Space Electronics Market Summary

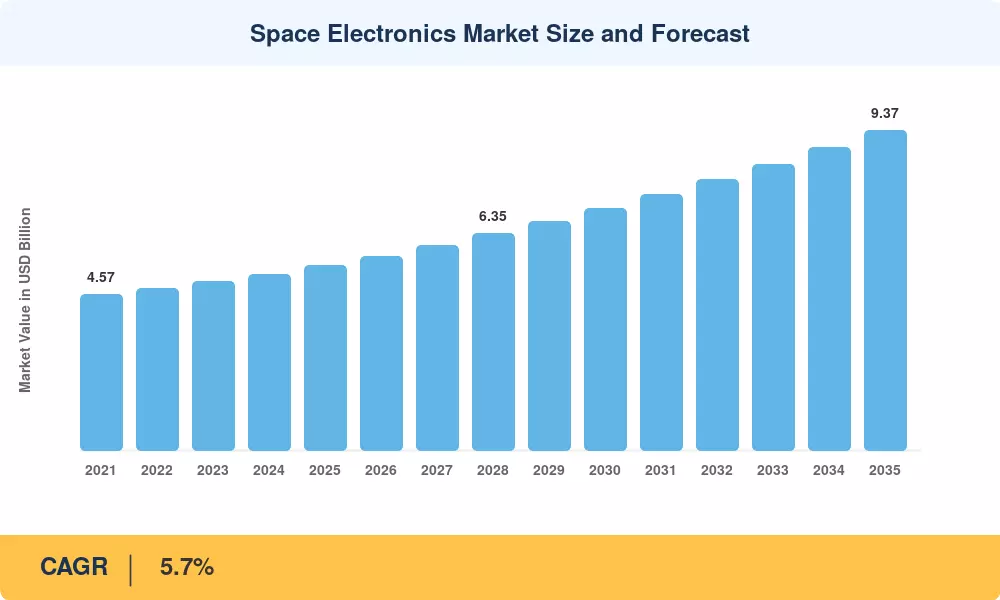

The Space Electronics Market stood at USD 5.41 billion in 2025 and is projected to reach USD 5.69 billion in 2026 before climbing to USD 9.37 billion by 2035, expanding at a 5.7% CAGR across the 2026–2035 forecast window. This growth trajectory reflects a decisive shift from bespoke, low-volume flight hardware toward scalable production architectures driven by mega-constellation deployments and renewed government exploration budgets. NASA's Artemis program alone has committed over USD 93 billion through the early 2030s, while the European Space Agency's 2025 ministerial conference secured EUR 16.9 billion for its next planning cycle — both programs funneling capital directly into qualified electronic subsystems [1][2].

A generational technology transition underpins this expansion. Legacy single-board computers and analog telemetry chains are giving way to system-on-chip architectures that merge processing, power management, and radiation mitigation onto monolithic dies. Wide-bandgap semiconductors — gallium nitride and silicon carbide devices — are displacing traditional silicon in power conversion stages, delivering 30–40% mass savings on solar-array regulators and electric-propulsion drivers [3]. Commercial semiconductor foundries are increasingly offering radiation-tolerant process nodes, compressing qualification timelines from years to months.

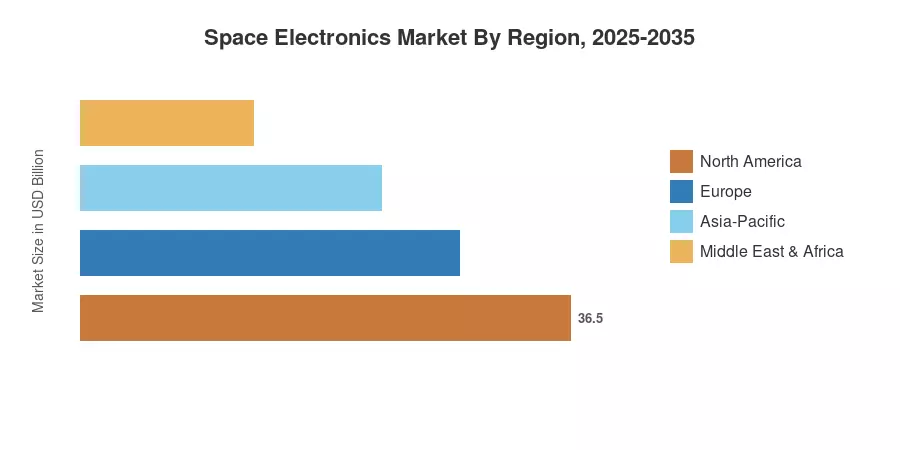

North America commands roughly 39.0% of the Space Electronics Market, anchored by vertically integrated defense primes and a dense network of fabless design houses. Asia-Pacific is the fastest-growing region at a 9.7% CAGR, propelled by India's expanding ISRO launch cadence and China's aggressive LEO constellation filings. Europe holds the second-largest share at approximately 26%, with institutional demand flowing through ESA and bilateral cooperation frameworks. As sovereign launch capabilities multiply across continents, the addressable hardware base for qualified electronics will widen through 2035 and beyond.

Key Report Takeaways

• By Platform

- Satellites captured roughly 61.5% of the Space Electronics Market in 2025, driven by broadband-constellation build-outs that require thousands of identical bus units.

- Deep-space probes are forecast to grow at a 9.4% CAGR as missions to the Moon, Mars, and the asteroid belt demand autonomous onboard computing.

• By Component

- Integrated circuits anchor the component landscape, with FPGAs and rad-hard microprocessors accounting for the highest per-unit value.

- Power devices represent the fastest-growing component category at an 8.3% CAGR through 2035, fueled by the shift to electric propulsion and high-voltage solar arrays.

• By Application

- Communication systems led application-level revenue in 2025 with a 47.7% share of the Space Electronics Market, reflecting the dominance of data-relay and broadband payloads.

• By Type

- Radiation-tolerant parts exhibit the highest type-level CAGR at 9.6%, as constellation operators favor cost-optimized designs that accept limited single-event upsets.

• By End-User

- Commercial operators accounted for 58.5% of 2025 revenue, a share that continues to expand as private launch costs decline.

- Military and defense demand, however, is the fastest-growing end-user category in the Space Electronics Market

• By Region

- The Asia-Pacific Space Electronics Market is poised to grow at a 9.7% CAGR, led by India, China, and South Korea.

- North America is the dominating region with 39.0% share.

Market Size and Forecast (2021–2035)

The table below integrates historical actuals (2021–2024) derived from government procurement databases, public company filings, and industry association data, with a forward-looking forecast (2026–2035) calibrated against launch-manifest projections and announced constellation orders.