Ring Main Unit Market Summary

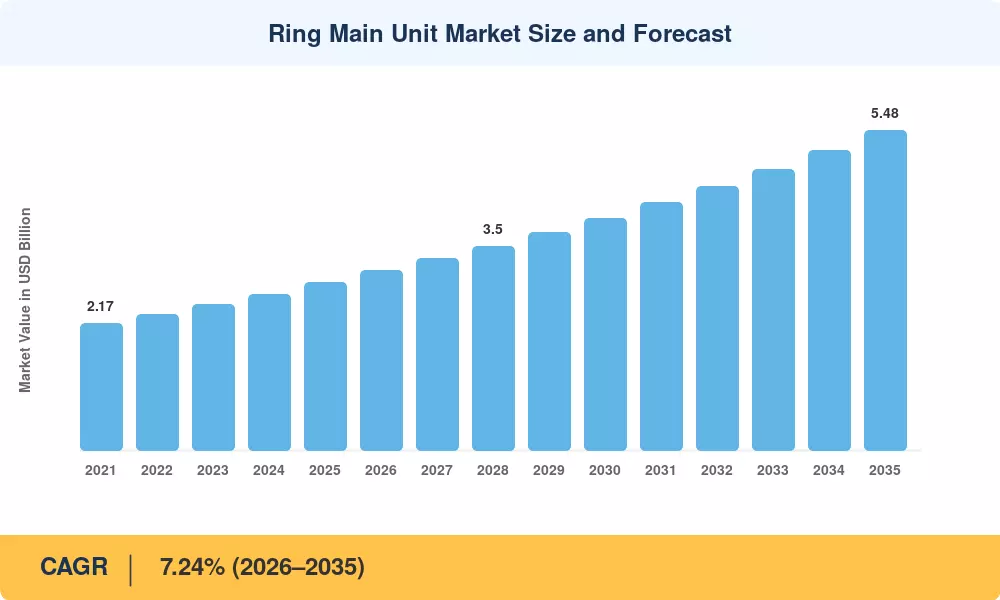

The Ring Main Unit Market reached an estimated USD 2.87 billion in 2025 and is projected to climb from USD 3.08 billion in 2026 to USD 5.48 billion by 2035, registering a CAGR of 7.24% across the forecast window. Two catalysts are accelerating procurement cycles: the European Union's revised F-Gas Regulation (EU) 2024/573, which phases down SF₆ use in medium-voltage switchgear starting 2026, and Asia-Pacific governments channeling over USD 320 billion into urban underground cabling programs through 2030[2]. These policy mandates are converting what was once a replacement-driven aftermarket into a front-loaded capital-expenditure cycle.

Technology transformation sits at the heart of the Ring Main Unit Market's growth story. Legacy oil-insulated and air-insulated compact RMU distribution network designs are giving way to SF6 free RMU switchgear vacuum platforms and solid insulated RMU SIS switchgear architectures that eliminate greenhouse-gas liabilities while shrinking footprint by up to 40% [3]. Siemens Energy's 2024 commitment of EUR 180 million toward vacuum-interrupter production capacity signals the scale of capital flowing into next-generation insulation [4]. Meanwhile, smart RMU remote control IEC 61850 communication modules are turning passive ring-main cabinets into network-aware nodes capable of fault isolation in under 200 milliseconds.

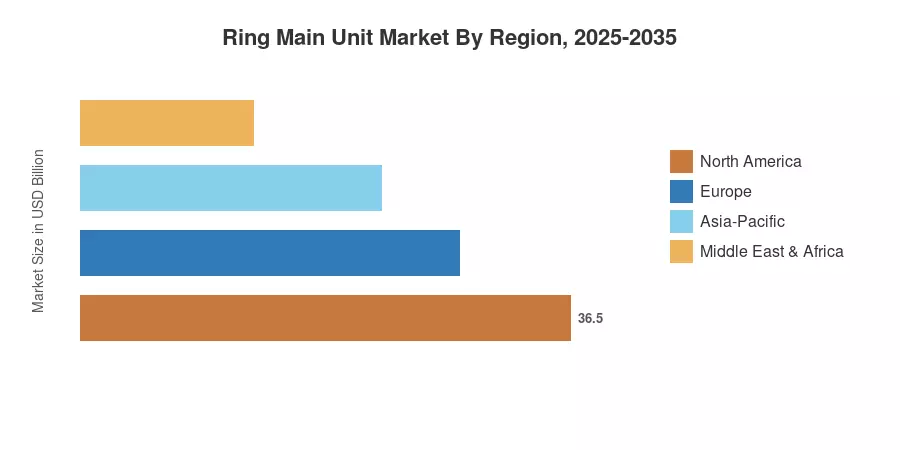

Asia-Pacific dominates the Ring Main Unit Market with roughly 46% of 2025 revenue, driven by China's State Grid underground feeder expansions and India's RDSS utility modernization scheme. The region is also the fastest-growing, forecast to compound at 9.1% through 2035. Europe holds the second-largest share at approximately 24%, propelled by the F-Gas phase-down and renewable collector-loop installations across the North Sea wind corridor

Key Report Takeaways

• By Insulation Type

- Gas-insulated configurations captured an estimated 62% of Ring Main Unit Market revenue in 2025, reflecting entrenched installed bases across mature grids

- SF6 free RMU switchgear vacuum and solid insulated RMU SIS switchgear variants are forecast to expand at a 10.3% CAGR through 2035, outpacing all other insulation categories

• By Installation

Outdoor RMU ring main outdoor enclosure units held a 61% share of 2025 shipments, favored for rural and peri-urban feeder loops

- Voltage

- The above-25 kV segment is set to grow at 8.3% CAGR, as renewable parks and data centers demand higher-voltage collector architectures

• By Automation

- Conventional manually operated units comprised 82% of 2025 Ring Main Unit Market shipments, yet smart RMU remote control IEC 61850 variants will register a 9.7% CAGR

- End User

- Distribution utilities commanded roughly USD 1.52 billion in 2025 revenue, while renewable energy and micro-grid developers represent the fastest-expanding end-user bracket

• By Region

- Asia-Pacific led all regions, accounting for 46% of 2025 sales in the Ring Main Unit Market

- South America is expected to reach USD 0.31 billion by 2035, aided by Brazil's PRODIST grid-code updates

Market Size and Forecast (2021–2035)

MRFR's market sizing employs a hybrid bottom-up/top-down methodology. Bottom-up estimates aggregate OEM shipment volumes, unit ASPs, and aftermarket service revenues across 42 countries. Top-down validation cross-references utility CAPEX disclosures, customs trade data (HS code 8537), and quarterly earnings from publicly listed switchgear manufacturers[5].

.webp?v=1783416353)