Soil Conditioners Market Summary

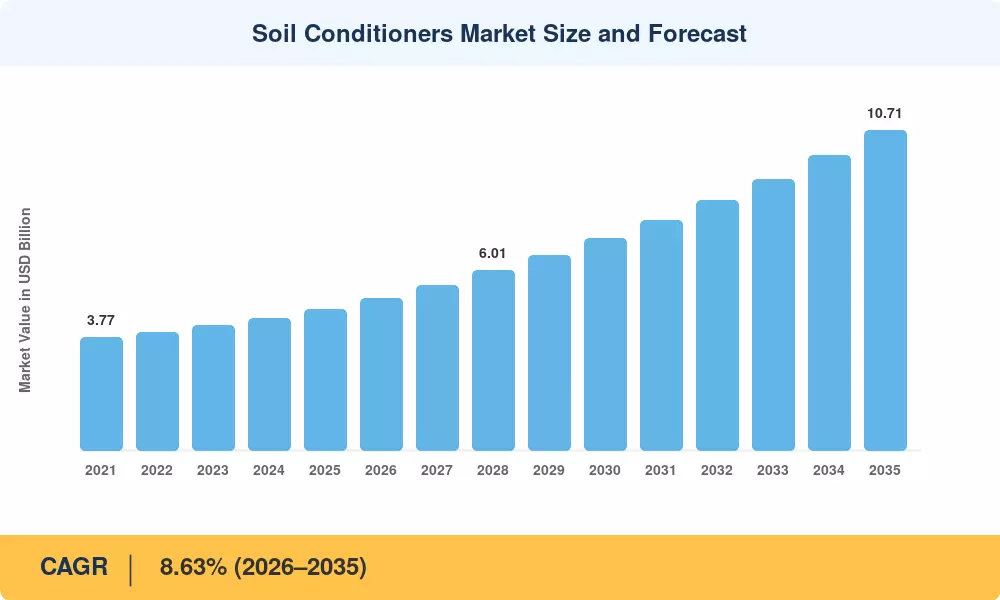

The Soil Conditioners Market was valued at USD 4.72 billion in 2025 and is projected to reach USD 5.09 billion in 2026 before climbing to USD 10.71 billion by 2035, registering a CAGR of 8.63% over the forecast period (2026–2035). This expansion is anchored to accelerating government soil-health mandates — the EU's Soil Monitoring Law adopted in 2024, India's Soil Health Card scheme covering over 230 million holdings, and the U.S. Department of Agriculture's USD 3.1 billion investment in conservation programs under the Inflation Reduction Act [1][2]. Degrading arable land quality across intensively farmed regions continues to push growers, municipalities, and industrial landscapers toward conditioning inputs that rebuild tilth and nutrient-cycling capacity.

A decisive technology shift is reshaping the Soil Conditioners Market. Conventional lime-and-gypsum treatments, which dominated for decades, are steadily giving ground to bio-enhanced and enzyme-catalyzed formulations that accelerate microbial colonization and carbon sequestration. Digital soil-mapping platforms — integrating satellite multispectral imagery with IoT-enabled soil probes — are refining application rates, cutting input waste by an estimated 18–22% on precision-managed farms [3]. Leading suppliers now bundle biological conditioners with data-driven advisory subscriptions, creating recurring revenue streams that traditional commodity sellers cannot easily replicate.

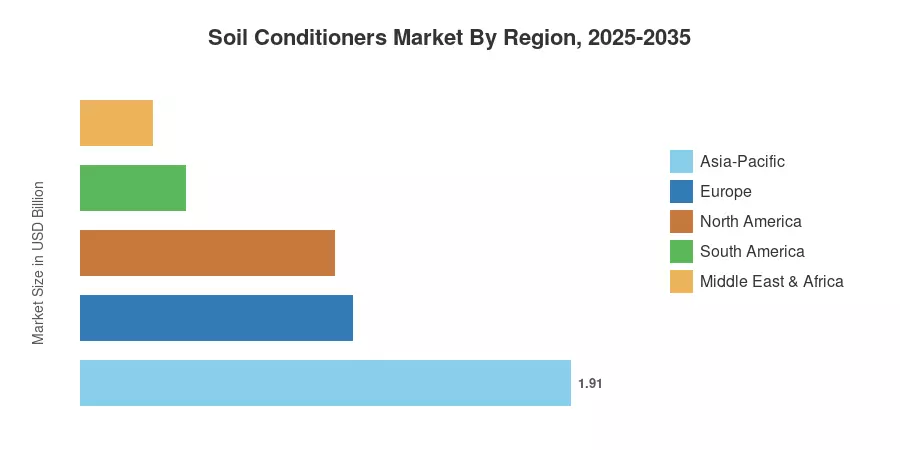

Asia-Pacific commands the largest share of the Soil Conditioners Market at roughly 40.50% of global revenue in 2025, driven by intensive rice and wheat cultivation systems across China, India, and Southeast Asia. South America is the fastest-growing region, posting an anticipated CAGR of 8.75% through 2035 as Brazilian soybean and sugarcane producers scale regenerative soil practices. Europe holds the second-largest regional position, underpinned by the EU Common Agricultural Policy's eco-scheme conditionalities that incentivize organic amendments. The decade ahead will be defined by regulatory tightening, biological product innovation, and the digitalization of soil management at scale.

Key Report Takeaways

• By Product Type

- Organic inputs held a 59.50% share of the Soil Conditioners Market in 2025, reflecting farmer preference for carbon-rich amendments that improve water-holding capacity and microbial diversity.

- Enzyme-enhanced variants are forecast to grow at a 9.10% CAGR through 2035, supported by R&D breakthroughs in catalytic bio-stimulants.

• By Crop Type

- Cereals and grains captured 36.00% of the Soil Conditioners Market in 2025, as wheat and rice systems across monsoon Asia drive bulk-volume demand.

- Fruits and vegetables are projected to expand at a 9.90% CAGR from 2026 to 2035, led by high-value horticulture in protected environments.

• By Formulation

- Dry products led with a 46.10% revenue share in 2025, preferred for broadacre field application due to lower transport costs and longer shelf stability.

- Liquid solutions are advancing at a 10.30% CAGR from 2026 to 2035, propelled by fertigation compatibility and vertical farming adoption.

• By Region

- Asia-Pacific accounted for 40.50% of the Soil Conditioners Market in 2025.

- South America is the fastest-growing region with an 8.75% CAGR through 2035.

Soil Conditioners Market Size and Forecast (2021–2035)

Market Research Future's sizing model triangulates bottom-up revenue estimates from manufacturer shipments, distributor sell-through records, and government agricultural census data against top-down demand proxies, including cultivated area expansion, soil degradation indices, and regulatory compliance timelines. Historical figures (2021–2024) are validated against trade association publications and customs databases; forecast projections apply segment-weighted CAGRs adjusted for policy catalysts and technology adoption curves[5].