South Africa ICT Market Summary

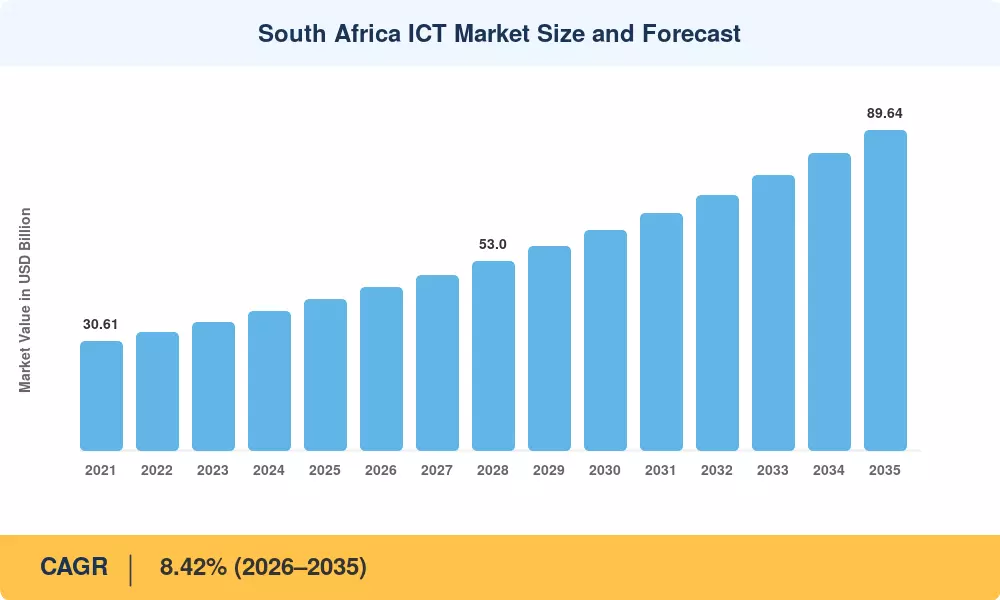

The South Africa ICT Market reached a valuation of USD 42.31 billion in 2025 and is projected to climb from USD 45.69 billion in 2026 to USD 89.64 billion by 2035, registering a CAGR of 8.42% across the forecast window. This acceleration is anchored in South Africa's National Digital and Future Skills Strategy, which earmarked ZAR 1.2 billion for digital literacy and broadband expansion between 2024 and 2027, alongside a private-sector commitment of over USD 1.5 billion in hyperscale data-center capacity across Johannesburg and Cape Town. ICT regulation and policy in South Africa continues to shape procurement cycles, particularly as the Electronic Communications Amendment Act tightens spectrum-allocation timelines and mandates open-access fiber corridors.

Legacy on-premise systems that once dominated enterprise IT budgets are rapidly giving way to cloud-native architectures and hybrid deployments. Cloud adoption by South African enterprises accelerated after major load-shedding episodes forced business-continuity redesigns, and the country's three largest banks collectively invested over USD 800 million in digital infrastructure investment in South Africa during 2023–2024 alone [2]. Fintech and e-commerce growth in South Africa further compounds demand, with real-time payment mandates under the South African Reserve Bank driving API-first platform builds across the BFSI vertical.

Gauteng province commands roughly 44% of the South Africa ICT Market, supported by Johannesburg's status as the continent's financial hub. The Western Cape trails at approximately 22% share, fueled by Cape Town's emerging tech-startup corridor. Broadband and fiber rollout in Sub-Saharan Africa positions the wider region for the fastest growth trajectory globally, with neighboring economies leveraging South African cloud infrastructure as a regional gateway. The decade ahead will see digital infrastructure investment in South Africa reshape not just domestic competitiveness but continental connectivity patterns

Key Report Takeaways

• By Product Type

- IT services held a 34.8% share of the South Africa ICT Market in 2025, driven by managed-services contracts tied to cloud migration programs

- IT security and cybersecurity is advancing at a 9.1% CAGR through 2035 as cyber-insurance underwriters in the South Africa ICT Market tighten compliance requirements

- IT software revenues are projected to reach USD 18.7 billion by 2035, underpinned by ERP and CRM modernization cycles

• By Enterprise Size

- Large enterprises captured 66.4% of spending in the South Africa ICT Market during 2025

- Small and medium enterprises are on track for a 9.5% CAGR to 2035, supported by government voucher schemes and fintech and e-commerce growth in South Africa

• By End-User Vertical

- BFSI commanded USD 10.2 billion of the South Africa ICT Market in 2025

- Healthcare is forecast to expand at a 9.2% CAGR through 2035, driven by telemedicine mandates and electronic health-record adoption

• By Deployment Model

- Cloud accounted for 50.1% of revenue in the South Africa ICT Market in 2025

- Hybrid architecture is projected to post an estimated USD 22.4 billion by 2035 as data-residency requirements force balanced deployments

Market Research Future (MRFR)'s estimates integrate bottom-up enterprise-spending surveys, vendor revenue disclosures, and macroeconomic multipliers calibrated against South Africa's GDP growth outlook. Historical figures (2021–2024) reflect audited vendor filings; forecast projections (2026–2035) apply a compounding growth model validated through cross-referencing with national statistics from Stats SA and the Department of Communications and Digital Technologies [3].

.webp?v=1782888033)