Smart Window Market Summary

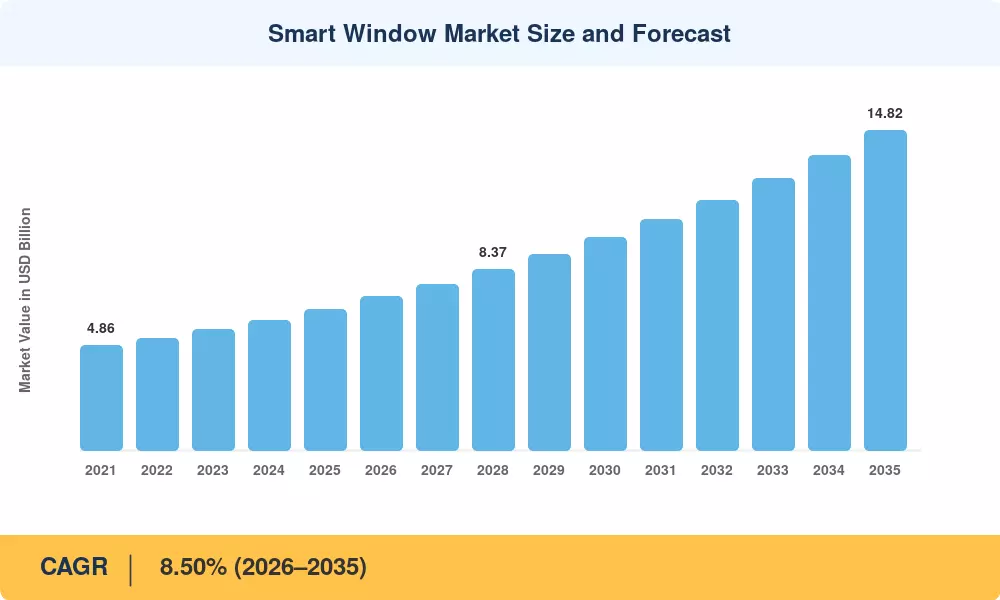

The Smart Window Market stood at USD 6.55 Billion in 2025, is projected to reach USD 7.11 Billion in 2026, and is forecast to grow to USD 14.82 Billion by 2035, expanding at a CAGR of 8.50% during 2026–2035. Two forces are pulling this growth forward simultaneously: mandatory building energy codes — California's Title 24 and the 2024 IECC edition chief among them — and corporate decarbonization pledges that treat automated fenestration as a non-negotiable line item in capital budgets [1]. The Smart Window Market is no longer a niche luxury play; it sits at the intersection of energy policy and occupant comfort, with procurement teams evaluating payback cycles rather than aesthetics alone.

Legacy manual blinds and static glazing are giving way to sensor-driven motorized shading and switchable glass that respond to daylight, occupancy, and grid signals in real time. The U.S. Department of Energy estimates that windows account for roughly 30% of building heating and cooling loads, and advanced fenestration can cut that figure by 20–35% [2]. Venture-backed glass specialists and established shade manufacturers alike are embedding edge computing into motor controllers, layering cybersecurity protections, and piloting ESCO financing to shorten payback periods for retrofit projects.

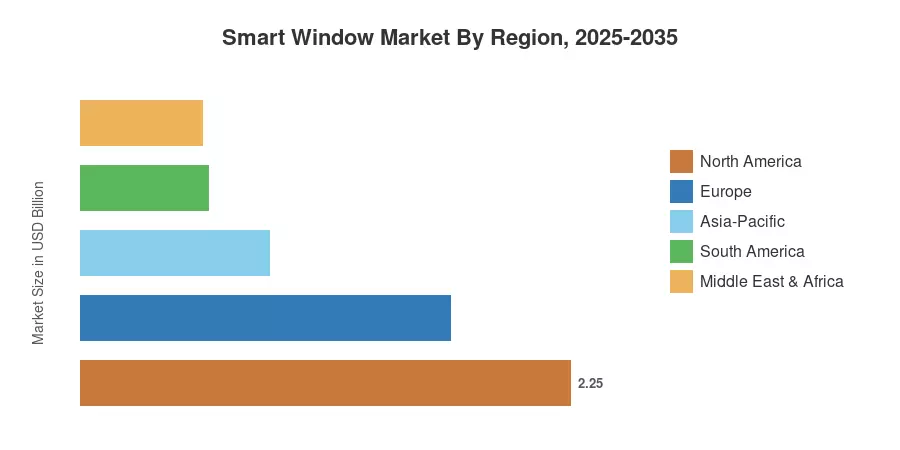

North America commands the largest revenue pool in the Smart Window Market, holding approximately 34.4% of global revenue in 2025, anchored by stringent energy codes and a deep commercial real-estate pipeline. Asia-Pacific is the fastest-growing region, advancing at a 13.25% CAGR through 2035 as urbanization and green-building certification programs accelerate adoption across China, India, and South Korea. Europe ranks second by market share at roughly 26%, driven by the EU Energy Performance of Buildings Directive and aggressive renovation-wave targets [3]. By the mid-2030s, smart fenestration will likely be standard specification in most Class A office construction globally.

Key Report Takeaways

• By Product Type

- Motorized Roller Shades captured approximately 36.5% of the Smart Window Market share in 2025, buoyed by competitive pricing and compatibility with existing window frames.

- Smart Glass Panels & Controllers are expanding at a 11.75% CAGR through 2035, driven by demand for tint-on-demand glazing in premium commercial envelopes.

• By Application

- Commercial deployments accounted for roughly 39.8% of the Smart Window Market share in 2025, led by Class A office and healthcare campus projects.

- Residential applications are registering the fastest growth at 12.65% CAGR, propelled by smart-home platform integration and Matter-enabled IoT ecosystems.

• By Region

- North America retained the dominant position in the Smart Window Market, contributing about 34.4% of 2025 global revenue.

- Asia-Pacific is on track to post a 13.25% CAGR from 2026 to 2035, with China and India leading capacity additions.

Smart Window Market Size and Forecast (2021–2035)

Market Research Future's sizing model blends bottom-up product shipment data, top-down macroeconomic indicators, and validated vendor disclosures across 35 countries. Historical figures (2021–2024) reflect actual trade flows, while the forecast period (2026–2035) applies regression-adjusted growth assumptions calibrated to energy code adoption curves and construction-start indices.