uses.