Optical Satellite Communication Market Summary

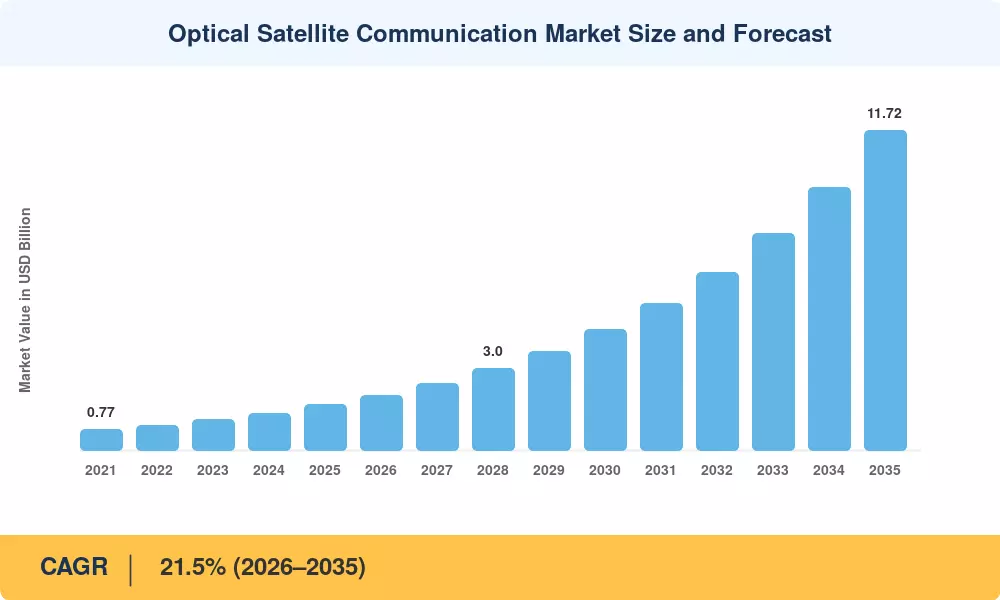

The optical satellite communication market was valued at USD 1.67 Billion in 2025 and is projected to grow from USD 2.03 Billion in 2026 to USD 11.72 Billion by 2035, registering a CAGR of 21.5% during the forecast period (2026–2035). This expansion is anchored in escalating demand for high-bandwidth optical satellite systems capable of moving terabits of data per second across Low-Earth-Orbit mega-constellations. NASA's Space Communications and Navigation program allocated over USD 650 million through 2025 for laser-based satellite data relay demonstrations, while the European Space Agency committed EUR 1.9 billion to its ARTES ScyLight program for secure inter-satellite optical link development[2].

Legacy radio-frequency transponders—once the backbone of satellite data relay—are rapidly giving way to free-space optical laser communication terminals that deliver 10–100× higher throughput at a fraction of the mass and power budget. The U.S. Space Development Agency's Tranche 2 procurement alone calls for more than 200 laser-equipped satellites, injecting roughly USD 2.4 billion into optical ground station technology and flight-qualified transceivers between 2024 and 2028 [3]. Private constellation operators such as SpaceX and Amazon's Project Kuiper are simultaneously embedding inter-satellite optical link hardware across thousands of spacecraft.

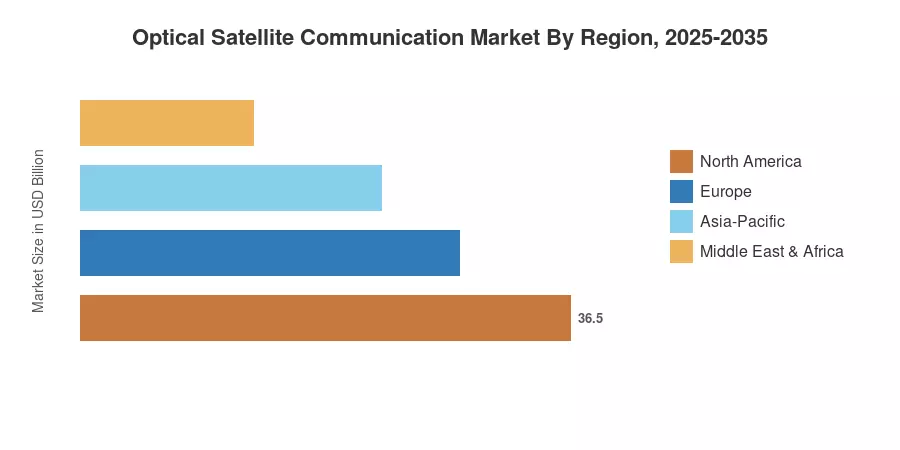

North America commands a 24.6% share of the optical satellite communication market, driven by Pentagon-backed investment and Silicon Valley venture capital. Asia-Pacific is the fastest-growing region at a 23.2% CAGR, fueled by China's 100 Gbps space-to-ground laser tests and India's newly funded optical payload roadmap. Europe holds the second-largest share at approximately 23.1%, with Airbus-Tesat's EDRS constellation serving as a commercial proof point. The decade ahead will see free-space optical laser communication shift from a technology differentiator to a baseline requirement for any satellite operator bidding on sovereign or commercial capacity.

Key Report Takeaways

• By Component

- Optical transceiver terminals captured a 29.2% revenue share of the optical satellite communication market in 2024, reflecting defense procurement momentum.

- Beam-steering assemblies are projected to register a 24.6% CAGR through 2035, as adaptive optics become critical for high-bandwidth optical satellite downlinks.

- Optical ground station technology segments are expanding across allied nations, investing in sovereign laser receive sites.

• By Orbit & Payload

- LEO platforms accounted for 63.8% of the optical satellite communication market share in 2024, driven by mega-constellation rollouts.

- Medium satellites represent the fastest payload segment at a 23.7% CAGR, reflecting laser-based satellite data relay integration on 500-kg class buses.

• By End-User

- Government and defense programs commanded a 52.6% share in 2024, underscoring security-driven demand for inter-satellite optical link infrastructure.

• By Region

- Asia-Pacific is forecasted to expand at a 23.2% CAGR, making it the fastest-growing geography in the optical satellite communication market.

Market Size and Forecast (2021–2035)

Market sizing combines top-down revenue analysis of satellite prime contractor filings with bottom-up terminal shipment tracking across 14 countries. Historical figures (2021–2024) rely on disclosed contract values and launch manifests; forecast projections apply MRFR's proprietary demand model calibrated to constellation build-out timelines and spectrum-migration schedules.