Specialty Fertilizers Market Summary

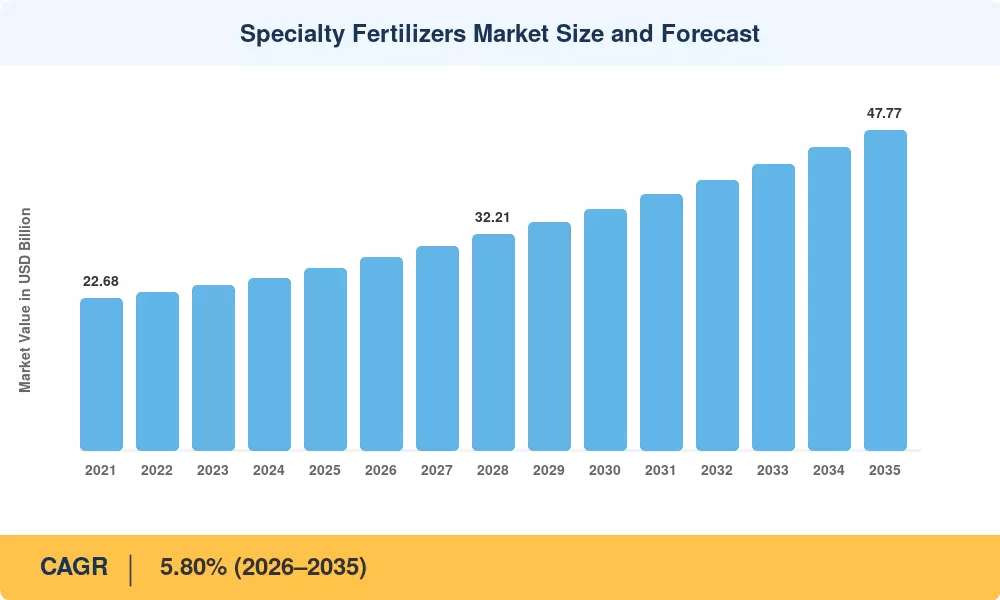

The Specialty Fertilizers Market was valued at USD 27.12 Billion in 2025, with the forecast period opening at USD 28.75 Billion in 2026 and projected to reach USD 47.77 Billion by 2035 at a CAGR of 5.80% during 2026–2035. Two catalysts anchor this trajectory: national nutrient-use-efficiency mandates — such as China's Zero-Growth Fertilizer Action Plan and India's revamped Nutrient-Based Subsidy regime — and rising private-sector investment in precision fertigation infrastructure, which exceeded USD 2.1 billion globally in 2024 [#9, #10]. Growers are no longer treating specialty grades as premium luxuries; they are treating them as operational necessities in water-scarce and carbon-conscious production systems.

A technical change is changing the way that nutrients go to the plant. Commodity granules are being displaced by sensor-guided, variable-rate fertigation systems that broadcast liquid and controlled-release nourishment zone-by-zone. BloombergNEF projects that green-ammonia capacity under construction will exceed 6 million metric tons by 2028, making low-carbon nitrogen a compliance-ready feedstock for the Specialty Fertilizers Market [12]. In lawn management, greenhouse production and high-value horticulture, polymer-coated granules are replacing split-application urea regimens.

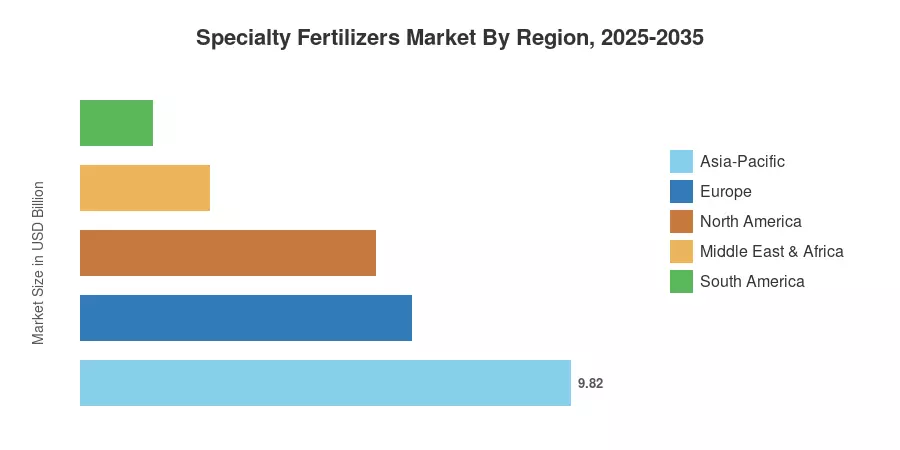

Asia-Pacific holds 36.2% of the worldwide revenue with intensive rice-vegetable rotations and increasing usage of fertigation in India and Southeast Asia. The Middle East & Africa geography is the fastest expanding, growing at a CAGR of 9.5% through 2035 as Gulf-state agri-tech projects channel investments into arid greenhouse complexes. Europe has the second-largest proportion of 24.5%, supported by the EU Fertilising Products Regulation, which reduces the cadmium limits and promotes specialist alternatives. The Specialty Fertilizers Market is at a structural inflection point, when regulatory pressure and digital agronomy are merging to expedite the mainstream adoption.

Key Report Takeaways

• By Specialty Type

- Liquid fertilizers captured 35.8% of the Specialty Fertilizers Market in 2025, reflecting fertigation compatibility and lower labor requirements.

- Controlled-release fertilizers are forecast as the fastest-growing specialty type, registering a CAGR of 9.5% during 2026–2035.

• By Application Mode

- Fertigation accounted for 44.5% of global application demand in 2025, led by drip-irrigation expansions across arid and semi-arid regions.

- Foliar application is projected to grow at a CAGR of 6.4% through 2035, driven by micronutrient-correction programs.

• By Crop Type

- Horticultural crops represented 39.8% of the Specialty Fertilizers Market in 2025 as the largest crop segment.

- Turf and ornamental crops are the fastest-growing crop segment, expanding at a CAGR of 8.5% during 2026–2035.

• By Geography

- Asia-Pacific held 36.2% of global revenue in 2025, led by China, India, and ASEAN economies.

- The Middle East & Africa are anticipated to record the fastest regional growth at a CAGR of 9.5% through 2035.

Specialty Fertilizers Market Size and Forecast (2021–2035)

Market Research Future’s (MRFR) estimations are based on primary interviews with agrochemical manufacturers, distributor channel surveys, customs trade data, and cross-validation against FAO and IFA fertilizer-use databases. Historical statistics (2021-2024) are actual trade volumes; 2025 is the base-year estimate, and 2026-2035 figures are anticipated projections with a blended CAGR of 5.80%.