Shrimp Market Summary

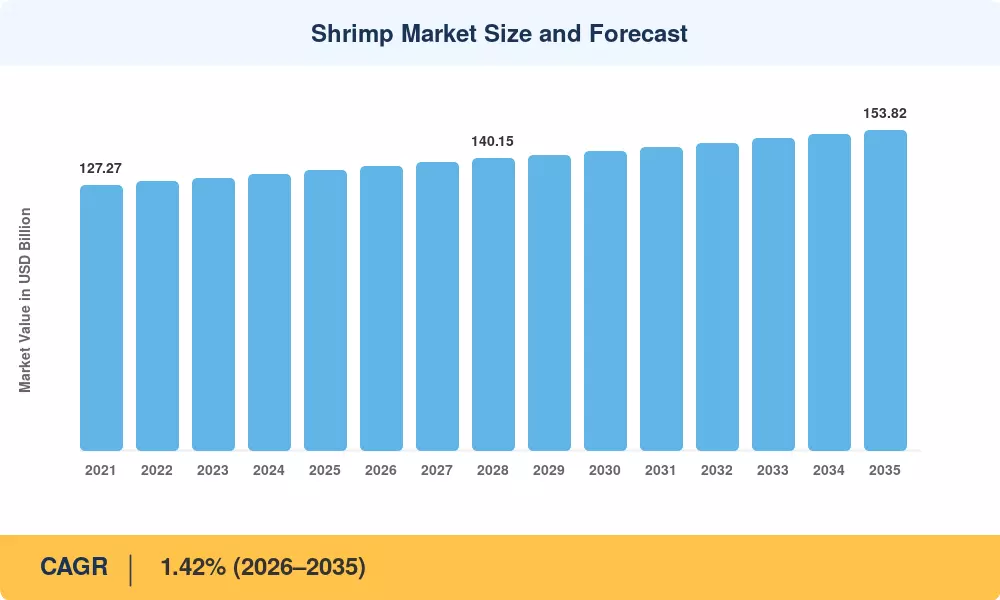

The global Shrimp Market stood at USD 134.67 billion in 2025 and is projected to reach USD 136.58 billion in 2026 before climbing to USD 153.82 billion by 2035, registering a CAGR of 1.42% during the forecast period. Rising per-capita seafood consumption in Asia-Pacific — where governments have rolled out multi-billion-dollar aquaculture modernization programs — and growing demand for peeled and deveined shrimp across Western foodservice channels are the two structural forces propelling this trajectory[2].

A fundamental shift is underway in how shrimp reach the consumer's plate. Land-based recirculating aquaculture systems (RAS) are displacing traditional open-pond operations, driven by climate volatility and the spread of early-mortality syndrome across Southeast Asian farms. Thailand's Department of Fisheries committed approximately USD 420 million between 2023 and 2026 to subsidize RAS conversions, while Ecuador's shrimp aquaculture production capacity expanded 11% year-on-year in 2024 through vertically integrated hatchery-to-export corridors [3][4].

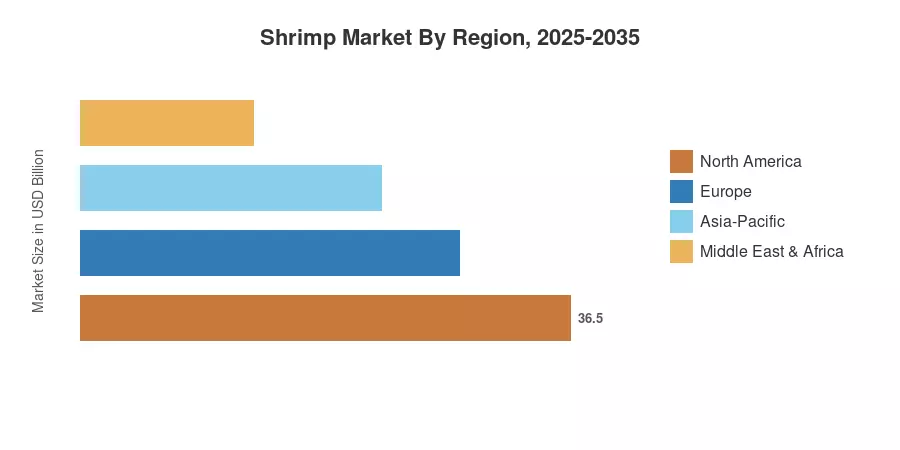

Asia-Pacific commands roughly 48.4% of the global Shrimp Market revenue, anchored by China, India, and Vietnam. Europe is the fastest-growing region at an estimated 2.36% CAGR through 2035, fueled by sustainability-focused procurement mandates and rising consumer preference for frozen and fresh shrimp products. North America retains the second-largest share at approximately 21%, where foodservice recovery and retail expansion of white and black tiger shrimp products continue to drive imports. The decade ahead will be shaped by traceability technologies and shifting trade flows as farmed and wild-caught shrimp supply chains reconfigure around ESG benchmarks [5][6].

Key Report Takeaways

• By Species

- Pink shrimp accounted for 42.3% of the Shrimp Market in 2025, led by large-scale farmed and wild-caught shrimp harvests across the Gulf of Mexico and Indian Ocean corridors

- Tiger shrimp — including white and black tiger shrimp varieties — are projected to expand at a 2.55% CAGR through 2035 as improved hatchery genetics boost survival rates

• By Form

- Frozen and fresh shrimp in the frozen segment captured 59.8% of the Shrimp Market share in 2025, reflecting cold-chain infrastructure maturation across Asia-Pacific

- Canned shrimp products are forecast to grow at a 3.95% CAGR, driven by shelf-stable convenience trends in emerging economies

• By Source

- Farmed shrimp supplied 55.8% of global volume in the Shrimp Market, with shrimp aquaculture production expanding in Ecuador and India

- Wild-caught shrimp output is set to rise at a 3.40% CAGR, maintaining a premium among quality-conscious buyers in Europe and Japan

• By Distribution Channel

- On-trade channels retained 58.7% share in 2025, though off-trade retail of peeled and deveined shrimp is accelerating at a 2.65% CAGR

• By Region

- Asia-Pacific commanded 48.4% of the 2025 Shrimp Market revenue

- Europe is poised for the fastest expansion at a 2.36% CAGR to 2035

Market Size and Forecast (2021–2035)

MRFR's valuation model combines FAO production statistics, national customs trade data, processor-level revenue disclosures, and proprietary demand surveys across 32 countries. Historical figures (2021–2024) are reconciled against published export/import volumes, while forecast values (2026–2035) are generated through econometric demand modeling calibrated to GDP growth, protein substitution elasticity, and aquaculture capacity expansion timelines.