Spinal Fusion Devices Market Summary

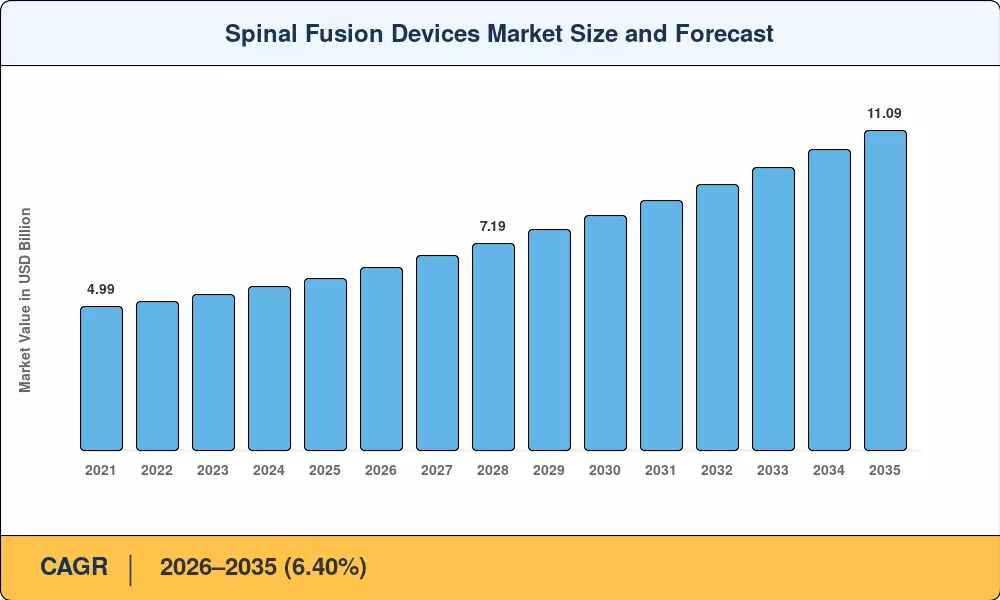

The Global Spinal Fusion Devices Market size was valued at USD 5.97 Billion in 2025, and the market is projected to grow from USD 6.35 Billion in 2026 to USD 11.09 Billion by 2035, registering a CAGR of 6.40% during the forecast period 2026–2035. Rising prevalence of degenerative disc disease across aging populations — combined with expanded Medicare reimbursement for outpatient fusion procedures — has created a durable demand floor that is unlikely to soften before 2030. CMS approval of more than a dozen new outpatient fusion DRG codes since 2021 [1] has accelerated case-mix migration from inpatient hospitals to ambulatory surgery centers, pulling volume growth and device procurement forward simultaneously.

The spinal fusion devices market is undergoing a technological transformation, transitioning from commodity hardware to precision-engineered, patient-specific solutions. 3-D-printed porous titanium and PEEK cages, which are developed using AI-driven surgical planning software, are replacing traditional titanium rod-and-screw assemblies. Robotic-assisted placement platforms, which have now achieved a pedicle screw accuracy of over 96% [2], have garnered over USD 1.8 billion in cumulative venture and strategic investment since 2020 [3]. Additionally, the FDA has approved seven novel robotic spine systems between 2023 and 2025.

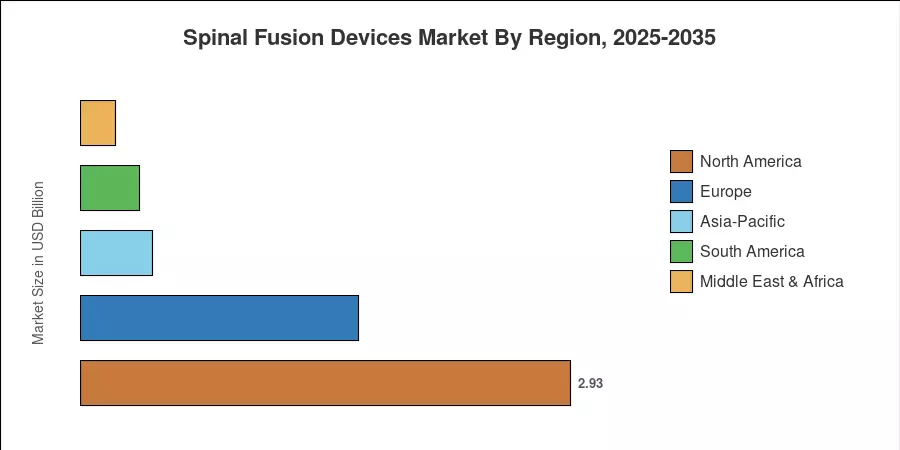

High procedural reimbursement rates and a dense surgeon-training infrastructure have enabled North America to control approximately 49.1% of the global spinal fusion devices market. Driven by the expansion of health insurance coverage in China and India, the Asia-Pacific region is the fastest-growing geography, with a compound annual growth rate (CAGR) of 7.19%. Germany and the United Kingdom are the market leaders in device adoption, with Europe holding the second-largest proportion at approximately 27.8%. The next decade will be determined by the extent to which value-based bundled payment models can compress average selling prices at a quicker rate than volume growth and innovation premiums can compensate.

Key Report Takeaways — Spinal Fusion Devices Market

By Product Type

- Lumbar fusion devices captured 46.0% of the spinal fusion devices market in 2025, reflecting the outsized burden of lower-back degenerative conditions among adults over 50.

- Interbody cages represent the fastest-growing product category, expanding at a 7.28% CAGR through 2035, propelled by surgeon preference for stand-alone cage designs that reduce operative time.

By Surgery Type

- Minimally invasive spine surgery accounted for 66.4% of the spinal fusion devices market revenue in 2025, as robotic navigation platforms lower complication rates and shorten hospital stays.

- Open spine surgery is declining in share but remains clinically indispensable for multi-level deformity corrections and complex revision cases.

By Region

- North America retained the largest regional position with 49.1% of the spinal fusion devices market, supported by favorable payer economics and a mature ASC infrastructure.

- Asia-Pacific is on pace for a 7.19% CAGR to 2035, led by government-backed hospital construction programs in China and rising medical tourism volumes in India and Thailand.

Spinal Fusion Devices Market Size and Forecast (2021–2035)

Market Research Future's estimates combine primary interviews with orthopedic spine surgeons, purchasing directors at hospital networks, and device manufacturer executives, triangulated against publicly filed revenue data and FDA 510(k)/PMA clearance databases. Historical figures (2021–2024) are derived from audited company filings, while forecast values (2026–2035) apply a constant 6.40% CAGR anchored to the validated 2025 base year.