Passenger Information System Market Summary

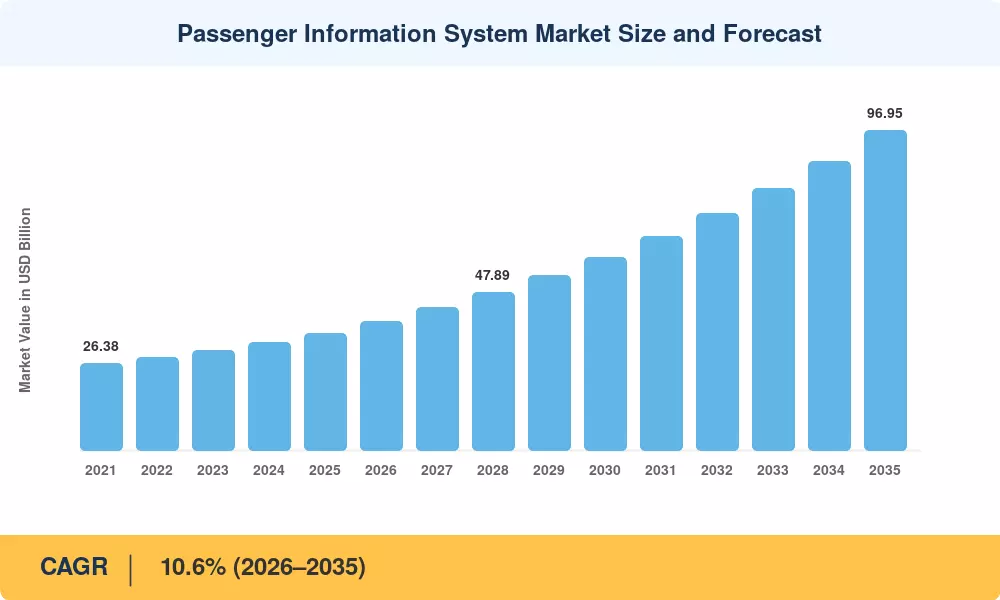

The Passenger Information System Market was valued at USD 35.40 billion in 2025 and is projected to grow from USD 39.15 billion in 2026 to USD 96.95 billion by 2035, registering a CAGR of 10.6% during the forecast period. Governments worldwide have accelerated investment in transit digitization—the U.S. Federal Transit Administration's Capital Investment Grants Program alone authorized over USD 3.2 billion for transit modernization in FY 2024, much of it earmarked for rider-facing information infrastructure [1]. The European Commission's Sustainable and Smart Mobility Strategy further mandates interoperable traveler data by 2030, channeling billions into cross-border rail and urban transit upgrades [2].

Legacy static signage, paper timetables, and stand-alone public-address units are giving way to cloud-connected platforms that fuse GPS tracking, predictive analytics, and multi-language accessibility into a single dashboard. The convergence of 5G networks, edge processors, and AI-driven disruption management allows transit operators to push context-aware alerts to displays, mobile apps, and wearables simultaneously—shrinking dwell times and lifting on-time performance by measurable margins [3].

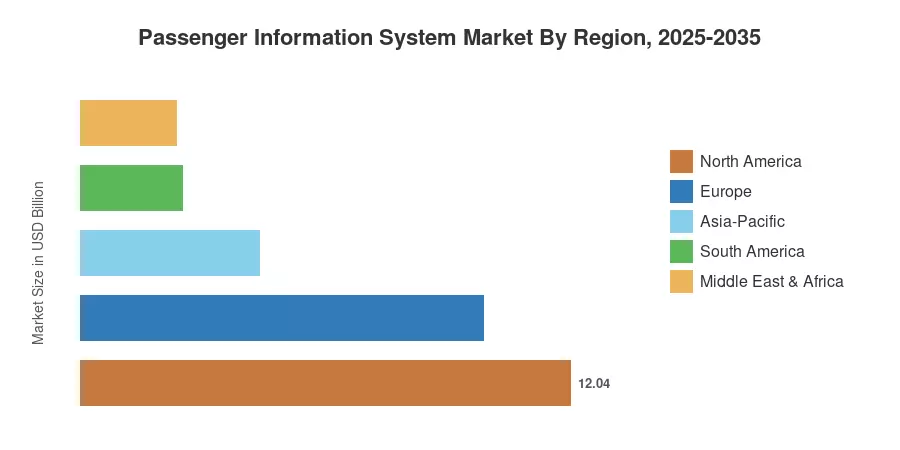

North America leads the Passenger Information System Market with roughly 34% of global revenue, anchored by mature rail and bus-rapid-transit networks. Asia-Pacific is the fastest-growing region at a projected 12.4% CAGR, propelled by metro-rail expansion across India, China, and Southeast Asia. Europe holds the second-largest share at approximately 28%, driven by stringent accessibility directives and dense commuter rail networks. As transit agencies pivot from capital-heavy hardware cycles to subscription-based software models, the Passenger Information System Market is poised for sustained double-digit growth through 2035.

Key Report Takeaways

• By Component

- Hardware accounted for roughly 43.3% of Passenger Information System Market revenue in 2025, reflecting ongoing demand for ruggedized displays and onboard processors.

- The software sub-segment is forecast to register a 15.5% CAGR through 2035, driven by cloud analytics and predictive-disruption platforms.

• By Solution

- Information/Display Systems captured approximately 39.5% of the market share in 2025, the single largest solution category.

- Mobile Applications are projected to grow at a 15.1% CAGR as transit riders increasingly rely on smartphone-based trip planning.

• By Deployment Location

- Station/Wayside installations represented roughly 52.4% of the Passenger Information System Market in 2025.

- On-Board Systems are expanding at a 16.4% CAGR, fueled by next-generation trains with integrated passenger-display ecosystems.

• By Mode of Transportation

- Roadway/Bus and Coach networks held about 47.4% market share in 2025, reflecting the sheer scale of urban bus fleets globally.

• By Region

- North America commanded ~34% of the global Passenger Information System Market revenue.

- Asia-Pacific registered the fastest growth at an estimated 12.4% CAGR, led by massive metro-rail buildouts.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model triangulates bottom-up revenue from component manufacturers, system integrators, and software platform providers against top-down macroeconomic indicators, including transit-capital expenditure growth, urbanization rates, and government infrastructure budgets. Historical values (2021–2024) rely on audited company filings and validated government procurement records; the forecast period applies a calibrated CAGR anchored to identified demand drivers and restraint offsets.

.webp?v=1782471417)