SMS Firewall Market Summary

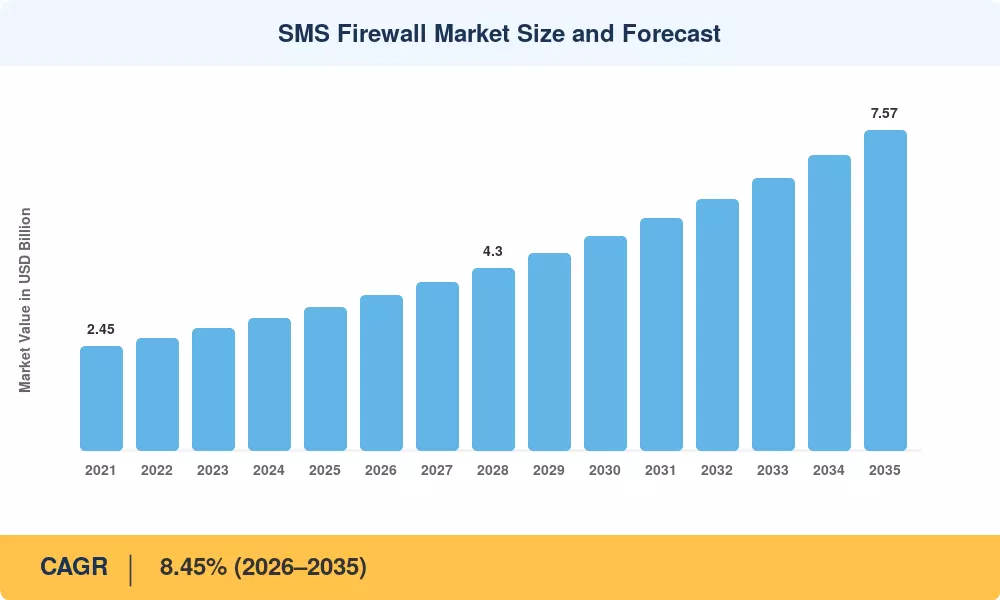

The SMS Firewall Market was valued at USD 3.38 billion in 2025 and is projected to reach USD 3.65 billion in 2026 before expanding to USD 7.57 billion by 2035, registering a CAGR of 8.45% during the 2026–2035 forecast period. Surging adoption of A2P messaging protection solutions by mobile operators — driven by TRAI's traceability mandates in India [2], the EU's revised Electronic Communications Code [3], and the FCC's renewed focus on robocall and spam mitigation in the United States [4] — is anchoring capital investment across the value chain. Operators lost an estimated USD 6.7 billion to SMS fraud globally in 2024, and that bleeding has forced accelerated procurement of next-generation filtering engines [5].

As operators switch from outdated SS7 SMS firewall architectures to signaling stacks based on Diameter and HTTP/2 that are compatible with 5G standalone cores, a technological revolution is changing the SMS firewall market [6]. Rule-based filtering appliances are being replaced by cloud-native, AI-driven analytics tools, which provide real-time SMS spam filtering at throughputs higher than 50,000 messages per second. The demand for interoperable mobile network messaging security gateways was sparked by the participation of 78 operator groups in GSMA's 2024 SMS SenderID Protection Registry [7].

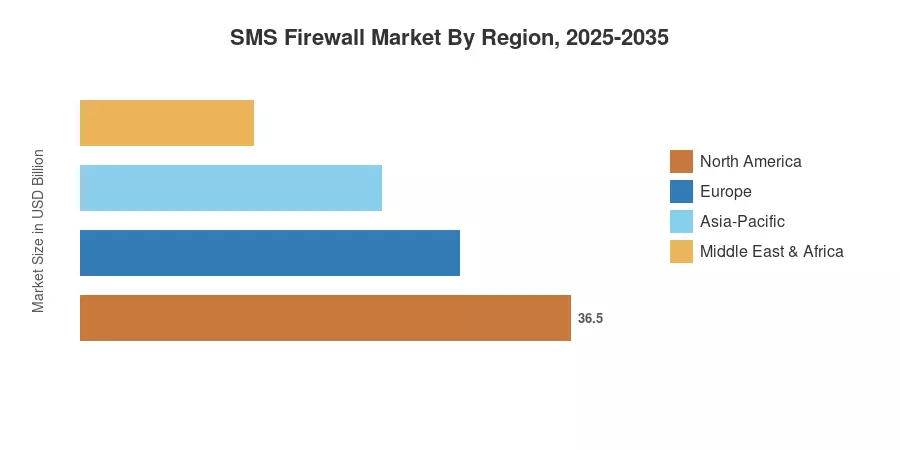

Due to strict TCPA compliance and corporate spending on roaming SMS security, North America accounts for over 40% of global income. With a 13.0% CAGR, Asia-Pacific is the fastest-growing market due to South Korea's and Japan's quick rollouts of 5G and India's DLT-based sender verification ecosystem. Thanks to GDPR-driven data sovereignty regulations that necessitate on-shore SMS filtering, Europe has the second-largest market at roughly 26%. Through 2035, the SMS firewall market is expected to grow by double digits in emerging markets.

Key Report Takeaways

• By SMS Type

- A2P traffic dominated the SMS Firewall Market with approximately 69.0% share in 2025, reflecting the critical need for A2P messaging protection across banking, healthcare, and government verticals.

- P2P enterprise messaging is forecast to expand at a 10.5% CAGR through 2035 as operators deploy behavioral analytics to differentiate legitimate peer traffic from grey-route abuse.

• By Deployment

- On-premise deployments held 56.4% of the SMS Firewall Market revenue in 2025; cloud deployments are projected to register a 13.6% CAGR as tier-2 and tier-3 operators adopt subscription-based mobile network messaging security tools.

• By Service Type

- Professional services captured 59.5% revenue share in 2025, while managed services will accelerate at 11.7% CAGR as operators outsource real-time SMS spam filtering operations.

• By End-User Industry & Network Generation

- BFSI accounted for 35.2% of revenue, spending heavily on SS7 SMS firewall upgrades to secure OTP and transaction-alert channels.

• By Network Generation

- 5G network segments will accelerate at a 13.3% CAGR through 2035 as standalone deployments demand protocol-aware roaming SMS security layers.

• By Regional

- North America led with 40.0% revenue share in the SMS Firewall Market in 2025.

- Asia-Pacific is predicted to register a 13.0% CAGR, driven by regulatory mandates and rising A2P messaging protection needs.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s market sizing integrates bottom-up operator CAPEX surveys, vendor revenue disclosures, and top-down TAM modeling calibrated against GSMA Intelligence subscriber data and ITU traffic statistics. Historical figures (2021–2024) are validated; 2025 is the base year; 2026–2035 values apply the calibrated CAGR of 8.45%.