RF Test Equipment Market Summary

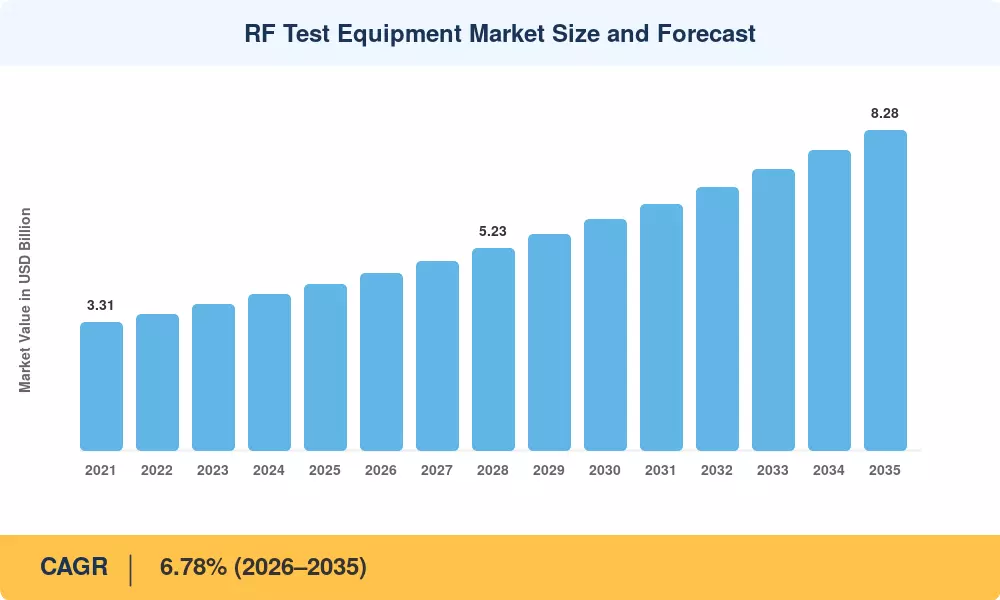

The RF Test Equipment Market reached an estimated USD 4.30 billion in 2025 and is projected to grow from USD 4.59 billion in 2026 to USD 8.28 billion by 2035, registering a CAGR of 6.78% across the forecast window. Two structural catalysts underpin this trajectory: the global push toward millimeter-wave 5G infrastructure—where over 4.7 million commercial base stations in China alone demand continuous RF signal measurement devices for massive-MIMO validation [1]—and the rapid proliferation of automotive radar operating in the 77–81 GHz band, which requires precise spectrum analyzer instruments for type-approval testing [8].

A generational technology transition is changing the nature of procurement cycles. Legacy analog benchtop analyzers are being replaced by software-defined modular platforms that combine several radio frequency test equipment in a single chassis. The 3GPP Release 19 requirements for Europe, approved in late 2025, reduced benchtop renewal cycles to less than twelve months, accelerating platform obsolescence and forcing capital expenditure towards reconfigurable microwave RF tests [1][5]. Wi-Fi 7, satellite-direct-to-device, and O-RAN disaggregated architectures are generating incremental revenue streams that didn’t exist five years ago for wireless protocol test equipment.

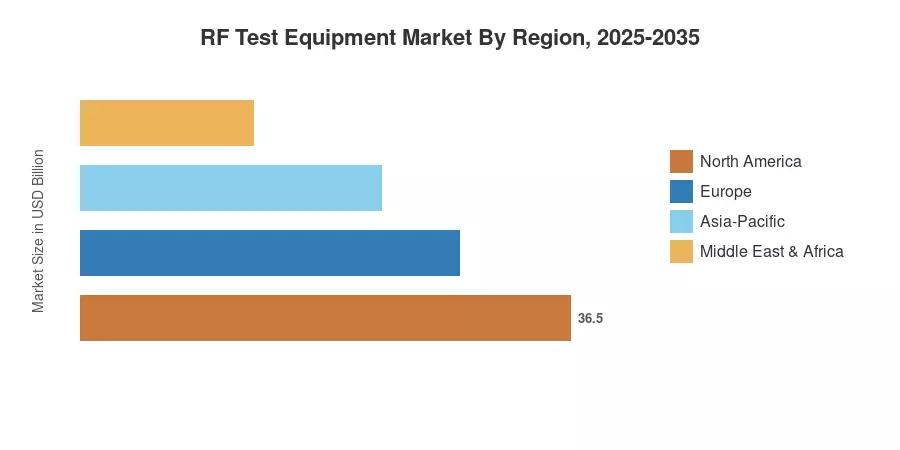

North America has the largest share of 38.3% of 2025 revenue, driven by FCC C-band interference requirements and DoD electromagnetic-spectrum upgrade spending [2][19]. Asia-Pacific is the fastest expanding market with an 8.3% CAGR driven by China’s FR2 deployment ambitions and India’s 5G densification push. The second greatest proportion is in Europe, with 24.2 % backed by the EU’s Digital Decade Program and the implementation of V-band standards [6][18]. Double-digit growth is anticipated for the RF Test Equipment Market across regional pockets through the 2030s.

Key Report Takeaways

• By Type

- Traditional GP instrumentation held a 34.8% revenue share in 2025, anchored by recurring calibration and compliance workflows across telecom labs.

- Modular GP instrumentation is expanding at an 8.4% CAGR through 2035, driven by demand for reconfigurable microwave RF testers.

• By Form Factor

- Benchtop instruments captured 37.6% of the RF Test Equipment Market in 2025, reflecting installed-base dominance in calibration centers.

- Modular platforms are projected to expand at a significant CAGR through 2031.

• By Geography

- North America led the RF Test Equipment Market with 38.3% share, supported by C-band spectrum compliance testing requirements.

- Asia-Pacific is on track for the fastest 8.3% CAGR, spurred by private 5G network rollouts and Ka-band satellite terminal validation.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) has designed a market-sizing model that combines top-down revenue analysis of publicly traded instrument vendors with bottom-up demand forecasts across verticals such as telecom, automotive, and aerospace. Historical data (2021-2024) are based on audited financial disclosures. Forecast figures (2026-2035) are based on calibrated growth assumptions confirmed against capital-expenditure pipelines, spectrum-auction schedules and standards-body release timetables.