Sodium-Ion Battery Market Summary

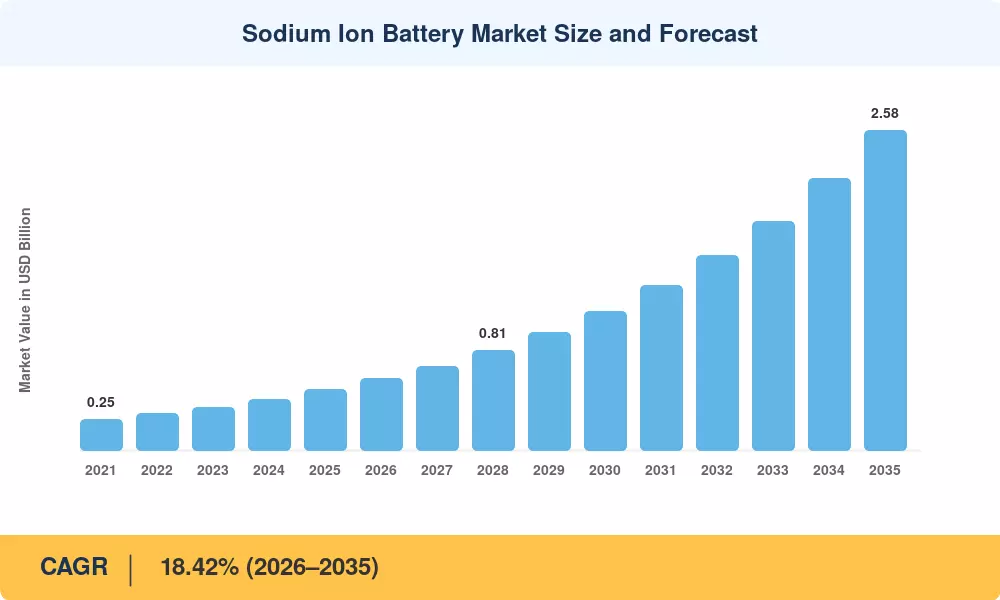

The Sodium Ion Battery Market reached an estimated USD 0.49 billion in 2025 and is projected to grow from USD 0.58 billion in 2026 to USD 2.58 billion by 2035, registering a CAGR of 18.42% during the forecast period (2026–2035). This expansion is anchored in persistent lithium carbonate price volatility — which saw spot prices swing by over 70% between 2022 and 2024 — and accelerating grid-scale storage tenders across China and Europe that specifically favor sodium-ion cell chemistries for their cost advantage over incumbent lithium iron phosphate packs [2][3].

A generational shift is underway in electrochemical storage. Utilities and fleet operators that historically relied on lithium-ion systems are now piloting Na-ion battery hard carbon anode configurations capable of delivering comparable cycle life at 25–30% lower cell-level cost. China's CATL sodium-ion battery commercial rollout in late 2023 validated gigawatt-hour-scale manufacturing, while the European Battery Alliance earmarked EUR 3.2 billion through 2030 for next-generation cell research, including sodium chemistries [4][5]. These investments are compressing the typical 8–10 year commercialization timeline for new battery technologies to roughly five years.

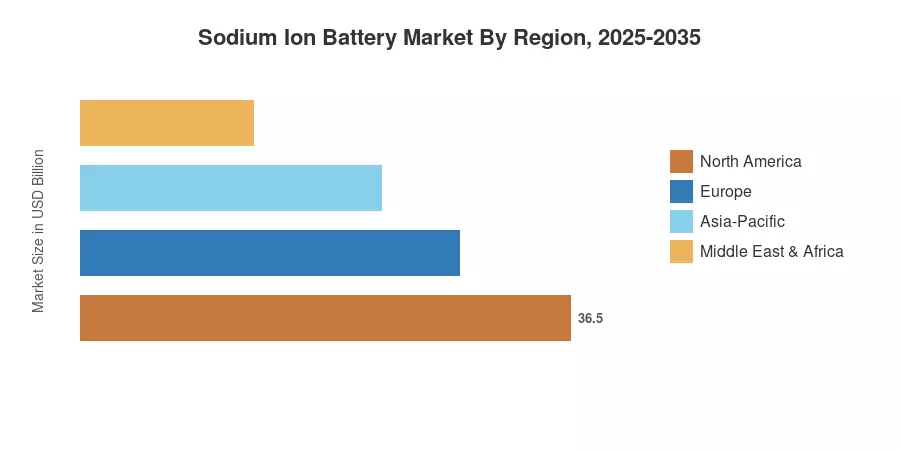

Asia-Pacific dominates the Sodium Ion Battery Market with approximately 49.2% revenue share in 2025, driven by China's policy-backed grid tenders and domestic cathode supply chains. Europe is the second-largest region, holding around 24.8% share on the strength of its battery passport mandate and sustainability regulations. Asia-Pacific simultaneously ranks as the fastest-growing region at a projected CAGR of 21.3% through 2035, as Indian and Southeast Asian manufacturers begin commissioning dedicated sodium-ion production lines

Key Report Takeaways

• By Form Factor

- Cylindrical cells accounted for roughly 52.4% of the Sodium Ion Battery Market in 2025, reflecting mature manufacturing tooling adapted from lithium-ion lines

- Pouch format cells are advancing at a 24.1% CAGR through 2035, propelled by lightweight packaging requirements for two-wheelers and urban delivery vehicles

• By Application

- Stationary energy storage commanded approximately 76.9% of the Sodium Ion Battery Market share in 2025, underpinned by four-hour discharge grid contracts in China and Europe

- Transportation applications are forecast to post a 21.6% CAGR through 2035 as automakers integrate sodium packs into low-range city cars

• By End-User Industry

- Utilities held the largest end-user share in the Sodium Ion Battery Market at around 59.6% in 2025

- Automotive demand is expected to expand at a 25.4% CAGR through 2035, the fastest among all end-user segments

• By Region

- Asia-Pacific led with 49.2% of global revenue in 2025 and is projected to grow at a 21.3% CAGR to 2035

- Europe captured the second-largest share, fueled by the EU Battery Regulation and carbon border adjustments

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up production capacity data from over 45 cell manufacturers, cross-referenced with downstream procurement contracts, regulatory filings, and trade databases. Historical figures (2021–2024) are based on audited shipment volumes; the 2025 base year blends preliminary shipment data with capacity utilization estimates; forecast years (2026–2035) apply a calibrated CAGR with adjustments for anticipated capacity ramp-ups, policy shifts, and raw-material price trajectories[6].