Solid Materials Handling Equipment Market Summary

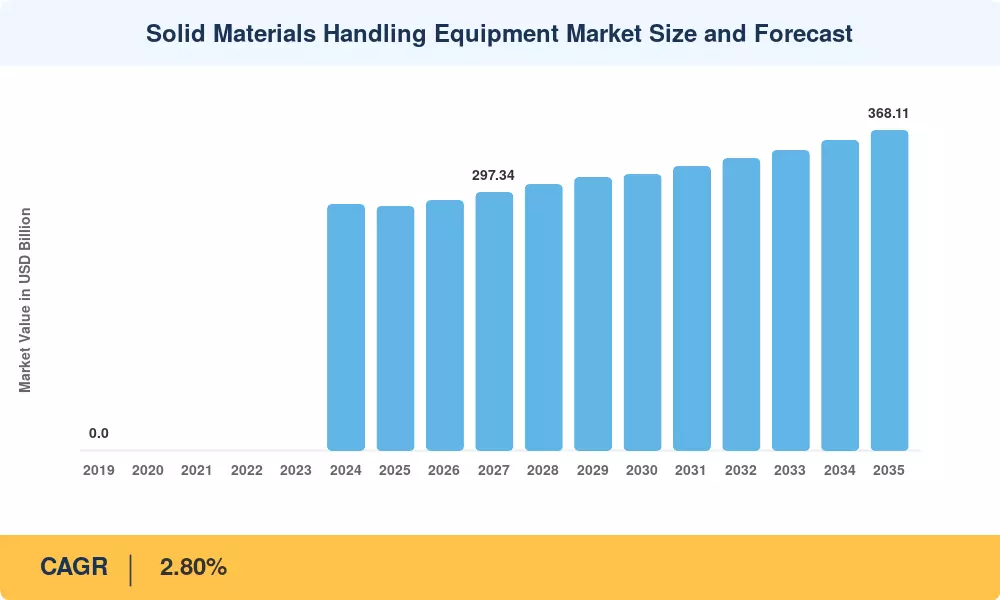

The global solid materials handling equipment market was valued at USD 280.35 billion in 2025 and is projected to reach USD 368.11 billion by 2035, registering a CAGR of 2.80% during the forecast period (2026–2035). The market's steady expansion is underpinned by increasing demand for automation in manufacturing and logistics processes, rising investments in infrastructure development and construction activities, and a growing emphasis on improving supply chain efficiency and productivity. Capital expenditure in logistics automation across major industrial economies continues to accelerate, with governments and private enterprises committing multibillion-dollar investments to modernize material flow systems in warehousing, mining, cement, and food-processing sectors [1][2].

Component-specific handling solutions, which sold for USD 476.40 million in 2025, dominate the product market, demonstrating the vital role that customized machinery plays in high-throughput industrial settings. Driven by the need to reduce operational downtime, on-wing service configurations—valued at USD 796.91 million in 2025—represent the largest service-mode segment. With a predicted 6.47% CAGR, the fastest-growing product category is on-wing engine cleaners, indicating a shift in the industry toward in-situ maintenance solutions. The industry's dedication to precision engineering and regional capacity expansion is demonstrated by significant innovations like Coperion's inventive discharge gate valve (2024) and Qlar Group's new pneumatic conveying test center in Bangalore (2026) [3][4].

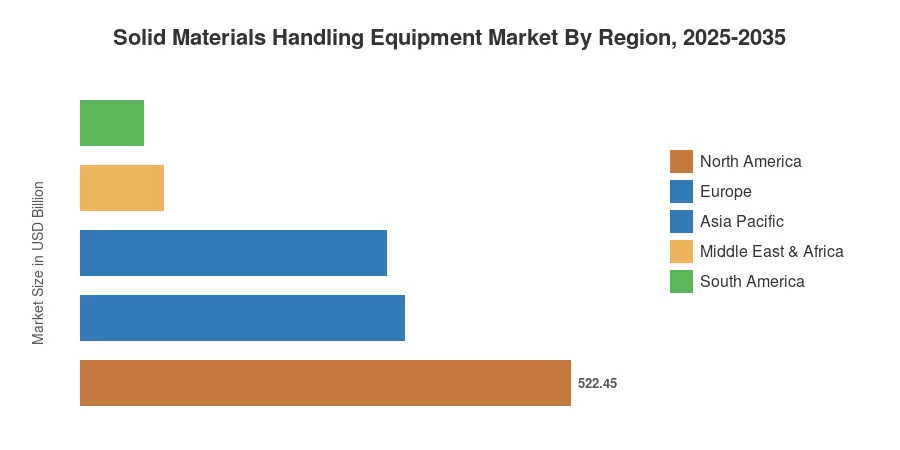

With a 2025 market value of USD 522.45 million and a compound annual growth rate (CAGR) of 6.17%, North America continues to be the leading region because to its sophisticated manufacturing infrastructure and early adoption of automation technology. With businesses like Qlar Group investing in specialized testing facilities to assist regional clients, the Asia Pacific is the fastest-growing market due to the rapid industrialization of China, India, and Southeast Asia. At USD 345.84 million in 2025, Europe has the second-largest share, while South America and the Middle East & Africa provide new growth opportunities fueled by rising mining and building activities. It is anticipated that the convergence of IoT integration, smart technologies, and sustainability requirements would change competitive dynamics in every region over the course of the next ten years [5][6].

Key Report Takeaways

| Segment Dimension | Key Metric | Notes |

| By Product Type — Dominant Segment | Component-Specific Cleaning Chemicals: USD 476.40 Mn (2025) | Largest product category driven by specialized industrial demand |

| By Product Type — Fastest Growing | On-Wing Engine Cleaners: 6.47% CAGR | Rapid adoption of in-situ maintenance solutions |

| By Nature — Dominant Segment | Organic Chemicals: USD 745.88 Mn (2025) | Preferred for performance and regulatory compliance |

| By Nature — Fastest Growing | Organic Chemicals: 5.83% CAGR | Sustained demand across industrial applications |

| By Formulation Base — Dominant Segment | Water-Based: USD 639.77 Mn (2025) | Environmental and safety regulations favor water-based solutions |

| By Formulation Base — Fastest Growing | Water-Based: 5.70% CAGR | Eco-friendly shift accelerating adoption |

| By Aircraft Type — Dominant Segment | Commercial Aircraft: USD 796.91 Mn (2025) | Largest end-use category by fleet volume |

| By Aircraft Type — Fastest Growing | Commercial Aircraft: 5.70% CAGR | Rising global air traffic and fleet expansion |

| By Service Mode — Dominant Segment | On-Wing: USD 796.91 Mn (2025) | Minimizes downtime and operational disruption |

| By End Use — Dominant Segment | Third-Party Maintenance Service Providers: USD 679.60 Mn (2025) | Outsourcing trend in maintenance operations |

| By End Use — Fastest Growing | Airlines & Fleet Operators: 5.90% CAGR | In-house capability development is accelerating |

| By Region — Dominant | North America: USD 522.45 Mn (2025) | Mature infrastructure and high automation adoption |

| By Region — Fastest Growing | North America: 6.17% CAGR | Continued reinvestment in industrial modernization |

Market Size and Forecast (2019–2035)

MRFR's market sizing methodology integrates bottom-up revenue estimation from primary interviews with equipment manufacturers, distributors, and end-users, supplemented by top-down validation using macroeconomic indicators, trade data, and secondary industry publications. Historical data (2019–2024) is benchmarked against company filings and industry association statistics, while forecast projections (2026–2035) apply segment-level CAGR models calibrated to regional demand drivers and policy scenarios.