Small Modular Reactor Market Summary

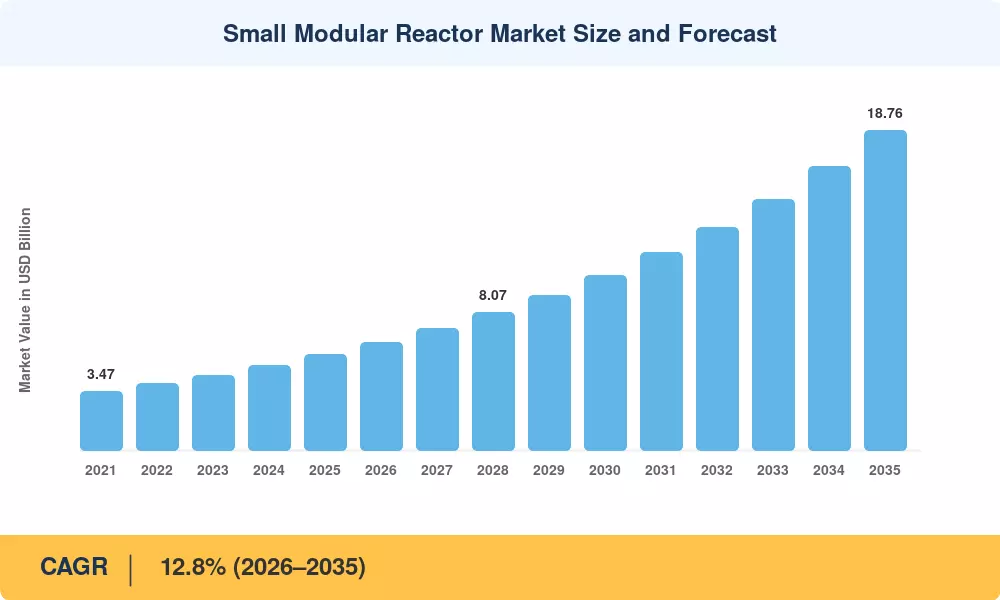

The Small Modular Reactor Market reached an estimated USD 5.62 billion in 2025 and is projected to grow from USD 6.34 billion in 2026 to USD 18.76 billion by 2035, registering a CAGR of 12.8% across the forecast period. This expansion tracks directly to sovereign energy security mandates and corporate net-zero commitments that have converted from pledges into funded procurement. The U.S. Department of Energy's USD 3.2 billion Advanced Reactor Demonstration Program, alongside the UK's Great British Nuclear initiative earmarking GBP 20 billion for new nuclear capacity, has created an investable pipeline that did not exist five years ago [1][2].

A generational shift in nuclear technology is underway. Legacy gigawatt-scale plants — averaging 12–15 years from groundbreaking to grid connection — are giving way to factory-fabricated units under 300 MWe that can be transported by rail and assembled on-site within 24–36 months. The International Energy Agency projects that global nuclear capacity must double by 2050 to meet Paris Agreement targets, and small modular designs represent the fastest credible path to that doubling [3].

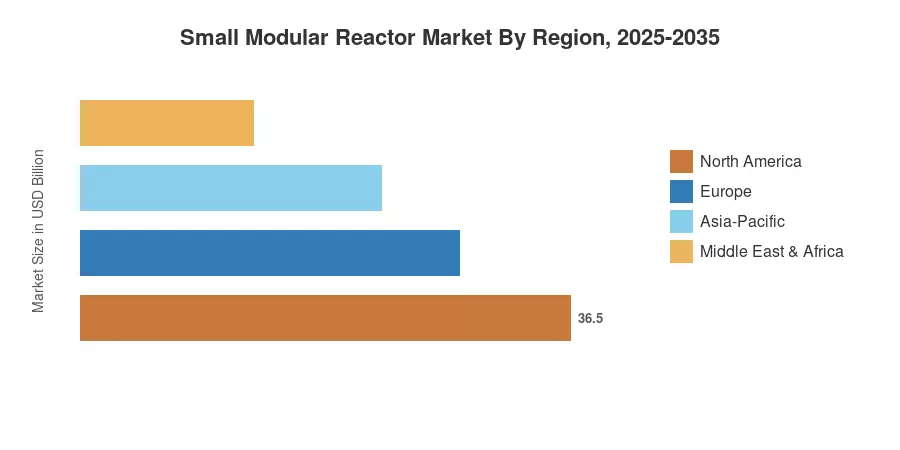

North America commands roughly 38% of the Small Modular Reactor Market, anchored by advanced design certifications and federal tax credits under the Inflation Reduction Act. Asia-Pacific is the fastest-growing region at an estimated 15.2% CAGR, driven by China's aggressive deployment of demonstration units and India's fleet-based SMR roadmap. Europe holds a 27% share, with the UK and France leading new build commitments. The decade ahead will be defined less by technology risk and more by supply-chain readiness and regulatory throughput [4][5].

Key Report Takeaways

• By Reactor Technology

- Light-water SMR designs account for approximately 52% of the Small Modular Reactor Market, reflecting the maturity of pressurized-water architectures and their licensing familiarity with regulatory bodies.

- High-temperature gas-cooled reactor concepts are growing at the fastest segment CAGR of 16.4%, fueled by demand for industrial process heat above 700°C.

- Molten salt reactor designs represent approximately USD 0.79 billion in 2025, attracting investment for their passive safety and fuel flexibility characteristics.

• By Application

- Electricity generation remains the primary demand driver, capturing 58% of deployments across the Small Modular Reactor Market as utilities seek dispatchable low-carbon baseload.

- Industrial heat applications are recording a CAGR of 14.9%, propelled by decarbonization targets in the steel, cement, and petrochemical industries.

• By Region

- North America holds the leading share at 38%, underpinned by the largest pipeline of licensed and pre-licensed designs globally.

- Asia-Pacific is forecast to reach USD 5.28 billion by 2035, with China operating demonstration reactors and South Korea advancing export-oriented designs.

- Europe holds a 27% share, driven by the UK's GBN selection process and France's restart of its national SMR program.

Small Modular Reactor Market Size and Forecast (2021–2035)

Market sizing draws on bottom-up project-pipeline analysis across 47 SMR design programs tracked globally, cross-referenced with top-down utility capital expenditure disclosures and government allocation data. Historical figures (2021–2024) reflect reported contract values, federal disbursements, and vendor revenue. Forecast values (2026–2035) incorporate probabilistic deployment schedules, regulatory timeline assumptions, and learning-rate cost reductions benchmarked to IEA and DOE projections [3].