Rubber Track Agricultural Equipment Market Summary

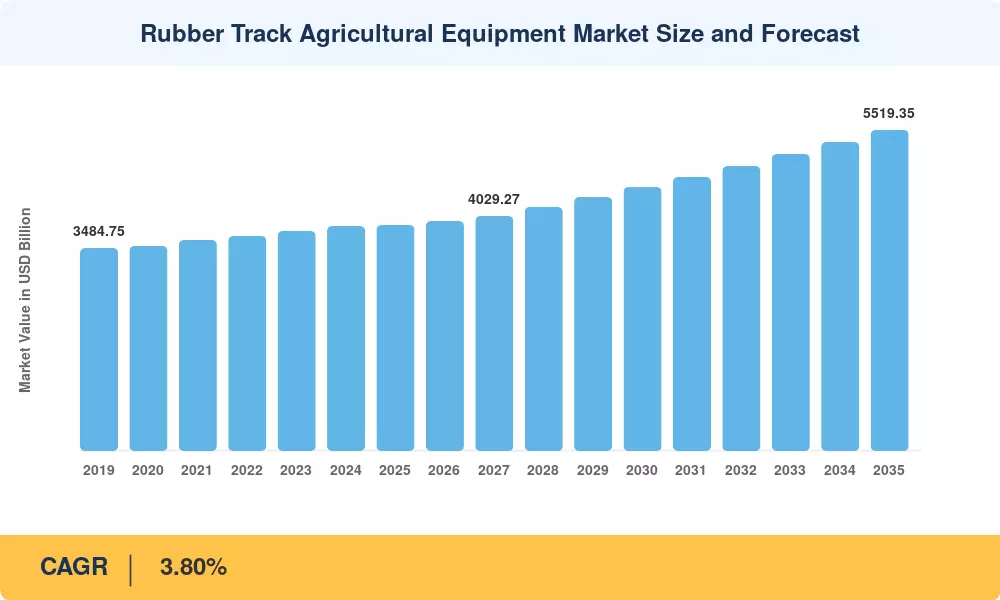

The global rubber track agricultural equipment market was valued at approximately USD 3,884.27 million in 2025 and is projected to reach USD 5,519.35 million by 2035, expanding at a compound annual growth rate (CAGR) of 3.80% during the forecast period of 2026–2035. The market's upward trajectory is underpinned by structural demand for high-efficiency, low-maintenance undercarriage systems in off-road agricultural machinery, growing adoption of rubber track platforms to enhance traction and reduce soil compaction within precision farming operations, and the sustained expansion of mechanized farming into regions characterized by challenging terrain conditions [2]. Investment in advanced land preparation and crop management technologies continued to accelerate through 2025, as original equipment manufacturers (OEMs) introduced electric drive powertrains, autonomous guidance capabilities, and expanded sprayer platforms designed for large-scale field operations, collectively reinforcing the shift toward track-based mobility in modern agriculture [3].

Due to their adaptability to row crop, broadacre, and mixed-use farming operations, rubber-track-equipped tractors continue to be the market's dominant equipment segment, accounting for the biggest revenue share in 2025. Because of their better load distribution and lower ground pressure characteristics when compared to segmented alternatives, continuous rubber tracks are the most popular track layout in terms of value. Wetland and specialty farming, where rubber tracks offer essential flotation and low soil disturbance in saturated or environmentally sensitive terrains, is the application segment with the quickest pace of growth. The convergence of track-based machinery with digital and electrified farming systems is highlighted by significant industry developments in early 2026, such as Caterpillar's introduction of the Cat D8 XE dozer with an electric drive powertrain and New Holland's introduction of the Defensor 4000 sprayer with precision agriculture integration [4].

