Oral Thin Film Drugs Market Summary

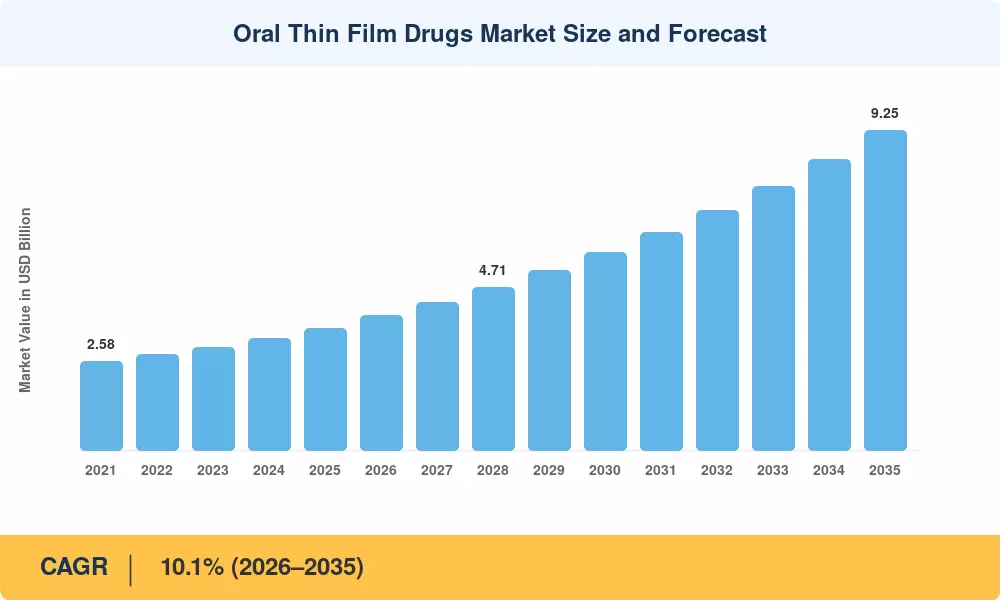

The Oral Thin Film Drugs Market size was valued at USD 3.53 Billion in 2025, and the market is projected to grow from USD 3.89 Billion in 2026 to USD 9.25 Billion by 2035, registering a CAGR of 10.1% during the forecast period 2026–2035. Two catalysts are accelerating this trajectory: the FDA's increasing receptiveness toward 505(b)(2) reformulation pathways and a global push by healthcare systems to reduce medication non-adherence costs, which the World Health Organization estimates exceed USD 100 Billion annually across chronic disease populations [1].

A fundamental shift is underway in how active pharmaceutical ingredients reach systemic circulation. Traditional tablets and capsules — long the default oral dosage form — are steadily giving way to polymer-based thin-film platforms that dissolve on mucosal tissue within seconds. Continuous manufacturing lines using advanced polymer extrusion and precision coating have cut unit production costs by an estimated 18–22% since 2021, enabling both branded and generic manufacturers to pursue thin-film reformulations across a widening therapeutic range. The U.S. National Institutes of Health allocated over USD 45 Million in grants during 2023–2024 specifically for novel oral delivery research, further underscoring institutional confidence in this technology class [3].

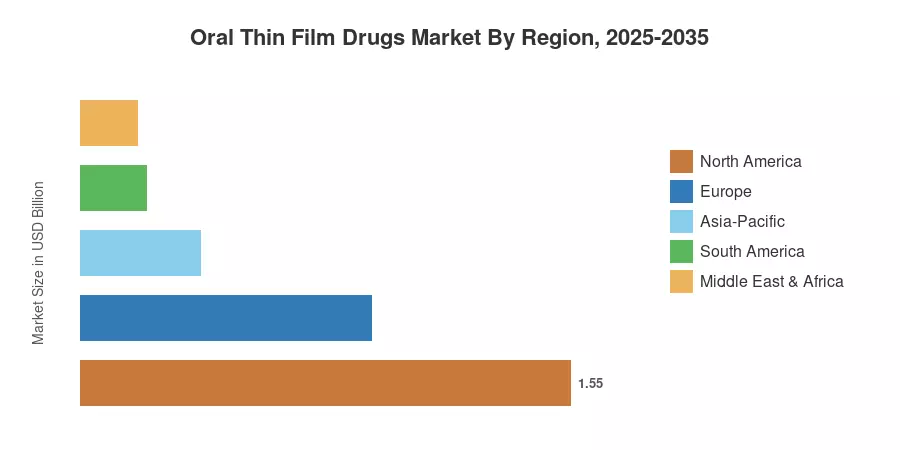

North America commands the largest share of the Oral Thin Film Drugs Market at roughly 44% of 2025 revenue, driven by a mature regulatory framework and high opioid-dependence treatment volumes. Asia-Pacific is the fastest-growing region with a projected CAGR of 10.9% through 2035, fueled by expanding generic pharmaceutical manufacturing in India and rising chronic disease burdens across China and Southeast Asia. Europe holds the second-largest position at approximately a 26% share, supported by EMA harmonization of film-based drug approval pathways. The coming decade will see the Oral Thin Film Drugs Market extend into oncology supportive care, CNS disorders, and pediatric-specific formulations as polymer science continues to advance.

Key Report Takeaways

• By Product

- Sublingual films accounted for roughly 58% of Oral Thin Film Drugs Market revenue in 2025, anchored by high-volume opioid-dependence therapies.

- Buccal films are forecast to register the fastest growth at a 12.0% CAGR through 2035, driven by emerging migraine and antiemetic indications.

• By Disease Indication

- Opioid dependence represented approximately 42% of market share in 2025, reflecting entrenched prescribing patterns and reimbursement coverage.

- Migraine therapies are projected to expand at a 12.8% CAGR, as new film-based triptans gain formulary placement.

• By Technology

- Solvent-casting technology held about a 58% share in 2025, remaining the workhorse manufacturing method.

- 3-D printing-based film production is anticipated to grow at a 12.2% CAGR, enabling personalized dosing.

• By Distribution Channel

- Retail pharmacies captured approximately 44% of the Oral Thin Film Drugs Market in 2025.

- Online pharmacies are expected to post a 13.1% CAGR as direct-to-patient models gain traction.

• By Region

- North America led with a 44% share of the Oral Thin Film Drugs Market

- While Asia-Pacific is on pace for a 10.9% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market Research Future's estimates combine primary interviews with pharmaceutical manufacturers, analysis of FDA and EMA approval pipelines, prescription volume tracking databases, and proprietary demand modeling. Historical figures (2021–2024) reflect audited revenue from leading contract development and manufacturing organizations (CDMOs), while forecast values (2026–2035) apply a calibrated growth algorithm accounting for pipeline approvals, patent expirations, and regional policy shifts.