Polyacrylamide Market Summary

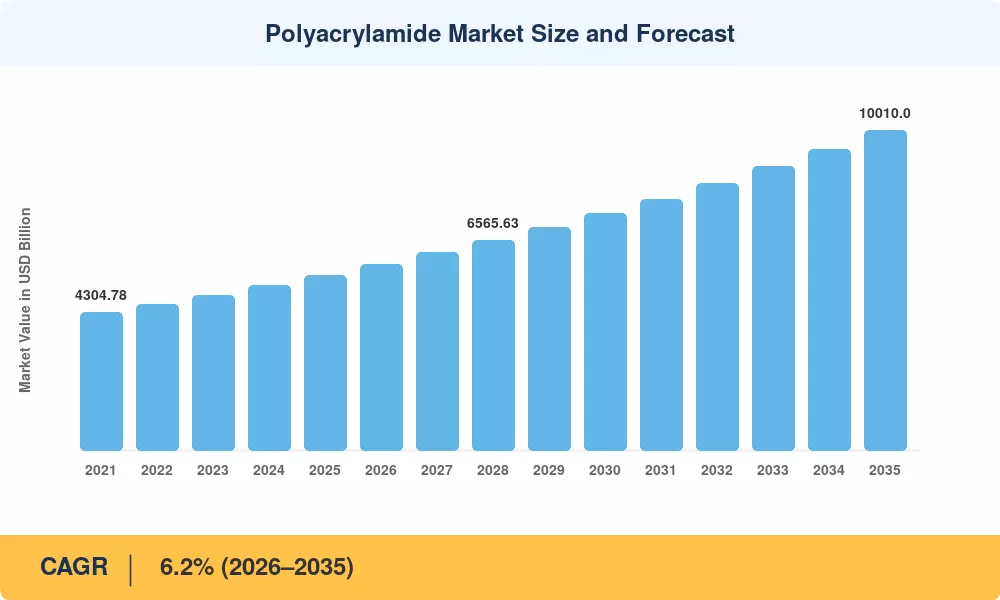

The global Polyacrylamide Market reached an estimated USD 5,480 million in 2025 and is projected to grow from USD 5,820 million in 2026 to approximately USD 10,010 million by 2035, registering a CAGR of 6.2% during the forecast period. Two catalysts are reshaping demand trajectories: the EU Urban Wastewater Treatment Directive 2024/3019, which mandates quaternary nutrient-removal stages across member states by 2030, and tightening EPA residual-monomer caps in the United States that are pushing municipal operators toward certified, high-purity acrylamide polymers [2][3].

A decisive shift is underway from commodity-grade polymer flocculants toward specialty formulations. Enhanced oil recovery programs in North American shale basins now require salt-tolerant, ultra-high-molecular-weight grades that commodity products cannot deliver. Simultaneously, semiconductor fabs across Taiwan, South Korea, and Japan are adopting precision-dosed water treatment polymers to meet sub-ppb purity thresholds, a specification level that has attracted over USD 1.2 billion in combined R&D investment from leading producers since 2023 [4][5].

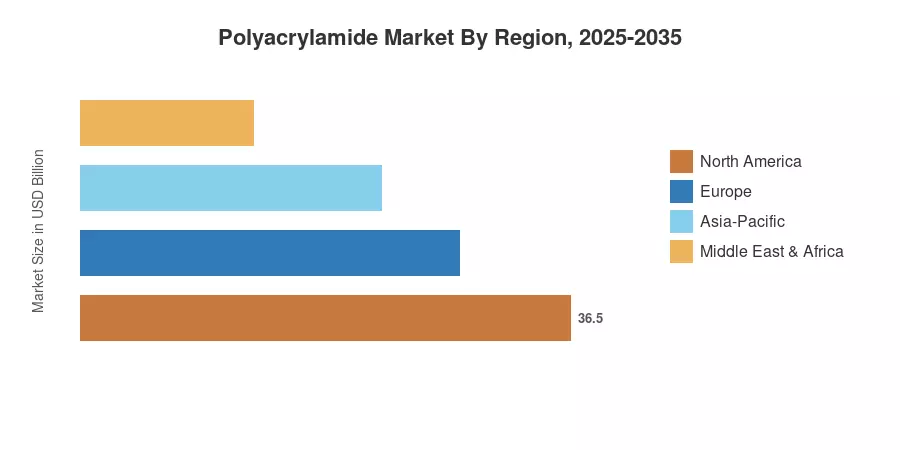

Asia-Pacific anchors the Polyacrylamide Market with roughly 53.4% of global revenue in 2025, driven by China's sludge treatment chemicals mandates and India's Jal Jeevan Mission water infrastructure program. North America follows with approximately 20% share, supported by oilfield chemicals demand across the Permian Basin. Europe accounts for about 17% share, led by nutrient-removal retrofit projects under the revised Urban Wastewater Directive. Through 2035, intensifying regulatory standards and the pivot toward bio-based flocculant chemicals will continue reshaping competitive dynamics across every region

Key Report Takeaways

• By Physical Form

- Powder formulations commanded the leading position in the Polyacrylamide Market in 2025, capturing 46.8% of global revenue share

- Emulsion/dispersion products are forecast to expand at a 6.6% CAGR through 2035, driven by automated dosing compatibility and ease of handling for wastewater treatment additives

• By Application

- Flocculants for water treatment held 44.4% of the Polyacrylamide Market revenue in 2025, reflecting municipal infrastructure expansion across developing economies

- Enhanced oil recovery applications are projected to grow at a 6.7% CAGR to 2035 as tertiary recovery programs intensify in mature shale formations

• By End-User Industry

- Water treatment accounted for 44.2% of the Polyacrylamide Market size in 2025, underscoring the dominance of industrial treatment chemicals in municipal and industrial settings

- Oil and gas end users are advancing at a 6.6% CAGR through 2035, fueled by rising oilfield chemicals consumption for heavy crude extraction

• By Region

- Asia-Pacific led the Polyacrylamide Market in 2025 with 53.4% share and is expanding at a 6.7% CAGR through 2035

- North America's shale-driven demand for polymer flocculants positions the region as a key growth contributor at a 5.9% CAGR

Market Size and Forecast (2021–2035)

MRFR's market sizing combines bottom-up revenue modeling from over 120 producer and distributor interviews with top-down validation using trade-flow data from UN Comtrade and regional chemical industry associations. Historical values are calibrated against audited company filings, while forecast projections apply segment-weighted CAGR analysis anchored to regulatory implementation timelines and capital expenditure plans disclosed by major end users.

.webp?v=1783672358)