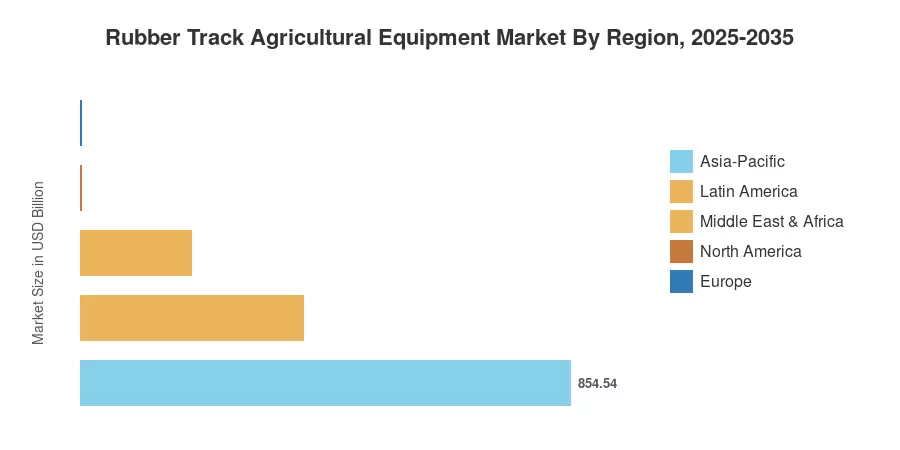

Due to widespread mechanized farming in Germany, France, and the UK, as well as strict soil health rules that encourage low-compaction track systems, Europe maintained its position as the leading regional market in 2025 and commanded the biggest part of worldwide revenues. Due to widespread precision agriculture use in the US and Canada, as well as rising replacement demand for rubber track systems in the Midwest grain belt, North America emerged as the fastest-growing regional market, with a compound annual growth rate (CAGR) above the global average. China, Japan, and Australia are the main demand centers in Asia-Pacific, which is the third-largest regional market. As digital agriculture, autonomous machinery integration, and regulatory emphasis on soil conservation come together to drive rubber track penetration across global farming operations, the market is anticipated to maintain its growth momentum through 2035 [5].

Key Report Takeaways

| Segment Dimension | Key Metric | Notes |

| Equipment Type — Dominant | Tractors: USD 1,747.92 Mn (2025) | Largest revenue contributor; versatile across farming operations |

| Equipment Type — Fastest Growing | Sprayers: CAGR 4.50% (2026–2035) | Driven by precision agriculture adoption and large-scale field spraying demand |

| Track Type — Dominant | Continuous Rubber Tracks: USD 2,408.25 Mn (2025) | Superior load distribution and soil protection characteristics |

| Track Type — Fastest Growing | Segmented Rubber Tracks: CAGR 4.20% (2026–2035) | Gaining share in retrofit and specialty equipment segments |

| Application — Dominant | Crop Farming: USD 2,136.35 Mn (2025) | Core demand driver across all major farming regions |

| Application — Fastest Growing | Wetland & Specialty Farming: CAGR 4.80% (2026–2035) | Niche growth in orchards, vineyards, and saturated-terrain operations |

| End User — Dominant | Large-Scale Commercial Farms: USD 1,942.14 Mn (2025) | Driven by capital expenditure cycles and fleet modernization |

| End User — Fastest Growing | Agricultural Service Contractors: CAGR 4.40% (2026–2035) | Contractor fleet expansion and utilization-based purchasing models |

| Region — Dominant | Europe: USD 1,359.49 Mn (2025) | Supported by soil health regulation and advanced mechanization |

| Region — Fastest Growing | North America: CAGR 4.30% (2026–2035) | Precision agriculture adoption and Midwest grain belt demand |

Market Size and Forecast (2019–2035)

The market size estimates presented in this report are derived from MRFR's proprietary bottom-up research methodology, integrating primary data from OEM financial disclosures, distributor surveys, and agricultural machinery trade association filings with secondary data from government agricultural mechanization reports, industry journals, and regional import-export databases. Historical values (2019–2024) reflect verified shipment and revenue data, while the base year (2025) is estimated from the most recent available 12-month period. Forecast values (2026–2035) are projected using demand-side modeling that incorporates macroeconomic indicators, crop acreage trends, equipment replacement cycles, and policy developments across major farming economies [6].