Smart Electric Meters Market Summary

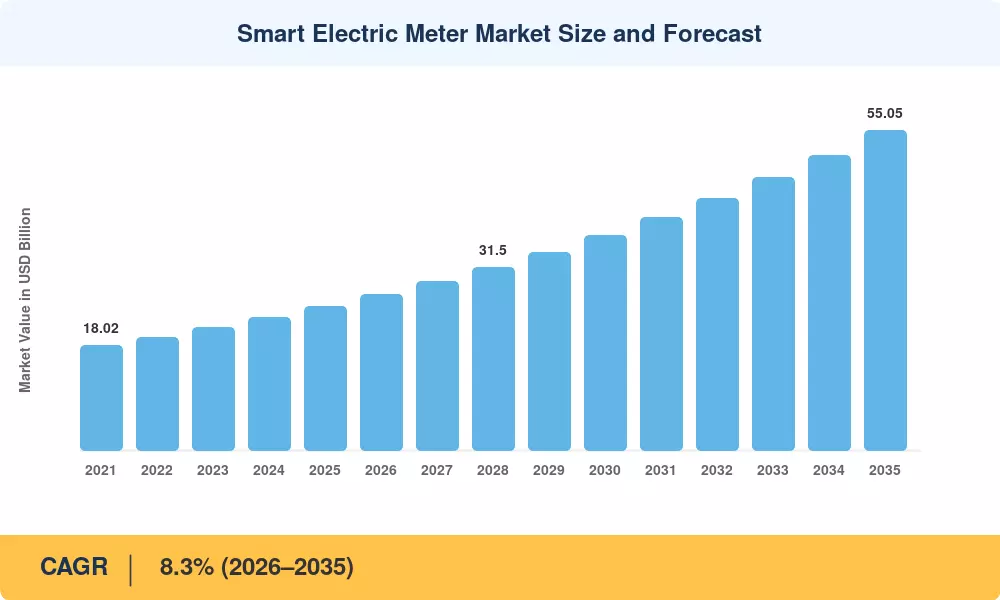

The global Smart Electric Meter Market stood at USD 24.80 billion in 2025, with the forecast trajectory projecting a rise from USD 26.86 billion in 2026 to approximately USD 55.05 billion by 2035, reflecting a compound annual growth rate of 8.3% across the 2026–2035 window. Two catalysts anchor this expansion: first, binding government mandates for AMI smart electricity meter rollout in the European Union, China, and India that collectively cover more than 1.2 billion connection points [2]; second, the global smart grid investment surge that exceeded USD 45 billion annually in 2024, channeling billions specifically toward metering infrastructure [3]. The Smart Electric Meter Market is entering a phase where utility spending is shifting decisively from pilot programs to full-scale fleet replacements.

Legacy electromechanical and first-generation electronic meters—many installed during the 1990s and early 2000s—are reaching end-of-life, accelerating a migration toward two-way communicating meters equipped with PLC RF mesh smart meter communication capabilities and advanced cybersecurity modules. The U.S. Department of Energy's Grid Modernization Initiative alone earmarked USD 3.5 billion for distribution-level upgrades in 2023–2025, a significant share of which flows into AMI smart electricity meter rollout programs [4]. Smart meter tamper detection alert functionality is also becoming a procurement requirement, as utilities globally report non-technical losses costing an estimated USD 96 billion per year [5].

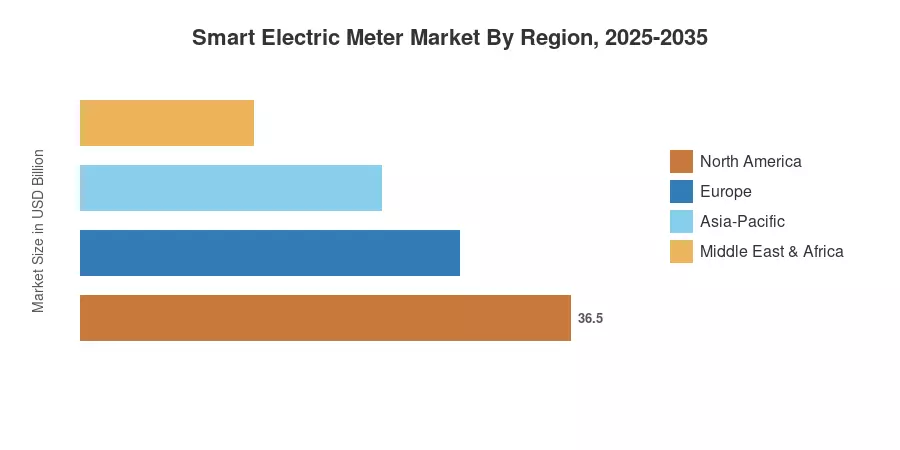

Asia-Pacific commands the dominant position in the Smart Electric Meter Market with roughly 38% revenue share, powered by China's State Grid having already deployed over 600 million units and India targeting 250 million smart prepaid meters under its RDSS scheme [6]. The Middle East & Africa region emerges as the fastest-growing geography at approximately 11.5% CAGR, driven by Saudi Arabia's SEC smart meter program and South Africa's revenue-protection imperative. Europe holds the second-largest share (~25%), propelled by the SMETS2 UK smart meter standard and the EU's mandate under the Clean Energy Package requiring 80% household penetration by 2030 [7]. The Smart Electric Meter Market looks set to maintain high single-digit growth as grid decarbonization and electrification agendas intensify globally through 2035.

Key Report Takeaways

• By Communication Technology

- PLC-based meters capture the largest technology share of the Smart Electric Meter Market at approximately 35%, reflecting strong adoption in dense urban deployments across Europe and China

- RF mesh architectures are expanding at a CAGR of ~9.6%, supported by North American utilities preferring PLC RF mesh smart meter communication networks for suburban and semi-rural geographies

- Cellular-connected meters (4G/LTE-M and NB-IoT) account for roughly USD 5.46 billion in 2025 revenue, gaining share as mobile network operators offer dedicated utility IoT tariffs

• By End User

- Residential metering constitutes ~55% of Smart Electric Meter Market value, driven by nationwide AMI smart electricity meter rollout mandates targeting household coverage

- The three-phase smart meter industrial segment is growing at 9.1% CAGR as manufacturing and data-center operators seek granular demand-side visibility

• By Region

- Asia-Pacific leads with 38% share; China and India collectively account for more than 70% of regional volume

- Middle East & Africa registers the fastest regional CAGR of ~11.5%, driven by smart meter demand response integration programs in Saudi Arabia and the UAE

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up shipment data from 35+ countries with top-down revenue cross-checks against utility capital expenditure filings, manufacturer annual reports[8].