Small UAV Market Summary

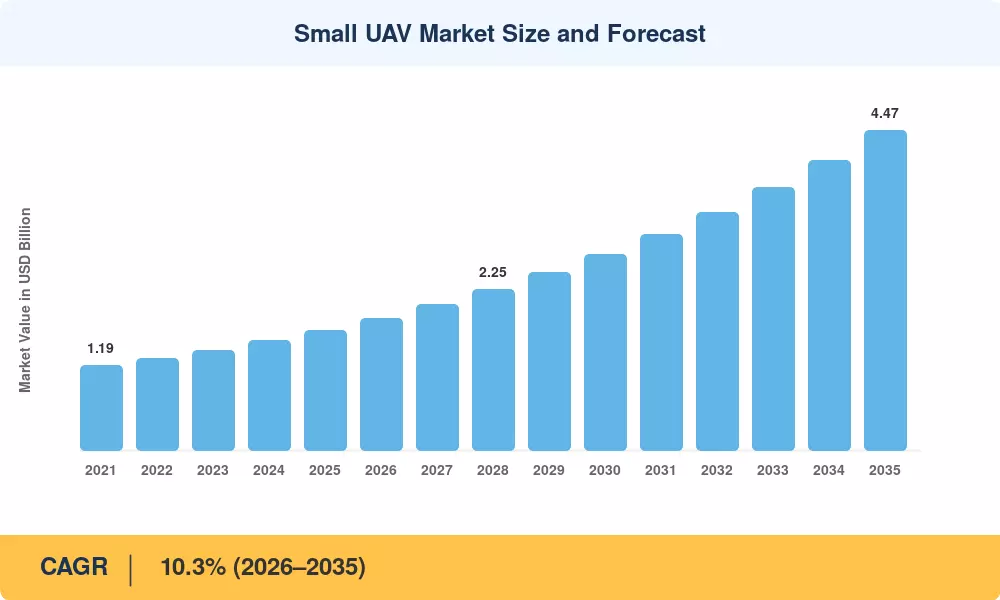

The Small UAV Market reached an estimated USD 1.68 Billion in 2025 and is projected to grow from USD 1.85 Billion in 2026 to USD 4.47 Billion by 2035, registering a compound annual growth rate of 10.3% during the forecast period. Pentagon budgets exceeding USD 2.3 billion annually for unmanned systems procurement and NATO's multinational small drone acquisition programs serve as twin engines propelling this expansion [1][2]. Demand is no longer confined to intelligence gathering — loitering munitions validated across Eastern European battlefields have permanently expanded the addressable mission envelope for the Small UAV Market.

A structural technology shift is underway. Crewed tactical reconnaissance platforms that once cost USD 15–25 million per airframe are giving way to expendable unmanned systems priced below USD 250,000, slashing mission costs by more than 90% [3]. Hybrid vertical-takeoff-and-landing designs are eroding the dominance of traditional fixed-wing airframes by removing runway dependencies and cutting launch cycle times to under five minutes. Battery-electric propulsion now powers the majority of fielded platforms, though fuel-cell powertrains are closing the endurance gap and attracting fresh defense R&D funding across the United States, Israel, and South Korea [4].

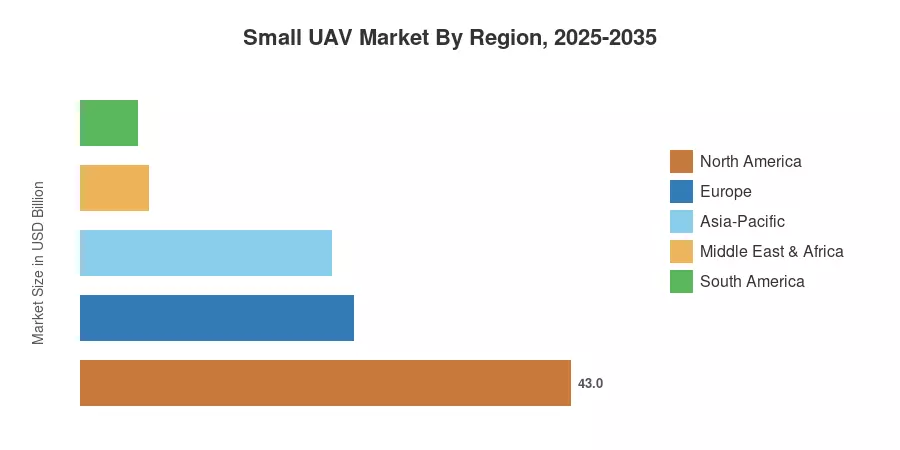

North America commands roughly 43% of global Small UAV Market revenue, anchored by sustained U.S. Department of Defense spending and a mature domestic supply chain. Asia-Pacific is the fastest-growing region with an estimated 11.5% CAGR through 2035, as indigenous production programs in China, India, and South Korea reduce dependence on Western suppliers. Europe holds approximately 24% of the market, driven by Ukrainian conflict-era procurement cycles and pan-EU defense integration initiatives. The competitive landscape will continue to intensify as dual-use commercial and military demand converge across all regions through the end of the decade.

Key Report Takeaways

• By Wing Type

- Fixed-wing platforms accounted for approximately 57% of the Small UAV Market share in 2025, benefiting from superior endurance and payload capacity for ISR missions.

- Hybrid vertical-takeoff designs are projected to expand at the fastest pace through 2035, reflecting military preference for runway-independent launch capability.

• By Application

- Intelligence, surveillance, and reconnaissance missions generated roughly 60% of total revenue in 2025, maintaining their position as the primary demand driver for the Small UAV Market.

- Combat roles deploying loitering munitions are recording the highest growth rate, validated by frontline performance in Ukraine and the Caucasus.

• By Region

- North America led with a 43% share in 2025, supported by unmatched Pentagon procurement budgets.

- Asia-Pacific posted the highest regional growth rate in the Small UAV Market, driven by China's indigenous drone industrial base and India's defense modernization roadmap.

Market Size and Forecast (2021–2035)

Market Research Future's Small UAV Market estimates are derived from a bottom-up revenue model combining platform unit shipments, average selling prices by weight class, aftermarket services, and payload attachment revenues. Historical data draws on verified defense procurement databases, trade publications, and manufacturer annual filings, while forecast-period projections apply segment-level growth assumptions validated against government budget trajectories and order backlog disclosures [5][6].

.webp?v=1783938003)