Privacy Management Software Market Summary

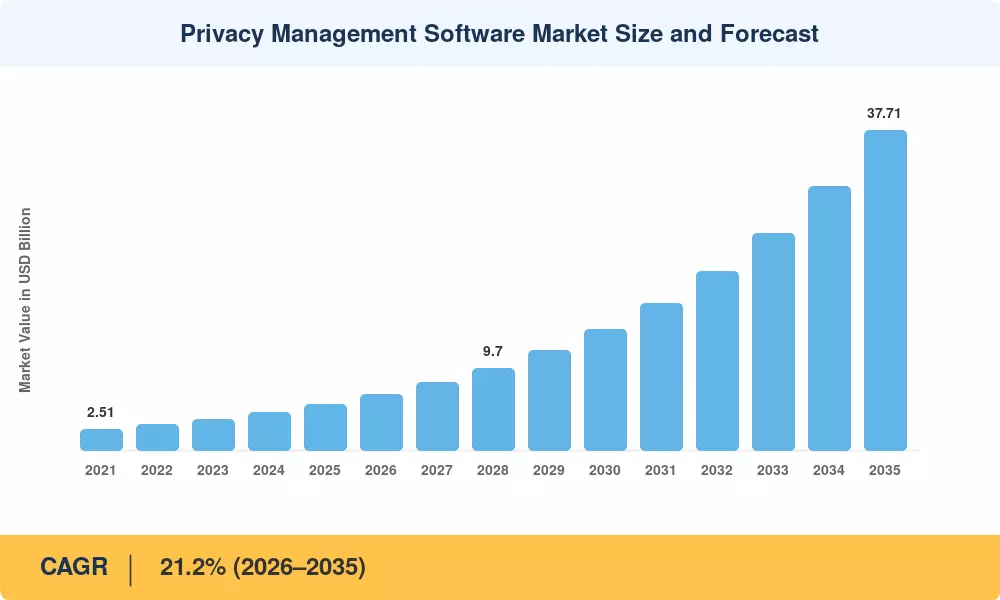

The Privacy Management Software Market reached an estimated USD 5.42 billion in 2025 and is projected to climb to USD 6.68 billion in 2026 before expanding to USD 37.71 billion by 2035, registering a CAGR of 21.2% across the 2026–2035 forecast window. Two catalysts are pulling budgets forward faster than most CIOs anticipated: the proliferation of omnibus privacy statutes — 16 U.S. states enacted comprehensive data privacy compliance tools legislation between 2023 and 2025 alone [2] — and the European Commission's AI Act, which embeds consent management platforms obligations directly into model-governance workflows [3]. Enterprises no longer view privacy software as a compliance checkbox; it has become operational infrastructure.

A generational technology shift is underway inside the Privacy Management Software Market. Legacy spreadsheet-driven privacy-impact assessments and manual data-mapping exercises are giving way to AI-powered discovery engines that crawl structured and unstructured repositories in real time. estimates that organizations deploying automated personal data protection tools reduced audit preparation time by 40% in 2024, freeing compliance teams to focus on strategic risk posture rather than documentation backlogs [4]. Investment reflects the momentum — venture and growth-equity funding into GDPR privacy software startups exceeded USD 2.1 billion in the 2023–2024 cycle [5].

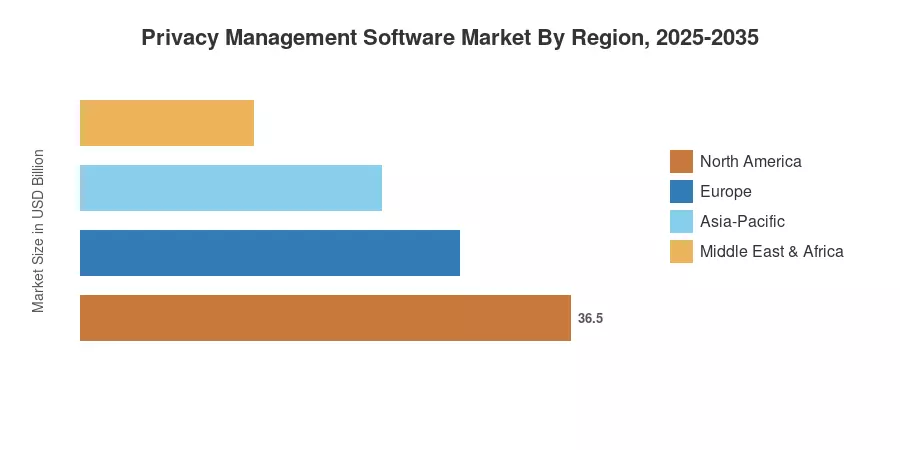

North America held approximately 40.4% of the Privacy Management Software Market in 2025, driven by California's evolving CPRA enforcement actions and a federal privacy bill progressing through Congress. Asia-Pacific is the fastest-growing region at a 29.1% CAGR, fueled by India's Digital Personal Data Protection Act and China's tightening cross-border transfer rules. Europe retained the second-largest share on the back of GDPR enforcement fines that surpassed EUR 4.2 billion cumulatively by late 2024 [6]. The decade ahead will reward vendors that combine privacy risk management depth with AI-native automation.

Key Report Takeaways

• By Component

- Solutions commanded 76.0% of the Privacy Management Software Market in 2025, reflecting enterprise preference for integrated consent management platforms over point tools.

- Services are expanding at a 26.1% CAGR through 2035 as organizations outsource implementation and managed privacy operations.

• By Deployment

- Cloud-deployed models accounted for 61.7% of the Privacy Management Software Market, accelerated by SaaS-first procurement policies.

• By Organization Size

- Cloud-deployed models accounted for 61.7% of the Privacy Management Software Market, accelerated by SaaS-first procurement policies.

- SMBs represent the fastest-growing cohort at a 25.1% CAGR, entering the compliance arena through affordable data privacy compliance tools.

• By Functionality

- Consent and preference management captured 33.1% of total functionality spend in 2025.

• By End-User Vertical

- Consent and preference management captured 33.1% of total functionality spend in 2025.

- BFSI dominated end-user verticals with 25.5% revenue share, while healthcare and life science is scaling at a 21.8% CAGR, leveraging personal data protection tools for HIPAA-GDPR alignment.

• By Region

- North America retained 40.4% of the Privacy Management Software Market, anchored by accelerating U.S. state-level privacy legislation.

- Asia-Pacific is rising at a 29.1% CAGR as data-localization mandates drive demand for GDPR privacy software equivalents across India, Japan, and South Korea.

Market Size and Forecast (2021–2035)

MRFR's sizing methodology triangulates vendor revenues, regulatory compliance spend surveys, and enterprise IT budget allocations across 32 countries. Historical figures (2021–2024) are validated against audited annual reports and spending trackers; forecast figures apply the calibrated 21.2% CAGR with adjustments for regulatory acceleration years.