Radar Sensors Market Summary

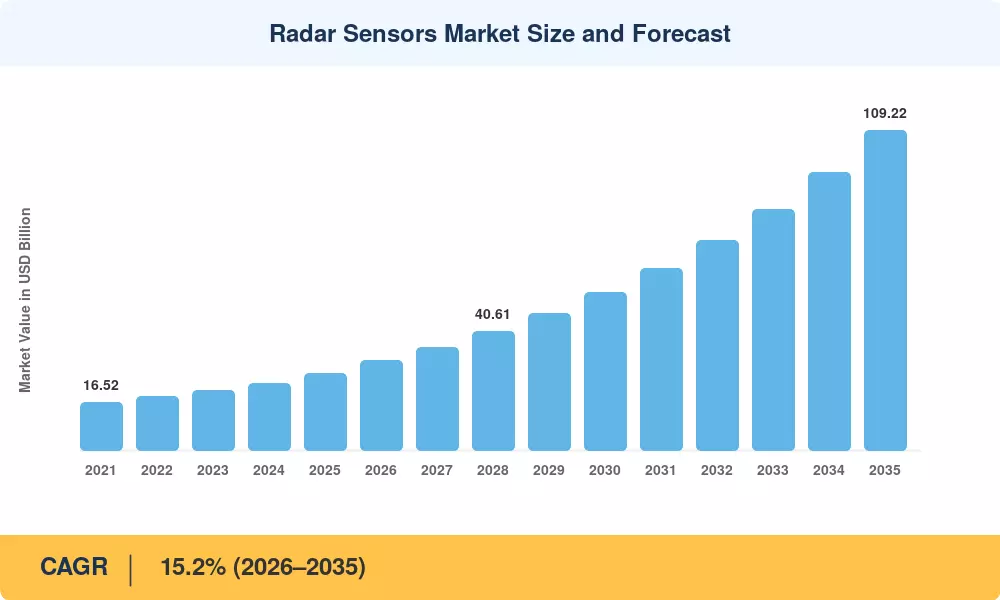

The Radar Sensors Market was valued at USD 26.28 billion in 2025 and is projected to grow from USD 30.57 billion in 2026 to USD 109.22 billion by 2035, registering a CAGR of 15.2% during the forecast period (2026–2035). Two catalysts are pulling demand forward simultaneously: Euro NCAP's tightened 2026 five-star protocol now mandates at least one forward-facing imaging sensor on every new passenger vehicle, and defense budgets across Asia-Pacific are channeling multi-billion-dollar allocations toward active electronically scanned array radar upgrades for surface combatants and fighter fleets [1][2].

Component Level Technology Transition Sweeping the Radar Sensors Market Platform developers are transitioning from legacy 24 GHz architectures to 77-81 GHz modules, yielding roughly ten-fold improvement in range resolution while reducing antenna footprints. Semiconductor vendors have responded with integration of radio-frequency front ends, baseband processing and machine-learning inference into a single system-on-chip, bringing the bill of materials for a short-range module below USD 20 in high-volume manufacturing runs [3]. This trend of integration is also cutting down on design cycles and lowering entrance barriers for Tier-2 automotive suppliers.

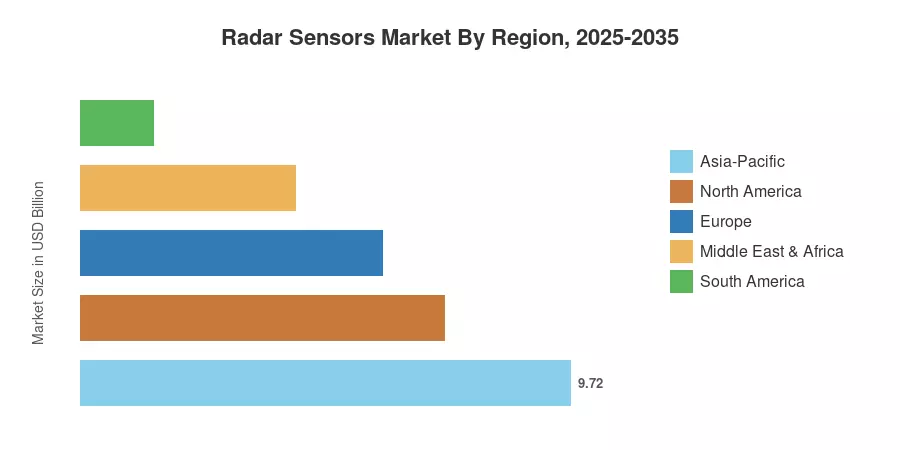

The Asia-Pacific region will have the greatest share of the global Radar Sensors Market with 37.0% of revenue in 2025, driven by China’s Level 2+ ADAS mandates and South Korea’s autonomous-vehicle corridor investments. The fastest-growing territory is the Middle East & Africa region, growing at a 16.2% CAGR through 2035 as smart-city plans in Saudi Arabia and the UAE embed perimeter-surveillance radar into key infrastructure. North America accounts for the second-highest share at 27.5% of the market, driven by Pentagon modernization contracts and the high rate of deployment of collision-avoidance systems by U.S. commercial fleets [4][5]. In the coming decade, radar will increasingly converge with lidar and camera fusion stacks, unlocking performance levels that no single sensing modality can achieve on its own.

Key Report Takeaways

• By Type

- Imaging radar accounted for 53.4% of the Radar Sensors Market in 2025, driven by automakers embedding high-resolution 4D imaging arrays into premium ADAS platforms.

- Non-imaging radar modules are forecast to grow at a 14.6% CAGR through 2035 as industrial and traffic-monitoring deployments scale.

• By Technology

- Frequency-modulated continuous-wave devices captured 51.3% of the Radar Sensors Market revenue in 2025.

- Digital MIMO radar is the fastest-growing technology category, projected at a 15.9% CAGR to 2035, as multi-channel architectures unlock angular super-resolution.

• By End-User

- The automotive segment held a 55.6% share of the Radar Sensors Market in 2025, reflecting mandated forward-collision-warning and adaptive-cruise-control fitment across major regulatory jurisdictions.

- Traffic-monitoring and smart-infrastructure applications are projected to post a 16.7% CAGR through 2035.

• By Geography

- Asia-Pacific led the Radar Sensors Market with 37.0% of the 2025 global revenue.

- The Middle East & Africa is the fastest-growing region at a 16.2% CAGR, fueled by NEOM and Abu Dhabi smart-city radar deployments.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) predictions are based on bottom-up revenue modelling of more than 120 sensor OEMs and Tier-1 suppliers, with top-down cross-validation against semiconductor shipment data, import-export customs records and publicly disclosed vehicle production quantities. Historical figures (2021-2024) are actuals reconciled against corporate filings. 2025 values are calibrated estimates. Forecast numbers (2026-2035) are derived from segment-level growth drivers that are aligned to confirmed regulatory timescales and OEM platform ramp timetables.

.webp?v=1785504474)