Piezoelectric Devices Market Summary

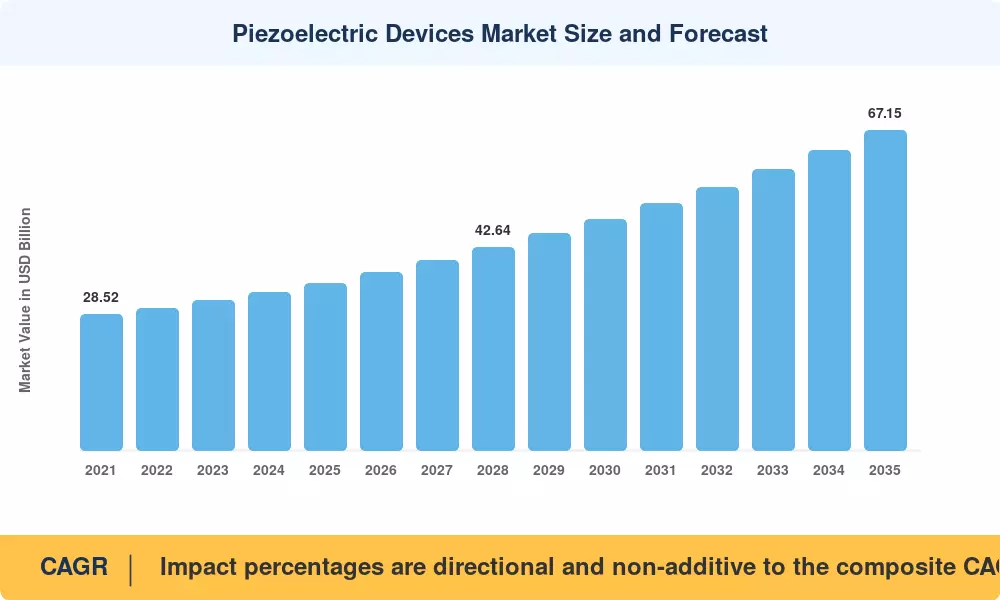

The Piezoelectric Devices Market reached USD 35.10 Billion in 2025 and is projected to grow from USD 37.45 Billion in 2026 to USD 67.15 Billion by 2035, registering a CAGR of 6.70% during the forecast period (2026–2035). Two catalysts anchor this trajectory: the global rollout of 5G-Advanced infrastructure, which depends on bulk acoustic wave filters fabricated from advanced piezo materials, and the European Union's revised RoHS directive pushing manufacturers toward lead-free piezoelectric compositions such as potassium sodium niobate [1]. These regulatory and technology forces create a durable demand floor that extends well beyond the current investment cycle.

Across the value chain, legacy bulk ceramic transducers are giving way to thin-film and single-crystal architectures that deliver higher electromechanical coupling at smaller footprints. The U.S. Department of Energy's USD 280 million advanced manufacturing initiative for smart-sensor integration in industrial plants underscores the government's willingness to subsidize next-generation piezo deployment [2]. Aluminum scandium nitride films, once confined to laboratory prototypes, now enable commercial RF filter production above 6 GHz, unlocking new spectrum for 5G and satellite communications.

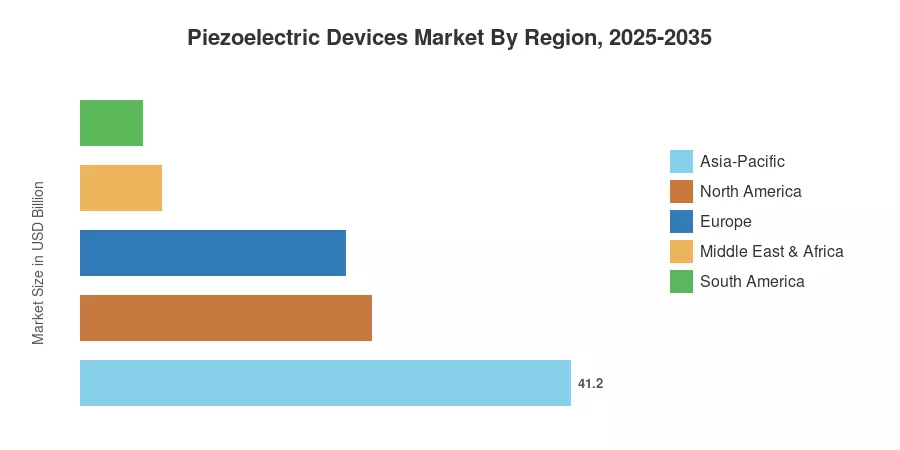

Asia-Pacific commands roughly 41.2% of the Piezoelectric Devices Market, driven by consumer electronics manufacturing clusters in China, Japan, and South Korea. The Middle East & Africa is the fastest-growing region, fueled by oil-and-gas sensing installations, while North America holds the second-largest share at approximately 24.5% on the strength of defense and medical device procurement. The Piezoelectric Devices Market is poised to benefit from convergent electrification, miniaturization, and industrial digitization trends through 2035.

Key Report Takeaways

• By Product Type

- Sensors accounted for 34.0% of the Piezoelectric Devices Market in 2025, supported by industrial condition-monitoring deployments across manufacturing and energy sectors.

- Energy harvesters represent the fastest-growing product segment, advancing at a 9.4% CAGR through 2035 as self-powered IoT nodes gain traction in remote infrastructure.

• By Material

- Ceramics commanded 62.0% revenue share in 2025, reflecting their cost efficiency and broad application compatibility across the Piezoelectric Devices Market.

- Polymers are expected to grow at a 9.0% CAGR through 2035, driven by flexible wearable and biomedical sensing applications.

• By End-User Industry

- Consumer electronics led the Piezoelectric Devices Market with 29.5% revenue share in 2025, anchored by smartphone haptic actuators and RF filter demand.

- Automotive and transportation are forecast to post an 8.1% CAGR through 2035 as electric vehicle platforms adopt piezo-based fuel injectors, parking sensors, and structural health monitors.

• By Region

- Asia-Pacific dominated the Piezoelectric Devices Market at 41.2% share in 2025.

- The Middle East & Africa are projected as the fastest-growing region, expanding on energy-sector sensing investments.

Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from trade association shipment data, company filings, and customs records, while forecast projections rely on bottom-up demand modeling calibrated against macroeconomic indicators, technology adoption curves, and policy timelines. All figures are denominated in current USD Billion.