Server Storage Area Network Market Summary

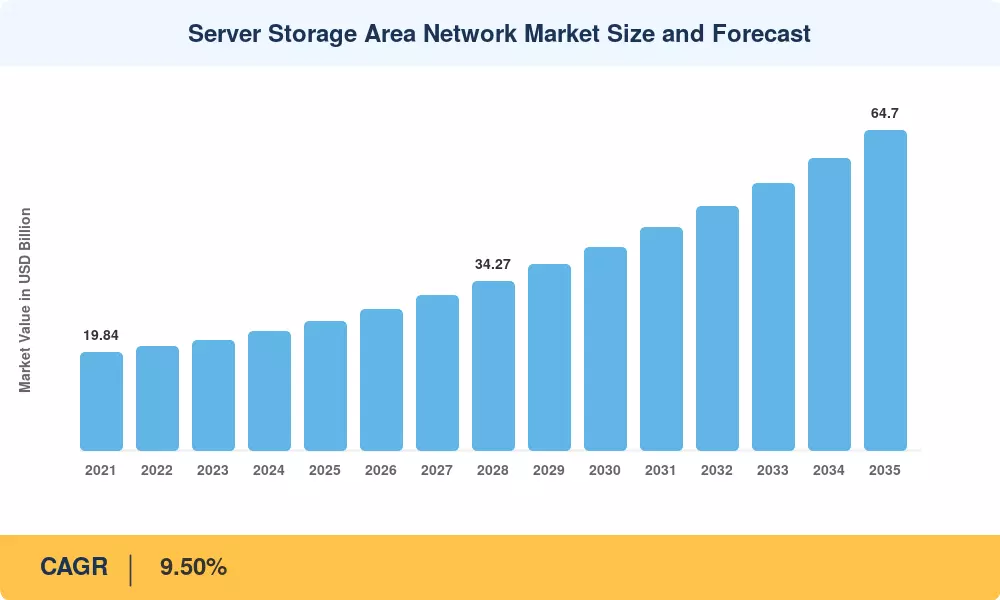

The Server Storage Area Network Market reached USD 26.10 Billion in 2025 and is projected to climb from USD 28.58 Billion in 2026 to USD 64.70 Billion by 2035, registering a 9.50% CAGR during the forecast period. Hyperscale data-center capital expenditure — which topped USD 260 Billion globally in 2024 according to Synergy Research Group [1] — remains the single largest catalyst, as every new AI training cluster and cloud availability zone demands high-throughput, low-latency block storage fabrics. Simultaneously, government digital-infrastructure mandates such as the EU's Digital Decade program and India's Digital India initiative are channeling public funds into enterprise-grade networking overhauls that directly benefit storage area network deployments.

A technology inflection is reshaping the Server Storage Area Network Market from the ground up. Legacy 16 Gbps Fibre Channel fabrics are giving way to 64 Gbps and 128 Gbps generations, while NVMe-over-Fabrics is collapsing the latency gap between direct-attached and networked storage to single-digit microseconds. Vendors are layering computational storage engines, CXL-enabled memory pooling, and software-defined orchestration into unified platforms — blurring the boundary between compute and storage domains. estimates that by 2027, over 40% of new SAN deployments will be software-defined [2], a shift that accelerates refresh cycles and pulls services revenue forward.

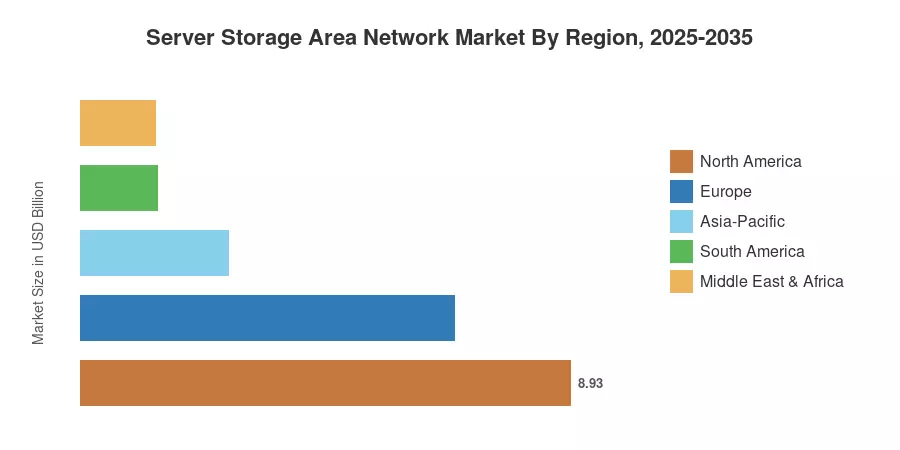

North America commanded roughly 34.2% of the Server Storage Area Network Market in 2024, propelled by U.S. hyperscaler spend and federal data-sovereignty requirements. Asia-Pacific is advancing at the fastest clip — a 10.30% CAGR through 2035 — driven by sovereign-cloud buildouts across China, India, and ASEAN nations. Europe held the second-largest share at approximately 26.1%, anchored by GDPR-driven data-localization and banking-sector modernization programs. As AI workloads, edge computing, and consumption-based procurement converge, the Server Storage Area Network Market is entering its most dynamic decade since the original Fibre Channel standardization era.

Key Report Takeaways

• By Product Type

- Hardware accounted for roughly 42.5% of Server Storage Area Network Market revenue in 2024, underpinned by continued demand for high-port-count directors and all-flash arrays.

- Services are poised to register the fastest segment CAGR of approximately 12.10% through 2035 as enterprises shift to consumption-based managed-SAN offerings.

• By Technology

- Fibre Channel retained the leading technology share in 2024, valued at an estimated USD 11.18 Billion.

- NVMe-over-Fabrics is projected to expand at a 11.50% CAGR through 2035 as AI inference clusters demand sub-10-microsecond latency.

• By Organization Size

- Large enterprises represented approximately 58.8% of the Server Storage Area Network Market in 2024.

- Small and medium enterprises are growing fastest, with a CAGR near 13.40% as cloud-managed SAN appliances lower entry barriers.

• By End-User Industry

- BFSI captured roughly 23.4% of the Server Storage Area Network Market revenue in 2024, driven by real-time transaction processing and regulatory archiving requirements.

- Cloud service providers are forecast to post the highest end-user CAGR of approximately 10.60% through 2035.

• By Region

- North America led the Server Storage Area Network Market with a 34.2% share in 2024.

- Asia-Pacific is the fastest-growing region, advancing at a 10.30% CAGR.

Market Size and Forecast (2021–2035)

Market Research Future's estimates integrate primary interviews with storage OEMs, channel partners, and enterprise CIOs alongside secondary data from vendor earnings disclosures, infrastructure spending trackers, and government procurement databases. Historical values (2021–2024) reflect actual shipment and revenue data; the forecast (2026–2035) uses a bottom-up model calibrated to workload growth projections, technology migration curves, and regional capital-expenditure plans.