Residential Real Estate Market Summary

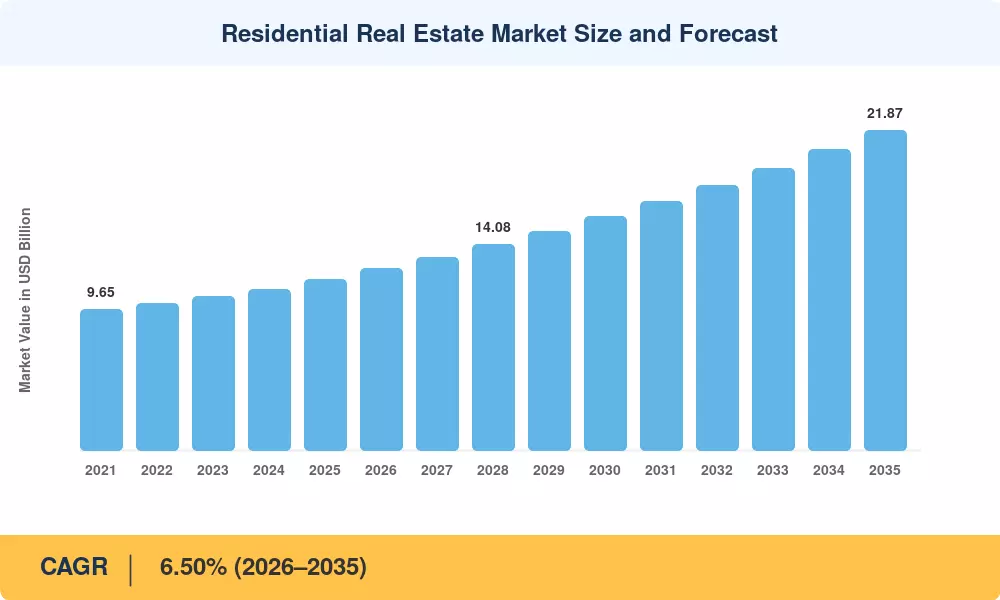

The Residential Real Estate Market was valued at USD 11.67 trillion in 2025 and is projected to reach USD 12.41 trillion by 2026, advancing to USD 21.87 trillion by 2035 at a CAGR of 6.50% during the 2026–2035 forecast period. Persistent housing undersupply across major economies, coupled with government-led construction programs in India, Brazil, and Saudi Arabia, continues to channel both public and private capital into the Residential Real Estate Market at an accelerating pace. Mortgage-support schemes and approvals reform in these countries have stabilized pre-sales pipelines and de-risked project delivery, drawing institutional investors who were historically focused on commercial assets [1].

A technological transformation is reshaping how housing is designed, sold, and managed. Legacy paper-based permitting, manual construction scheduling, and fragmented property management systems are giving way to Building Information Modeling (BIM), proptech transaction platforms, and AI-driven property valuations. The European Union's revised Energy Performance of Buildings Directive (EPBD) has committed member states to near-zero-emission newbuilds by 2030, redirecting an estimated EUR 275 billion annually toward retrofits and low-emissions construction across the continent's aging housing stock [3][4].

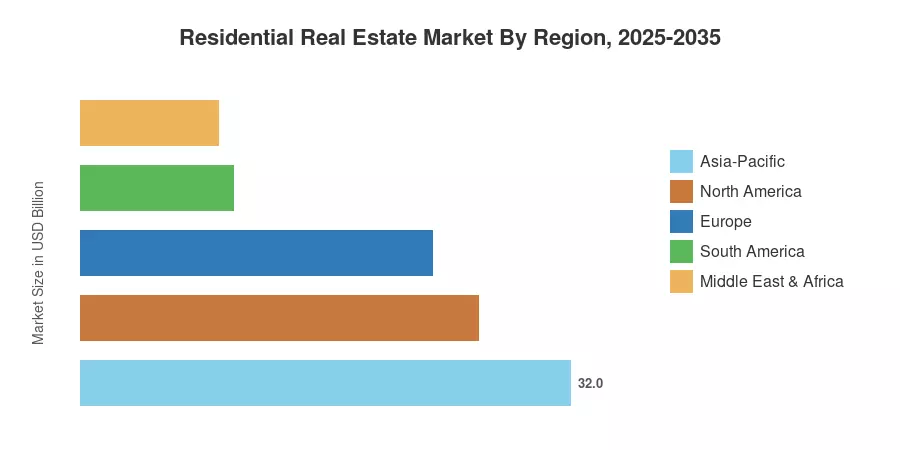

Asia-Pacific commands the largest share of the Residential Real Estate Market at 32.0% of global value and is simultaneously the fastest-growing region, projected at a 7.45% CAGR through 2035. North America holds the second-largest position with a 26.0% share, underpinned by resilient single-family demand and institutional rental expansion. Europe accounts for 23.0% of global activity, with renovation-led investment increasingly outpacing greenfield construction. As urbanization accelerates across emerging economies, the Residential Real Estate Market is positioned for sustained expansion through the next decade.

Key Report Takeaways

• By Property Type

- Apartments and condominiums held a 55.0% share of the Residential Real Estate Market in 2025, driven by urban density preferences and transit-oriented development policies across Asia-Pacific and Europe.

- Villas and landed houses are forecast to grow at a 6.72% CAGR during 2026–2035, reflecting demand for spacious living formats in suburban and peri-urban corridors post-pandemic.

• By Price Band

- Mid-market units accounted for 44.0% of 2025 transaction volumes, supported by government-backed mortgage programs and first-time-buyer subsidies.

- The luxury and super-prime segment is projected to expand at a 6.75% CAGR through 2035, fueled by cross-border wealth migration and branded-residence partnerships.

• By Business Model

- The secondary market represented 57.0% of activity in the Residential Real Estate Market in 2025, as established housing stock turnover remains the primary transaction channel globally.

- Primary sales are set to grow at a 7.12% CAGR through 2035 as large-scale master-planned communities enter delivery phases in India, the Middle East, and Southeast Asia.

• By Mode of Sale

- Outright sales captured 58.0% of transaction activity in 2025.

- Rentals are forecast to grow at a 7.25% CAGR during 2026–2035, as affordability pressure and lifestyle preferences shift tenure patterns in developed markets.

• By Region

- Asia-Pacific led the Residential Real Estate Market with a 32.0% share in 2025 and is expected to post the fastest CAGR of 7.45% through 2035.

- North America held a 26.0% share, while Europe accounted for 23.0% of global value.

Residential Real Estate Market Size and Forecast (2021–2035)

Market sizing draws on national housing-start data, property-registration databases, central-bank mortgage statistics, and proprietary developer surveys across 42 countries. Historical values (2021–2024) reflect audited transaction records and government housing ministry releases. Forecast values (2026–2035) apply econometric models incorporating population growth, urbanization rates, interest-rate scenarios, and policy pipelines.