Reusable Launch Vehicles Market Summary

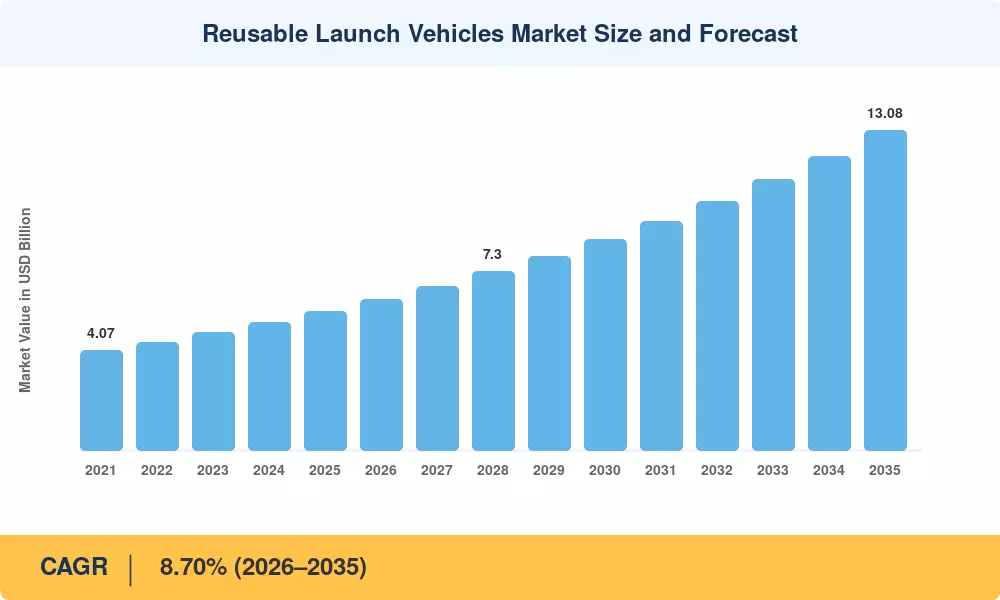

The reusable launch vehicles market was valued at USD 5.68 billion in 2025 and is projected to grow from USD 6.17 billion in 2026 to USD 13.08 billion by 2035, registering a CAGR of 8.70% over the forecast period (2026–2035). Operators across commercial and defense sectors are pivoting decisively from expendable rocket architectures to reusable space launch systems, driven by demonstrated booster life cycles exceeding 35 missions and refurbishment costs below 12% of new-build expenses [2]. NASA's Commercial Crew and Cargo programs, together with U.S. Space Force launch service agreements valued at over USD 5.6 billion through 2027, continue to anchor demand for propulsive landing rocket systems [3].

This is a key technology shift in this industry. The only way to get to orbit was legacy expendable spacecraft. Still, now vertical landing booster rockets and partially reusable first-stage systems that can autonomously recover on drone ships are taking over. The technology for reusable rocket stages has matured to the point where turnaround cycles are now weeks, not months, and the low-cost orbital access technology has brought the per-kilogram launch cost from ~USD 54,500 on expendable platforms to less than USD 2,700 on high-flight-rate reusable systems [4]. From 2021 to 2024, private investment globally toward reusable space launch systems topped USD 14.8 billion [5].

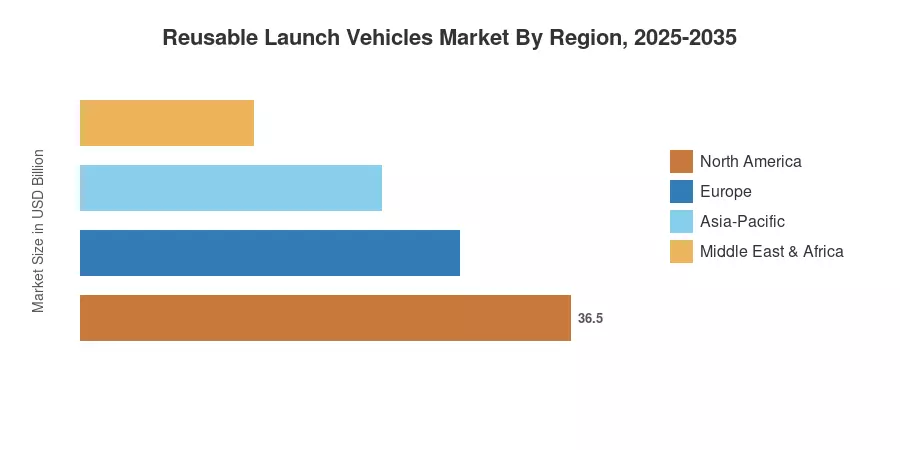

The reusable launch vehicles market is expected to be dominated by North America, with an estimated 77.5% share owing to SpaceX’s high-cadence operations and ULA’s Vulcan program. The Asia-Pacific is the fastest developing market with a projected CAGR of 19.0%, powered by ambitious national programs in rocket stage reusability technologies of China and India. Europe’s share is 10.2% due to the ArianeGroup’s development of the next-gen vehicle. Reusable space launch vehicles will progressively define worldwide access to orbit and beyond over the coming decade.

Key Report Takeaways

• By Type

- Partially reusable systems captured 88.5% of the reusable launch vehicles market share in 2025, reflecting the operational maturity of vertical landing booster rockets.

- Fully reusable configurations are forecast to grow at a 12.0% CAGR through 2035, as Starship-class vehicles advance low-cost orbital access technology.

• By Payload Class

- Medium payloads (2,000–20,000 kg) represented 56.8% of the reusable launch vehicles market in 2025.

- Heavy-payload missions are forecast to grow at a 9.8% CAGR as deep-space and station-resupply missions accelerate.

• By Geography

- North America led with 77.5% share of the reusable launch vehicles market in 2025.

- Asia-Pacific is projected to register the fastest growth at a 19.0% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market sizing is constructed using bottom-up revenue models using launch service provider contracts, government procurement databases and commercial manifest research. Historical data (2021-2024) is sourced from certified financial statements and validated launch logs. Forecast data (2026-2035) is based on Market Research Future (MRFR)’s unique demand-supply equilibrium framework calibrated to a CAGR of 8.70%.