Rolling Stock Market Summary

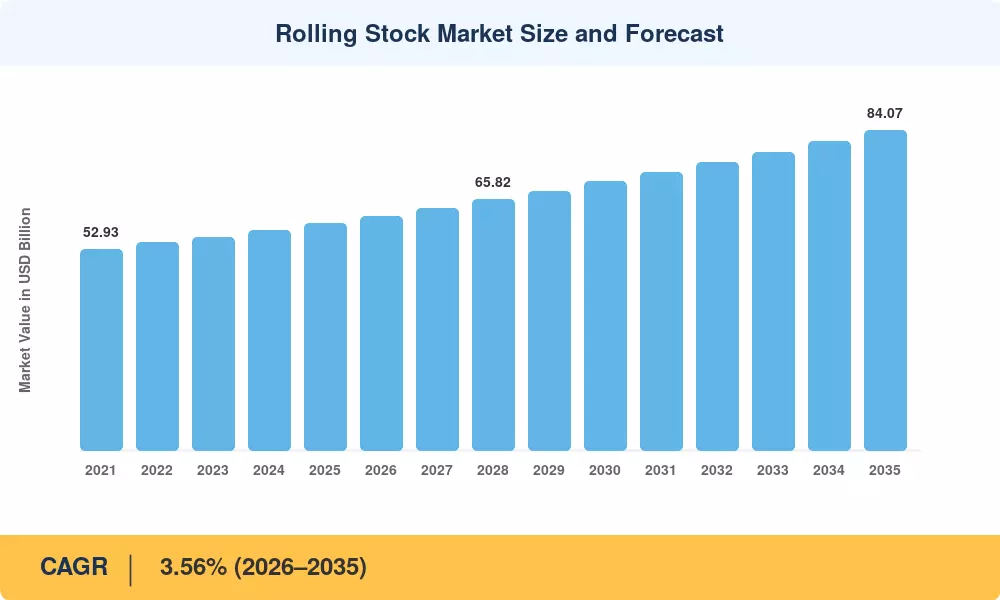

The Rolling Stock Market reached an estimated USD 59.68 billion in 2025 and is projected to climb from USD 61.38 billion in 2026 to USD 84.07 billion by 2035, registering a CAGR of 3.56% across the forecast window. Sovereign infrastructure investment plans remain the primary demand engine — China's 14th Five-Year Plan alone earmarked over USD 130 billion for rail network expansion through 2025, while the EU's Sustainable and Smart Mobility Strategy targets a doubling of high-speed rail traffic by 2030 [1][2]. Capital-intensive procurement cycles and multi-year fleet replacement programs mean order books stretch well beyond 12–18 months, insulating the Rolling Stock Market from short-term consumer demand fluctuations.

There is a dramatic digital change occurring in the way rail operators specify and acquire fleets. Decarbonization standards are ratcheting up, and legacy diesel traction is giving way to electric and battery-hybrid propulsion. For example, the European Green Deal’s Fit-for-55 package sets out a target of reducing transport emissions by 55% by 2030 compared to 1990 levels, and this is driving national operators to move towards electrified trainsets and lifecycle service contracts, where maintenance, spare parts and digital analytics are all bundled into single-source agreements [3]. Autonomous train operating technology – already proven on selected metro lines in Paris, Copenhagen and Singapore – is expanding to mainline applications, providing a digital overlay to what has typically been a heavy-engineering procurement category.

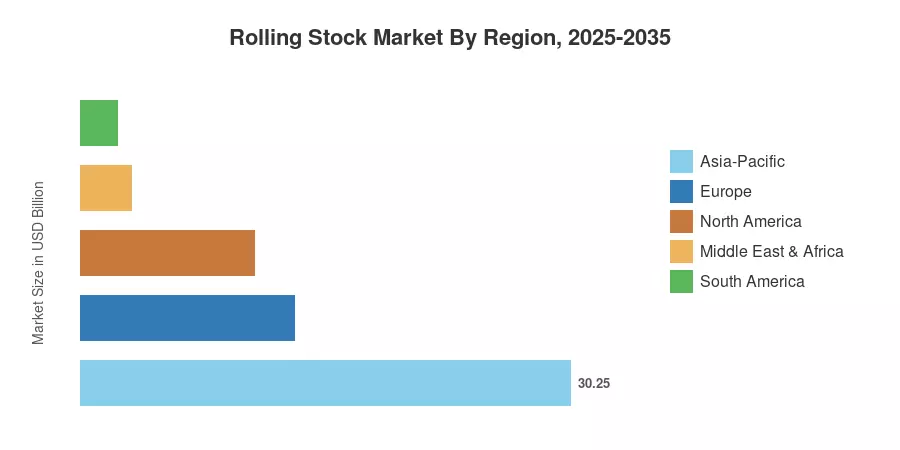

The Asia-Pacific region holds a share of over 50.68% in the Rolling Stock Market owing to the large-scale domestic manufacturing capabilities of China and the rapid development of metro and dedicated freight corridors in India. The Middle East & Africa region is the fastest-growing geography, growing at a 5.32% CAGR through 2035 as Gulf Cooperation Council states invest in inter-city rail lines and urban transportation systems. Europe has the second-highest share, with over 22%, mainly due to fleet renewal mandates and cross-border interoperability standards under the EU’s Fourth Railway Package [4]. The Rolling Stock Market is at an inflection moment where digital, environmental, and urbanization challenges are coming together to change fleet procurement methods around the world.

Key Report Takeaways

• By Type

- Passenger coaches captured approximately 72.15% of the Rolling Stock Market in 2025, reflecting heavy replacement demand across intercity and commuter corridors.

- Metros and light rail vehicles are expected to post the fastest expansion through 2035, driven by urbanization and municipal transit investment.

• By Propulsion

- Electric units accounted for 58.12% of the Rolling Stock Market in 2025, supported by mainline electrification programs in Europe and Asia.

- Diesel-powered fleets continue to serve freight-heavy corridors, though their share is declining year on year.

• By Application

- Passenger rail held a 59.17% share of the Rolling Stock Market in 2025 and remains the fastest-growing application segment.

• By Geography

- Asia-Pacific dominates the Rolling Stock Market with more than half of global revenue, while the Middle East & Africa posts the strongest regional CAGR.

Rolling Stock Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s size methodology blends bottom-up order-book data from OEM disclosures, national procurement agency budgets, and top-down macroeconomic rail-spend ratios. Historical numbers (2021-2024) are based on audited company revenues and government expenditure reports. Forecast forecasts are based on segment-level growth assumptions validated using sovereign transport investment pipelines.