Solid Oxide Fuel Cell Market Summary

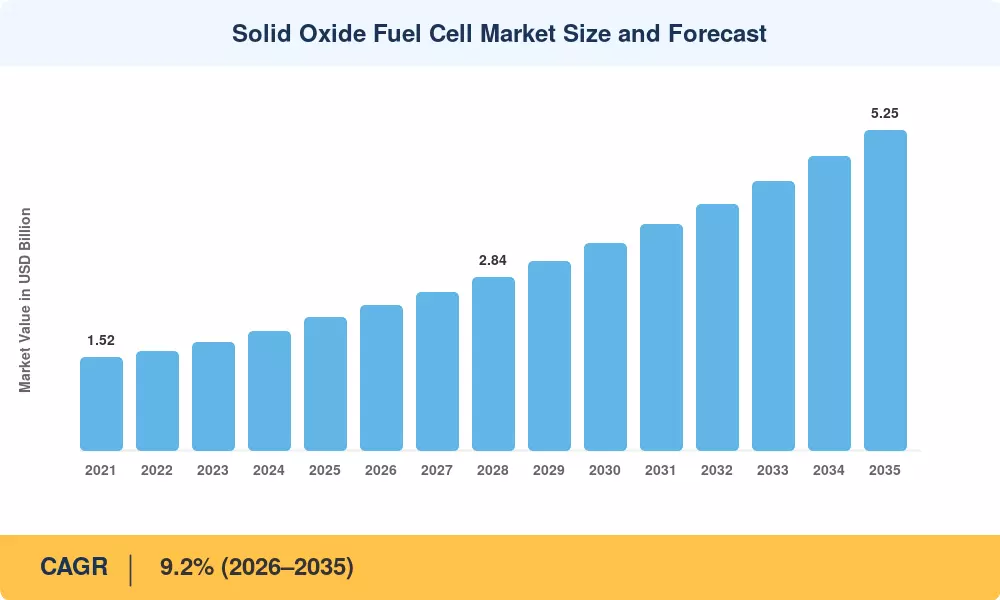

The Solid Oxide Fuel Cell Market stood at an estimated USD 2.18 billion in 2025 and is projected to reach USD 2.38 billion in 2026, growing at a compound annual growth rate of 9.2% through 2035 to hit USD 5.25 billion. That trajectory owes much to aggressive national hydrogen strategies — the U.S. Department of Energy's Hydrogen Shot initiative targeting USD 1/kg clean hydrogen by 2031, and the European Union's REPowerEU plan channeling EUR 5.2 billion into electrolyzer and fuel cell infrastructure [1][2]. These policy anchors are converting pilot-stage interest into bankable project pipelines across distributed power generation, industrial cogeneration, and maritime auxiliary power.

A fundamental technology shift is unfolding within the Solid Oxide Fuel Cell Market. Legacy diesel generators and centralized gas turbines that have long served backup and baseload power roles are being challenged by high-efficiency SOFC systems capable of 60%+ electrical efficiency — and above 85% when configured for combined heat and power. Capital costs for planar stack modules have dropped roughly 38% since 2019 according to DOE manufacturing analyses, and that cost curve is steepening as ceramic processing techniques mature [3]. Corporate procurement is accelerating: Bloom Energy alone shipped over 1.2 GW of cumulative capacity through 2024, with data center operators representing a fast-expanding customer cohort [4].

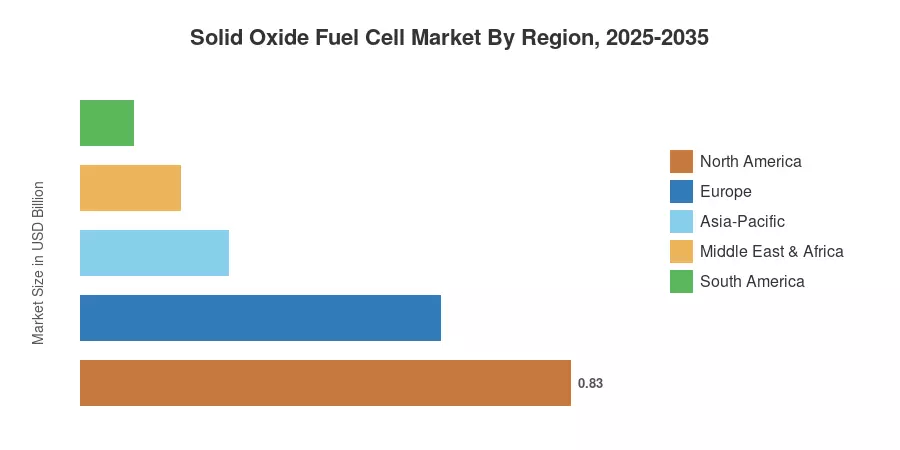

North America commands the largest share of the Solid Oxide Fuel Cell Market at approximately 38% of 2025 revenue, driven by federal investment tax credits under the Inflation Reduction Act and California's Self-Generation Incentive Program. Asia-Pacific is the fastest-growing region with a projected CAGR of 11.4%, led by South Korea's national fuel cell roadmap and Japan's ENE-FARM residential deployment program. Europe holds the second-largest share at roughly 28%, anchored by Germany's National Hydrogen Strategy and the EU's Clean Hydrogen Partnership funding [5][6]. As grid decarbonization targets tighten globally, the Solid Oxide Fuel Cell Market stands to absorb a rising share of stationary distributed energy investment through 2035.

Key Report Takeaways

• By Type

- Planar SOFC configurations dominate with approximately 68% of 2025 market revenue, benefiting from superior power density and manufacturing scalability

- Tubular designs are expanding at a CAGR of 10.8% through 2035, favored in harsh-environment and long-cycle industrial applications

• By Application

- Stationary power generation accounts for roughly USD 1.57 billion in 2025, representing the core revenue pillar of the Solid Oxide Fuel Cell Market

- Portable SOFC units are growing at 12.1% CAGR, propelled by military field power and remote telecom base station demand

- Transportation applications hold an estimated 8% market share, with marine auxiliary power emerging as the lead use case

• By Region

- North America leads the Solid Oxide Fuel Cell Market with 38% share, anchored by U.S. federal incentives and commercial data center procurement

- Asia-Pacific registers the fastest CAGR of 11.4%, reflecting national hydrogen economy buildouts in South Korea, Japan, and China

- Europe holds approximately 28% of global revenue, driven by EU Green Deal mandates and German industrial cogeneration projects

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology combines bottom-up shipment tracking from over 45 SOFC manufacturers and system integrators with top-down cross-validation against national energy deployment databases, DOE program disclosures, and IEA fuel cell installation registries. Historical figures reflect actual installations and recognized revenue; forecast values apply segment-level growth models calibrated to policy incentive schedules, manufacturing cost-learning curves, and hydrogen infrastructure buildout timelines.