Solar Control Window Films Market Summary

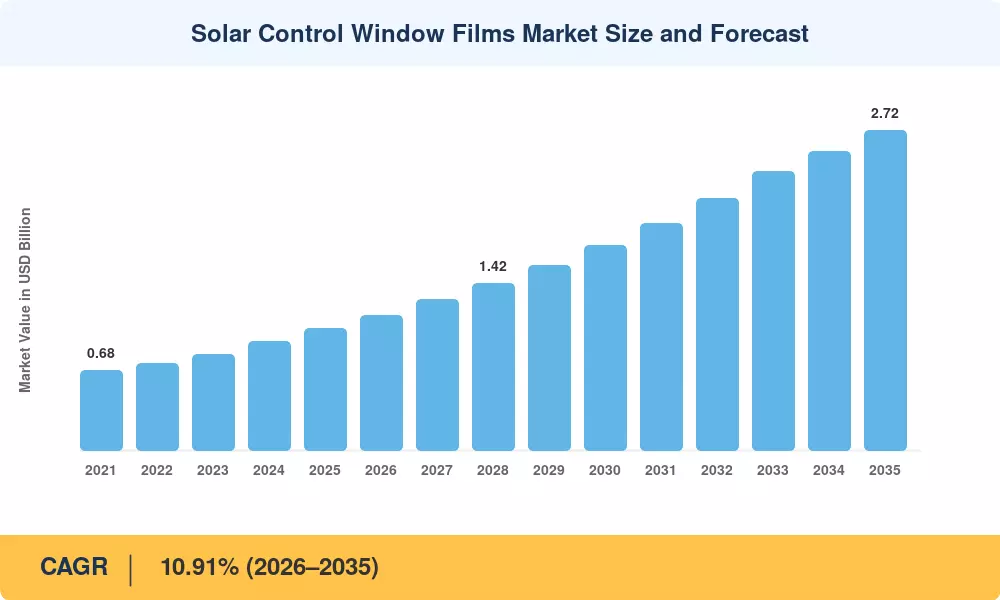

The Solar Control Window Films Market was valued at USD 1.04 billion in 2025 and is projected to reach USD 1.15 billion in 2026 before expanding to USD 2.72 billion by 2035, registering a CAGR of 10.91% during the forecast period (2026–2035). Accelerating decarbonization mandates across 130+ countries and rising commercial electricity tariffs — up 18% on average since 2021 — have turned heat control window film into a high-ROI retrofit investment with sub-three-year payback periods [2]. The convergence of green building codes and occupant comfort standards keeps this Solar Control Window Films Market on a resilient growth trajectory, even as petrochemical feedstock prices remain volatile.

A technological shift is reshaping the Solar Control Window Films Market from conventional dyed and metalized products toward advanced ceramic–metallic hybrid films and nano-ceramic coatings that reject over 95% of infrared radiation without darkening visible light transmission. The U.S. Department of Energy's Building Technologies Office allocated USD 280 million to envelope efficiency programs in FY 2024, explicitly naming UV protection films and solar protection films among eligible retrofit technologies [3]. Vacuum-coated reflective window films continue to dominate current specifications because they deliver neutral aesthetics alongside high infrared rejection, but next-generation ceramic formulations are rapidly closing the performance gap.

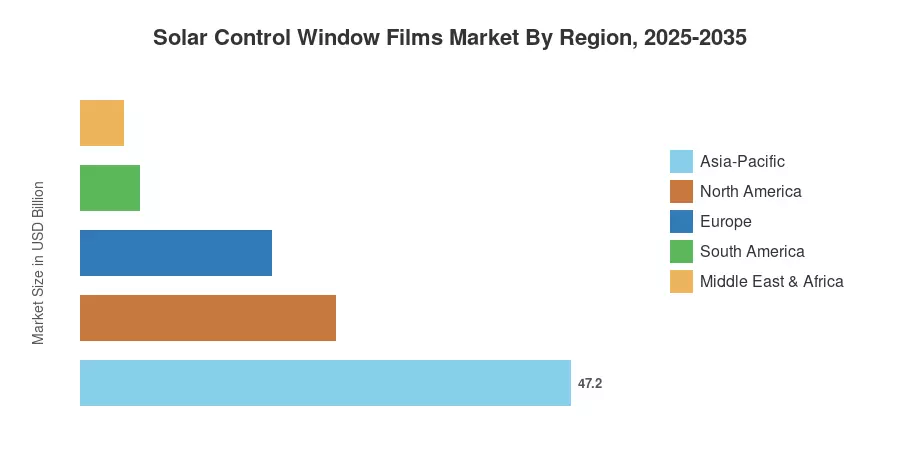

Asia-Pacific commands the largest share of the Solar Control Window Films Market at approximately 47.2% of 2025 revenue, driven by construction booms in China, India, and Southeast Asia. The region also posts the fastest CAGR of 11.28% through 2035. North America holds the second-largest position with roughly 24.6% share, buoyed by federal tax incentives under the Inflation Reduction Act that directly benefit energy-saving window film installations [4]. Europe rounds out the top three, where EU net-zero mandates and the revised Energy Performance of Buildings Directive are pulling architectural window films into mainstream specification.

Key Report Takeaways

• By Film Type

- Vacuum-coated reflective films captured 45.1% of the Solar Control Window Films Market share in 2025, reinforcing their role as the specification standard for commercial glazing

- Dyed films are expanding at a CAGR of 9.48% through 2035, gaining traction in cost-sensitive residential window tinting applications

• By Absorber Type

- Ceramic absorber technology led the Solar Control Window Films Market with 48.5% revenue share in 2025

- Metallic absorbers are posting the fastest growth at 11.12% CAGR, favored for their superior heat control window film performance in extreme climates

• By Installation Stage

- New-build projects accounted for USD 0.89 billion in 2025 revenue, reflecting the integration of sun control films into original glazing specifications

- Retrofit installations are growing at 11.45% CAGR as building owners upgrade aging facades with energy-saving window films

• By End-User Industry

- Construction held 57.3% of 2025 revenue, driven by green building certifications requiring solar protection films

- Automotive applications are forecast to expand at 11.74% CAGR through 2035

• By Region

- Asia-Pacific dominated with 47.2% of the Solar Control Window Films Market in 2025

- North America held 24.6% share, with the U.S. anchoring demand for commercial window films

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s proprietary estimation framework triangulates primary interviews with film manufacturers, construction procurement databases, distributor sell-through data, and macro indicators, including commercial construction starts and automotive production volumes. Historical figures (2021–2024) are validated against customs trade data and industry association shipment reports.