Orphan Drugs Market Summary

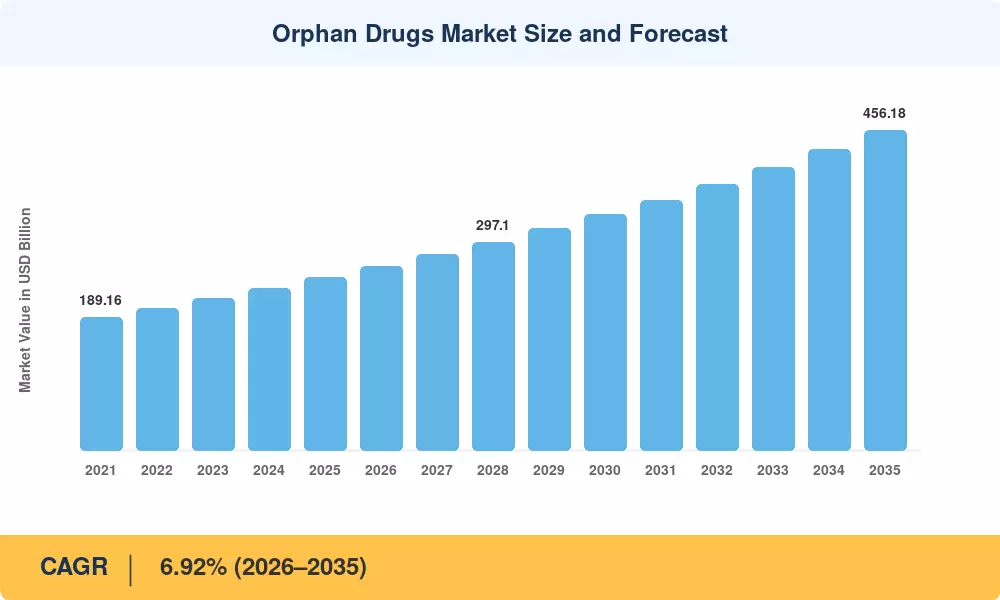

The Orphan Drugs Market reached an estimated USD 247.22 billion in 2025, positioning it as one of the pharmaceutical sector's most resilient growth corridors. Starting from a projected USD 263.10 billion in 2026, the Orphan Drugs Market is expected to climb to USD 456.18 billion by 2035, registering a CAGR of 6.92% across the forecast window. Two catalysts anchor this trajectory: the U.S. FDA's continued expansion of its orphan product designation pipeline — which exceeded 600 new designations annually by 2024 [1] — and the European Medicines Agency's evolving incentive framework that grants up to ten years of market exclusivity for designated orphan drug status therapies [2].

A fundamental shift in therapeutic modality is reshaping how rare disease treatments reach patients. Legacy small-molecule approaches are giving way to biologics-led innovation — gene therapies, antisense oligonucleotides, and enzyme replacement platforms now represent the fastest-growing development pipelines. The National Institutes of Health allocated over USD 6.3 billion toward rare genetic disorder drug research in fiscal year 2024, a 12% increase from the prior year [3]. AI-enabled adaptive trial designs are compressing Phase II timelines by as much as 45%, lowering the historically prohibitive cost of developing ultra-rare condition medications [4].

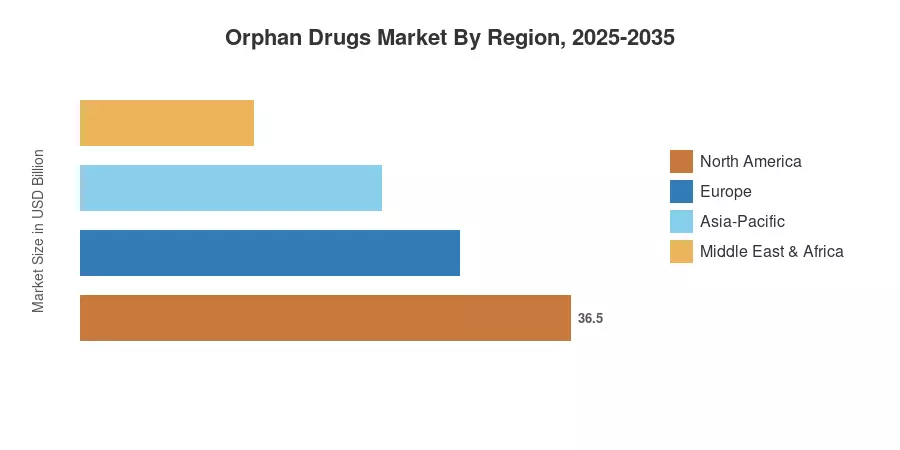

North America commands the largest share of the Orphan Drugs Market, holding approximately 48.8% of global revenue in 2025. Asia-Pacific stands as the fastest-growing region, driven by China's expanded rare-disease catalog and Japan's SAKIGAKE accelerated pathway for small patient population therapy approvals, with a projected CAGR of 12.18% through 2035 Europe remains the second-largest region, contributing roughly 27% of global value, though pending revisions to exclusivity rules may reshape competitive dynamics in the coming years.

Key Report Takeaways

• By Drug Type

- Biologics dominated the Orphan Drugs Market in 2025 with a revenue share of approximately 70.2%, fueled by expanding gene therapy and monoclonal antibody pipelines

- Non-biologics are projected to grow at a CAGR of 5.14% through 2035, supported by next-generation small-molecule platforms targeting rare genetic disorder drugs

• By Disease Area

- Oncologic disorders accounted for USD 93.27 Billion in 2025, reflecting the concentration of designated orphan drug status approvals in hematologic malignancies

- Neurologic disorders represent the fastest-expanding disease segment in the Orphan Drugs Market, with a forecast CAGR of 13.85% to 2035

• By Route of Administration

- Parenteral delivery held a 75.1% share of the Orphan Drugs Market in 2025, driven by biologics' infusion requirements

- Oral therapies are expected to post an 12.82% CAGR through 2035, as formulation science improves bioavailability for ultra-rare condition medications

• By Distribution Channel

- Hospital pharmacies captured approximately 66.9% of distribution in 2025, reflecting the clinical complexity of rare disease treatments

- Online pharmacies are expanding at a 14.25% CAGR, the fastest among all channels in the Orphan Drugs Market

• By Region

- North America retained dominance with a 48.8% share, anchored by favorable reimbursement for small patient population therapy

- Asia-Pacific's projected 12.18% CAGR makes it the fastest-growing region in the Orphan Drugs Market through 2035

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue analysis of approved orphan-designated products across 45+ countries, cross-validated with top-down prescription and reimbursement data from national health authorities. Historical figures draw on FDA and EMA orphan designation databases, company filings, and payer claims data [1][5].