Proton Pump Inhibitors Market Summary

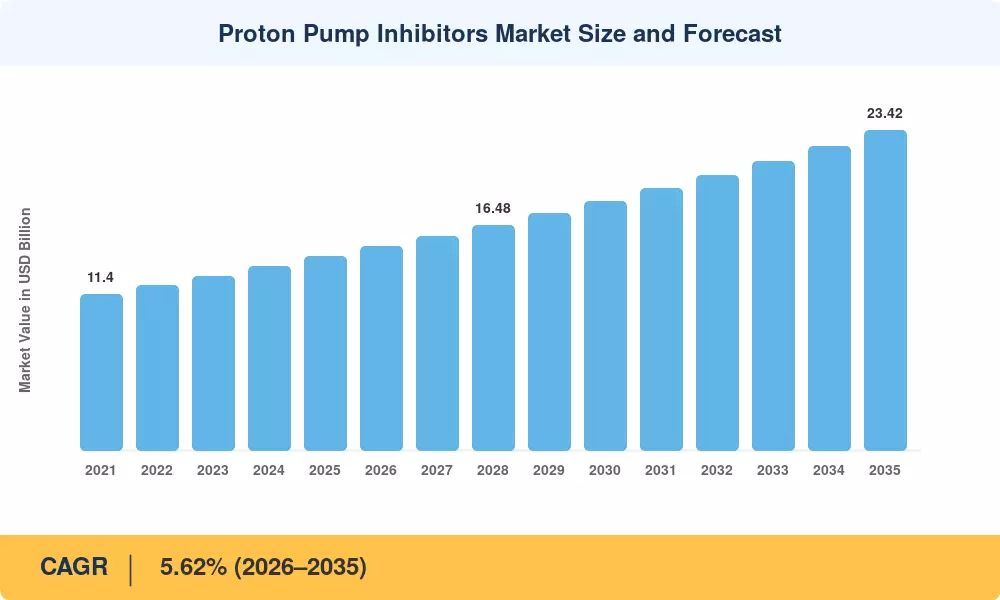

The Proton Pump Inhibitors Market reached an estimated USD 14.18 billion in 2025, with the forecast period opening at USD 15.02 billion in 2026 and climbing to USD 23.42 billion by 2035 at a CAGR of 5.62%. Two converging forces anchor this trajectory: expanded over-the-counter access policies across G7 economies and the accelerating prevalence of gastroesophageal reflux disease tied to urbanized dietary patterns. Government-backed programs for acid reflux medication affordability — including Japan's revised National Health Insurance pricing schedule and India's Jan Aushadhi generic formulary — are channeling billions in subsidized prescription volume toward gastric acid suppression therapies [2].

A pronounced shift is underway from legacy oral capsule formulations toward intravenous delivery systems optimized for critical-care and post-surgical settings. Hospital formularies increasingly favor IV pantoprazole and esomeprazole for patients who cannot tolerate enteral dosing, a transition accelerated by roughly USD 420 million in cumulative clinical-trial investment between 2022 and 2025 [3]. Omeprazole therapy remains the foundational molecule, yet next-generation potassium-competitive acid blockers are beginning to capture share in gastric acid suppression protocols across East Asia, pressuring established brands to reformulate or bundle combination packs with prokinetic agents.

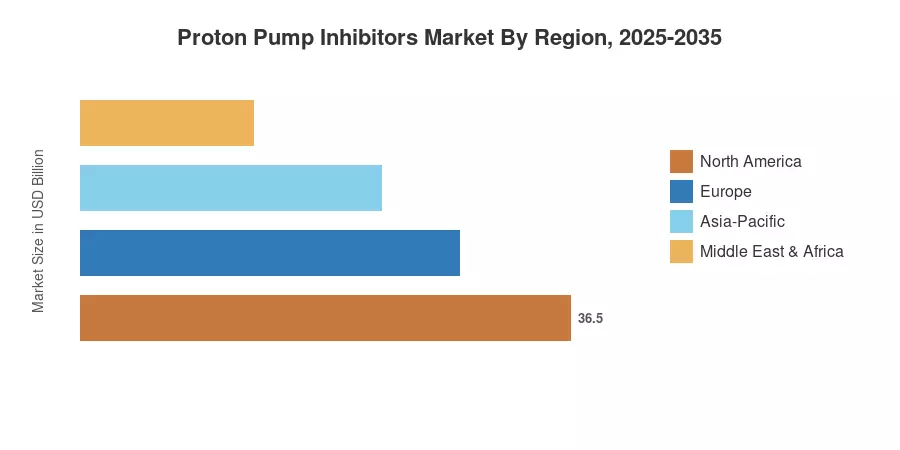

North America retained the largest share of the Proton Pump Inhibitors Market at approximately 39.8% in 2025, buoyed by high GERD treatment drug utilization and robust insurance reimbursement. Asia-Pacific is the fastest-growing region, projected to expand at a 7.02% CAGR through 2035, driven by generic manufacturing scale in India and China. Europe holds the second-largest share at roughly 26.5%, supported by harmonized EU regulatory pathways for stomach ulcer medication approvals [4]. The decade ahead will be defined by biosimilar PPIs entering clinical pipelines and digital therapeutics platforms that pair acid reflux medication with behavioral coaching.

Key Report Takeaways

• By Drug Type

- OTC formulations commanded approximately 48.2% of the Proton Pump Inhibitors Market in 2025, reflecting widespread self-medication trends and expanded pharmacy access

- Prescription drugs are projected to register a 6.98% CAGR through 2035, propelled by specialist-initiated GERD treatment drugs and high-dose acid suppression regimens

• By Route of Administration

- Oral products captured an estimated USD 8.83 billion share of the Proton Pump Inhibitors Market in 2025, supported by patient-friendly dosing convenience

- The intravenous segment is pacing toward a 7.12% CAGR through 2035, fueled by expanding critical-care and bariatric post-operative protocols

• By Region

- North America accounted for the dominant share of the Proton Pump Inhibitors Market at 39.8% in 2025

- Asia-Pacific leads regional growth with a projected 7.02% CAGR, anchored by generic omeprazole therapy scale-up in India and China

Market Size and Forecast (2021–2035)

MRFR's proprietary sizing framework blends bottom-up prescription volume analysis with top-down revenue benchmarking across 42 countries. Historical data relies on IMS Health/IQVIA audits, national formulary databases, and company filings; forecast projections integrate demographic prevalence modeling, regulatory pipeline tracking, and pricing scenario analysis.