Renal Denervation Market Summary

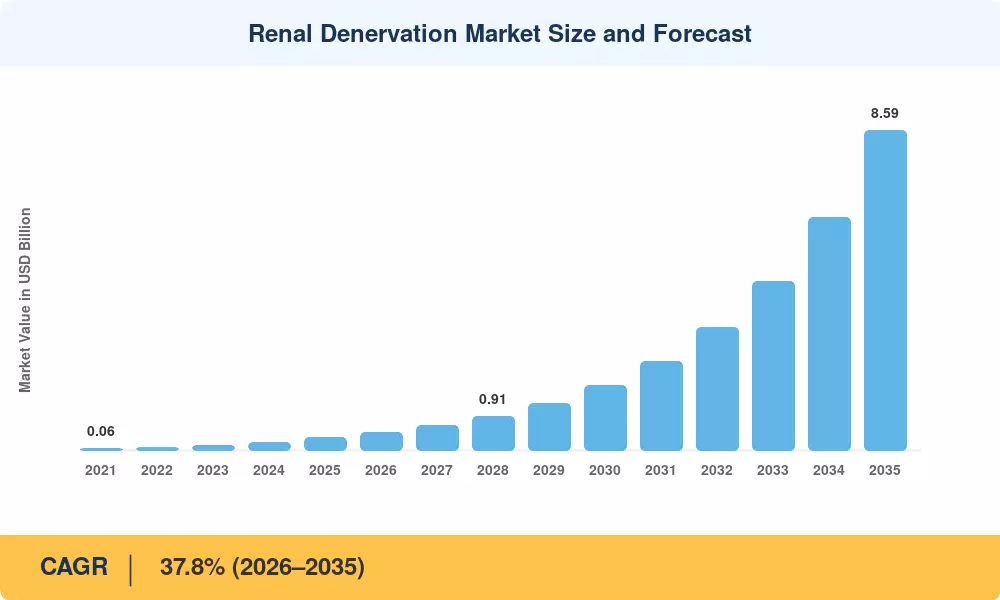

The Global Renal Denervation Market size was valued at USD 0.35 Billion in 2025, and the market is projected to grow from USD 0.48 Billion in 2026 to USD 8.59 Billion by 2035, registering a CAGR of 37.8% during the forecast period 2026–2035. This extraordinary trajectory reflects two converging forces: the global hypertension burden — the World Health Organization estimates roughly 1.28 billion adults aged 30–79 live with hypertension — and a wave of regulatory breakthroughs that have shifted catheter-based nerve ablation from clinical-trial curiosity to mainstream therapeutic option [2]. The FDA's breakthrough device designations for multiple platforms between 2023 and 2025 have opened U.S. reimbursement pathways that were previously the single largest barrier to commercial scale-up.

The technology landscape within the Renal Denervation Market is undergoing a decisive transition. First-generation radiofrequency catheters are giving way to ultrasound-based and micro-infusion platforms that deliver more consistent circumferential ablation patterns with fewer adverse events. Clinical trials such as RADIANCE-HTN TRIO and SPYRAL HTN-ON MED have generated pivotal evidence showing sustained ambulatory blood pressure reductions of 6–9 mmHg at 36 months, prompting several European national health systems to add procedure codes and dedicated reimbursement tiers [3].

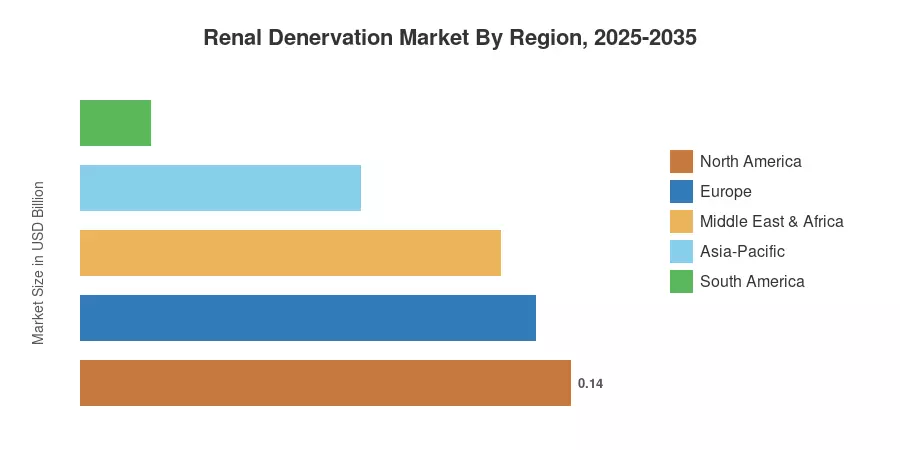

Europe commands the largest share of the Renal Denervation Market at approximately 38% of global revenue, driven by early CE-mark approvals and established reimbursement frameworks in Germany and France. North America is the fastest-growing region, with a projected CAGR of 41.2%, fueled by recent FDA clearances and expanding payer coverage decisions. Asia-Pacific holds roughly 22% of global value, anchored by Japan's advanced interventional cardiology infrastructure and China's growing investment in hypertension management programs. As clinical evidence deepens and device platforms mature, the Renal Denervation Market is positioned to become one of the highest-growth segments in cardiovascular devices through the mid-2030s.

Key Report Takeaways

• By Technology

- Radiofrequency-based platforms represent the dominant technology segment, accounting for approximately 52% of total Renal Denervation Market revenue in 2025, supported by the longest clinical track record and widest installed base of trained operators.

- Ultrasound-based systems are the fastest-growing technology segment, with a projected CAGR of 42.1% through 2035, driven by superior circumferential ablation profiles demonstrated in recent pivotal trials.

- Micro-infusion-based platforms are estimated to reach USD 0.87 billion by 2035, representing the newest entrant class with differentiated chemical ablation mechanisms.

• By End User

- Hospitals account for the largest end-user share of the Renal Denervation Market, reflecting the procedural complexity and imaging requirements of current-generation devices.

- Ambulatory surgical centers are posting a CAGR of 40.5%, driven by shorter procedure times with next-generation platforms and growing outpatient reimbursement models.

• By Region

- Europe leads the Renal Denervation Market with a 38% revenue share, underpinned by Germany's reimbursement leadership and France's expanded procedure coding.

- North America's CAGR of 41.2% makes it the fastest-growing geography, propelled by FDA breakthrough device designations and favorable CMS coverage determinations.

- Asia-Pacific holds approximately 22% of global value, with Japan and China serving as the primary growth engines.

Renal Denervation Market Size and Forecast (2021–2035)

Market Research Future's proprietary model triangulates bottom-up procedure volume estimates from over 40 countries with top-down revenue tracking from device manufacturers' annual filings, regulatory submissions, and hospital procurement databases. Historical figures reflect confirmed commercial shipments; forecast values incorporate pipeline device launches, anticipated reimbursement expansions, and clinical trial readouts scheduled through 2030.