Philippines Telecom Market Summary

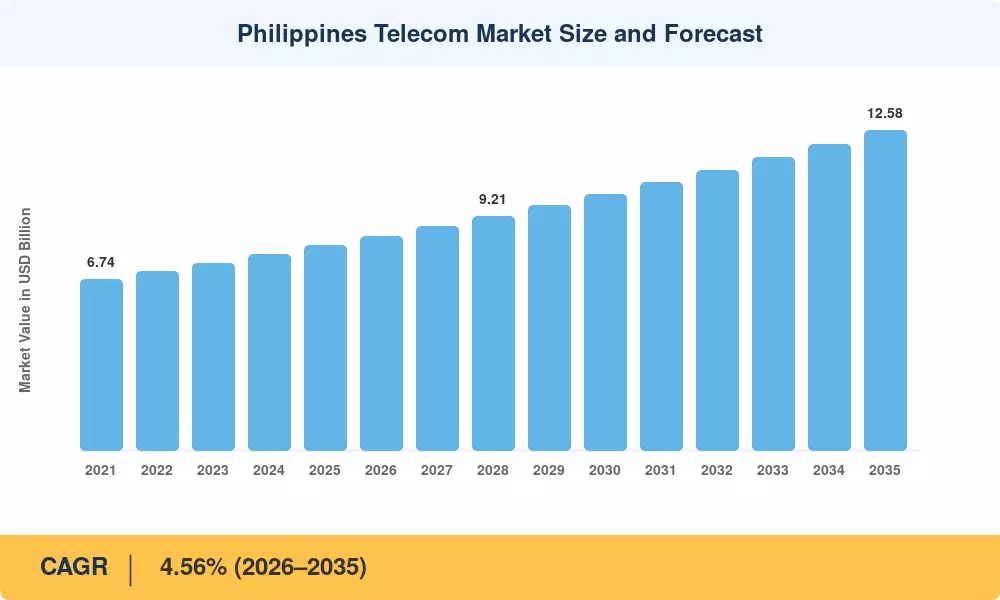

The Philippines Telecom Market was valued at USD 8.06 billion in 2025 and is projected to reach USD 8.41 billion in 2026 before climbing to USD 12.58 billion by 2035, expanding at a 4.56% CAGR during 2026–2035. This growth trajectory is anchored in the National Broadband Program's commitment to connect all municipalities by 2028 and the National Telecommunications Commission's (NTC) progressive spectrum allocation reforms that opened the 3.5 GHz and 26 GHz bands for 5G rollout by PLDT and Globe in Philippines [2]. Telco infrastructure investment in Philippines reached an estimated USD 2.3 billion in combined capital expenditure during 2024, signaling operator confidence in long-term demand [3].

A sweeping technology transformation is reshaping the Philippines Telecom Market as operators retire legacy 2G and 3G networks to redirect spectrum toward 4G LTE-Advanced and 5G NR deployments. Fixed broadband and fiber in the Philippines are accelerating rapidly, with PLDT's fiber-to-the-home footprint surpassing 8.5 million homes passed by mid-2025 [4]. Globe Telecom committed PHP 89 billion in capex during 2024 to densify its mobile and fixed broadband and fiber in the Philippines network, while Dito Telecommunity continued aggressive tower builds across Visayas and Mindanao [5]. OTT services and mobile data growth Philippines have emerged as critical revenue catalysts, with video streaming alone accounting for over 45% of downstream mobile traffic.

The Philippines dominates its single-country scope within the broader ASEAN telecom landscape, but the digital economy and connectivity in ASEAN Philippines positions the archipelago as the region's second-largest mobile subscriber base behind Indonesia. Enterprise connectivity is the fastest-growing end-user category at an estimated 4.82% CAGR through 2035, driven by BPO-sector demand for dedicated bandwidth and cloud-based unified communications As 5G coverage expands beyond Metro Manila into secondary cities, the Philippines Telecom Market is poised for a decade of infrastructure-led revenue acceleration.

Key Report Takeaways

• By Service Type

- Mobile data services captured approximately 57% of the Philippines Telecom Market in 2025, reflecting the country's mobile-first internet culture and rising smartphone penetration

- IoT and M2M services are projected to grow at a 4.68% CAGR through 2035, propelled by smart city pilots in Cebu and Davao and industrial automation in manufacturing zones

- OTT services and mobile data growth Philippines contributed USD 0.74 billion in 2025 revenue as streaming platforms compete for subscribers

• By End User

- The consumer segment held 72.5% of the Philippines Telecom Market share in 2025, underpinned by 82 million unique mobile subscribers and affordable prepaid data bundles

- Enterprise connectivity is advancing at a 4.82% CAGR, the fastest among end-user segments, as BPO firms and fintech companies scale their digital economy and connectivity in ASEAN Philippines operations

• By Region

- The National Capital Region (NCR) accounted for the largest revenue concentration due to population density and enterprise headquarters clustering

- Visayas and Mindanao represent the fastest-expanding coverage zones, with Dito Telecommunity targeting 84% population coverage by 2027

• Philippines Telecom Market Size and Forecast (2021–2035)

MRFR's market sizing integrates primary operator revenue filings (PLDT, Globe, Dito, Converge), NTC subscriber data, and proprietary demand modeling that triangulates ARPU trends against macro indicators, including GDP per capita and smartphone adoption. Historical values reflect audited annual reports; forecast figures apply a calibrated CAGR anchored to spectrum auction schedules and infrastructure deployment timelines.