Simulation Software Market Summary

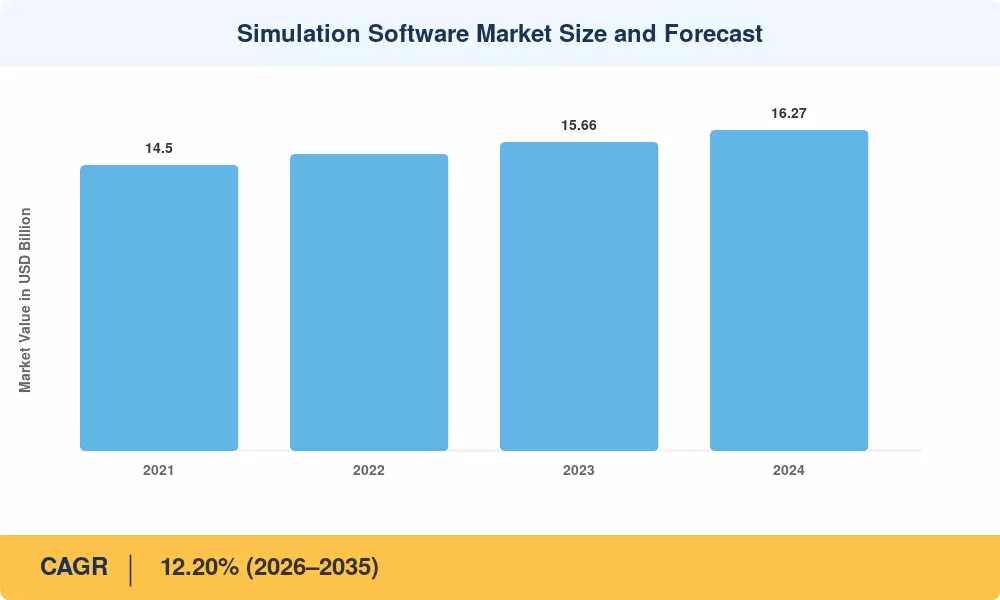

The Simulation Software Market reached an estimated USD 14.50 billion in 2025, entering the forecast period at USD 16.27 Billion in 2026 and projected to climb to USD 45.85 billion by 2035 at a 12.20% CAGR. Two forces are compressing adoption timelines across industries: first, regulatory mandates for virtual sustainability assessments — the EU's Corporate Sustainability Reporting Directive now treats digital twin simulation outputs as acceptable evidence for lifecycle impact disclosures [2]. Second, hyperscale cloud providers invested more than USD 9.8 billion in HPC-as-a-service capacity during 2024 alone, lowering the barrier for mid-market manufacturers who previously lacked dedicated solver infrastructure [3].

There is a structural change in technology. Cloud-native CAE simulation platforms with GPU-accelerated solvers and AI-driven surrogate models are replacing outdated on-premises finite-element and computational-fluid-dynamics stacks that operated on proprietary Unix clusters. In 2024, Siemens, Ansys, and Dassault Systèmes all reported yearly R&D budgets over USD 1.2 billion, with a large portion of that money going toward the integration of engineering simulation tools into unified product-lifecycle platforms [4]. Multi-physics coupling, which previously required weeks of manual mesh preparation, is now handled by virtual prototyping tools.

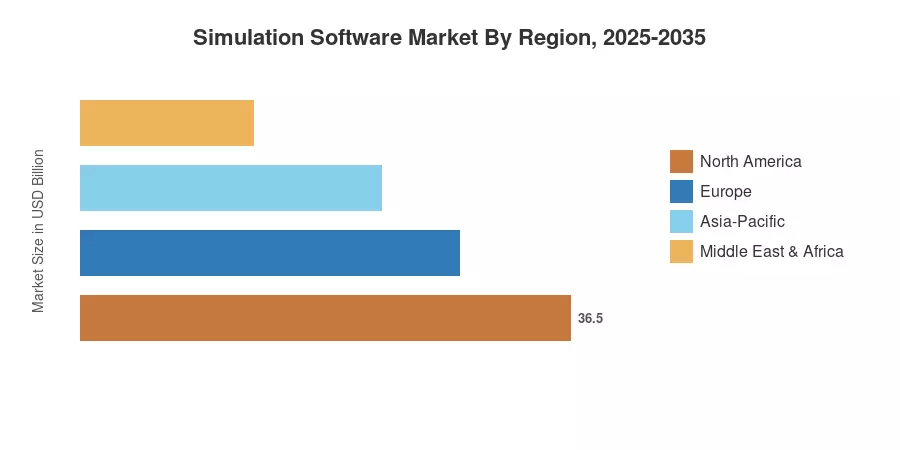

North America's defense and semiconductor projects account for about 33.5% of the world's revenue. With a predicted CAGR of 13.40%, Asia-Pacific is the fastest-growing market due to China's "Simulation-Industrialization 2025" strategy and India's developing automotive R&D facilities. Due to Industrie 4.0 directives and EU Green Deal compliance requirements, Europe has the second-largest stake at about 27.0%. As pay-as-you-go solvers democratize access beyond Tier-1 OEMs, the simulation software market is about to enter its broadest adoption phase.

Key Report Takeaways

• By Simulation Type

- Computational fluid dynamics captured an estimated 29.8% of 2025 revenue, reflecting heavy aerospace and automotive aerodynamic-optimization demand.

- Discrete-event and process simulation is the fastest-growing type at a projected 15.10% CAGR, fueled by supply-chain digital twin simulation deployments.

• By End-User Industry

- The automotive sector led the Simulation Software Market in 2025 with a 30.5% revenue share, as OEMs rely on 3D modeling simulation for crash-test and NVH validation.

- Healthcare and life sciences are forecast to expand at a 12.50% CAGR, driven by computational drug-discovery and medical-device virtual prototyping software.

• By Regional

- North America remained the dominant region, generating an estimated USD 4.86 billion in 2025 Simulation Software Market revenue.

- Asia-Pacific is poised to grow at a 13.40% CAGR, propelled by government-subsidized CAE simulation platforms adoption across China, India, and South Korea.

Simulation Software Market Size and Forecast (2021–2035)

Market sizing draws on bottom-up revenue analysis of licensed software, platform subscriptions, and professional services across 22 end-use verticals, cross-validated against vendor earnings disclosures and MRFR's proprietary demand model.