Power Tools Market Summary

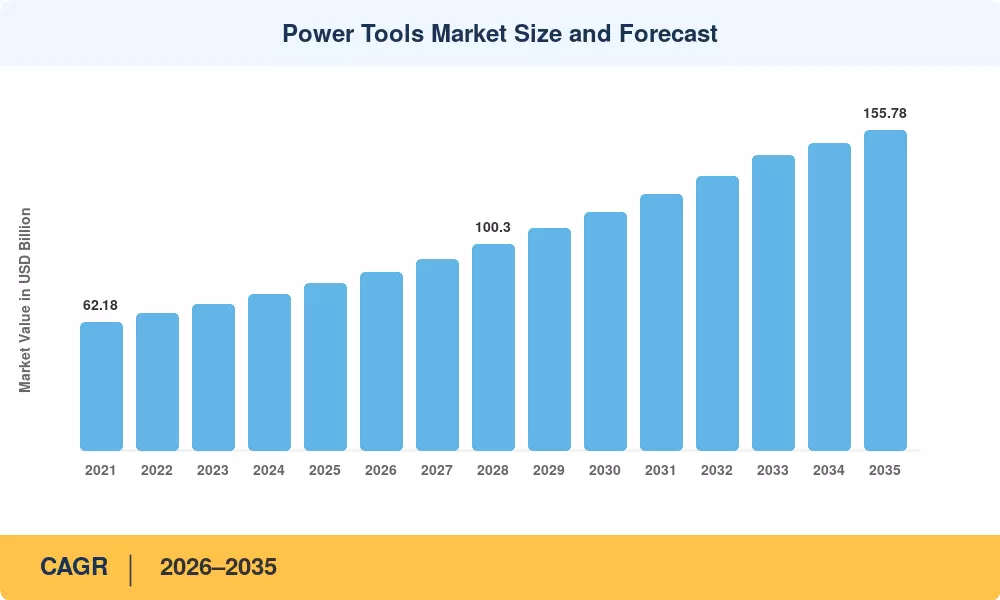

The Power Tools Market stood at USD 81.42 billion in 2025 and is projected to reach USD 86.47 billion by 2026 before climbing to USD 155.78 billion by 2035, expanding at a CAGR of 7.38% during 2026–2035. Accelerating public infrastructure budgets — including India's USD 133 billion capital expenditure allocation under Union Budget 2026 [1] and the United States' CHIPS and Science Act fabrication commitments [2] — are anchoring demand for high-precision, safety-compliant electric tools across construction sites and semiconductor cleanrooms alike.

A dramatic technology change is taking place in the Power Tools Market. The corded and pneumatic platforms that have dominated workshops for decades are being replaced by the lithium-ion cordless devices that can generate more than 550 watt-hours per charge. This change eliminates the risks of extension cords and exhaust fumes while matching – and in many torque-controlled applications surpassing – the output of older gasoline-powered systems. Battery-powered angle grinder models and cordless brushless drill driver platforms are now the fastest-selling SKU categories in the professional and retail channels [3]. Similarly, the rotary hammer SDS drill industry has also migrated to cordless designs with key OEMs collectively investing more than USD 2.1 billion on brushless motor R&D between 2024 and 2027 [4].

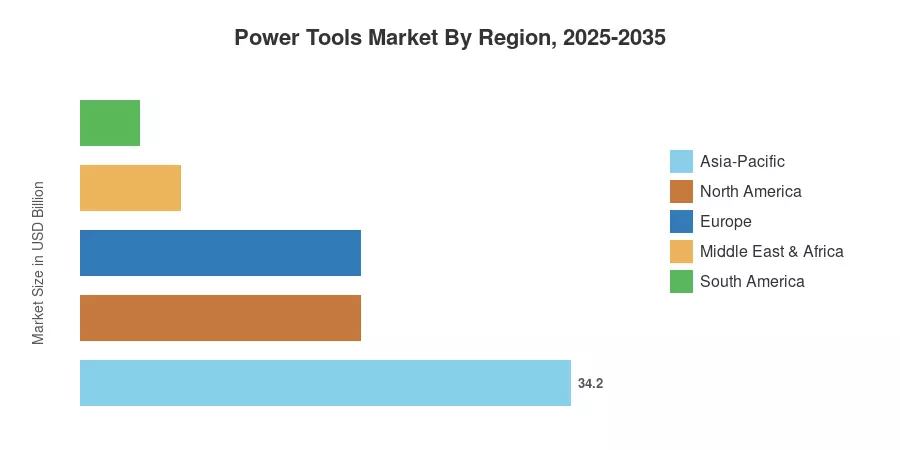

Asia-Pacific commands the dominant position in the Power Tools Market, holding roughly 42% of global revenue, propelled by megaproject pipelines in China, India, and Indonesia Europe trails as the second-largest region at approximately 24% share, buoyed by renovation mandates under the EU Green Deal. North America is the third-largest contributor, yet the residential and DIY segment is expanding rapidly as oscillating multi-tool kit adoption climbs among homeowners. The decade ahead will reward manufacturers that pair cordless platform ecosystems with IoT-enabled torque documentation and direct-to-consumer digital storefronts.

Key Report Takeaways

• By Mode of Operation

- Electric tools captured 66.8% of the Power Tools Market revenue in 2025, with cordless variants within this category growing fastest at an 8.18% CAGR through 2035

- Pneumatic and hydraulic tools together account for the balance, though their combined share is contracting as battery energy density improvements accelerate platform migration

• By Product

- Drilling and fastening tools — including the cordless brushless drill driver and rotary hammer SDS drill — held 33.6% share in 2025

- Impact drivers and wrenches are forecast to grow at an 8.72% CAGR through 2035, the fastest among product sub-segments in the Power Tools Market

- Cutting and grinding tools, led by the angle grinder battery-powered segment, represent a USD 18.4 billion opportunity by 2035

• By End-User

- Construction and infrastructure end-users accounted for 48.9% of the Power Tools Market size in 2025

- The residential and DIY segment is the fastest-growing end-user category, registering an 8.84% CAGR as power tool combo kit set bundles drive household penetration

• ByRegion

- Asia-Pacific leads with a 42% revenue share, while North America is valued at approximately USD 19.54 billion in 2025

- The Middle East & Africa region is expanding at the highest regional CAGR of 8.6%, driven by Saudi Vision 2030 construction activity

Market Size and Forecast (2021–2035)

Market Research Future's Power Tools Market sizing relies on a bottom-up triangulation of OEM shipment data, distributor sell-through figures, and customs trade databases across 35 countries, cross-validated against top-down macroeconomic indicators such as construction output and manufacturing PMI indices.