Steam Turbine Market Summary

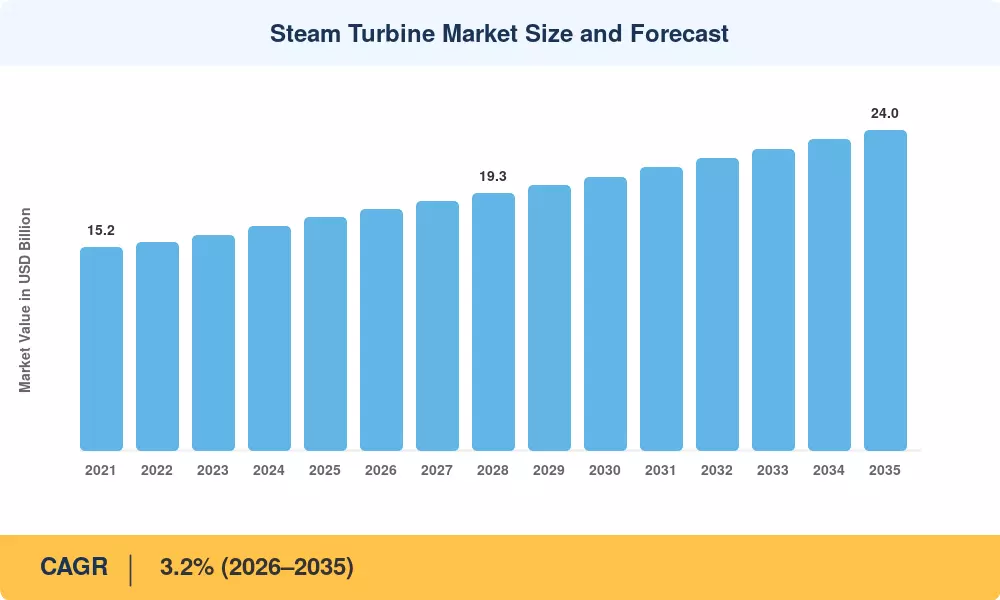

The global Steam Turbine Market reached an estimated USD 17.5 billion in 2025 and is projected to grow from USD 18.1 billion in 2026 to USD 24.0 billion by 2035, registering a CAGR of 3.2% during the forecast period (2026–2035). This growth trajectory reflects the dual pull of coal-to-gas fleet transitions in mature economies and accelerating thermal capacity additions across emerging Asia. The IEA's World Energy Outlook 2024 flagged over 680 GW of planned coal retirements by 2040, each requiring replacement dispatchable capacity — a pipeline that feeds directly into steam turbine demand [1].

Technologically, the Steam Turbine Market is transitioning through a generational shift. The backbone of 20th-century power generation – subcritical units – is being replaced by ultra-supercritical and advanced ultra-supercritical designs, running at steam temperatures >600°C and boosting net plant efficiency above 47%. GE Vernova and Siemens Energy have committed more than USD 2.8 billion for enhanced steam-path R&D until 2030 [2]. Close to 60% of all new orders for gas-fired capacity globally are now for combined-cycle gas turbine (CCGT) plants, which use the exhaust heat to drive a steam turbine [3].

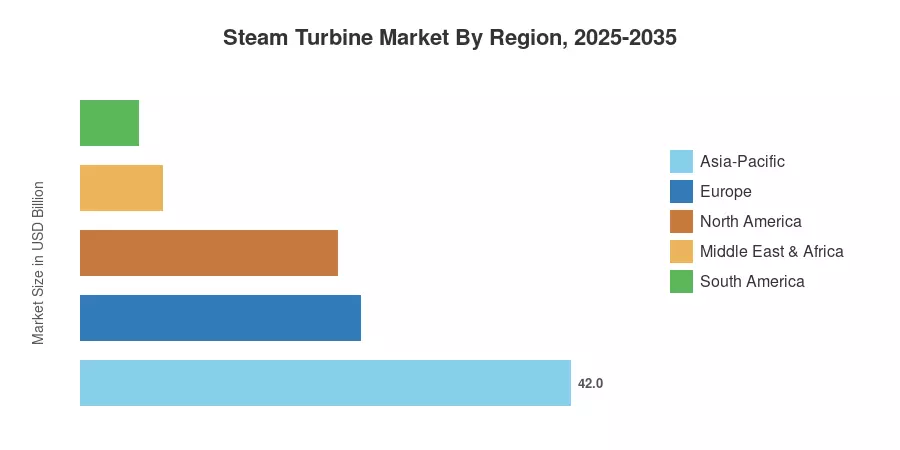

Asia-Pacific accounts for around 42% of the Steam Turbine Market, led by coal fleet upgrades in China and India, and LNG-based expansions in SE Asia. The region is also anticipated to witness the highest CAGR of 4.1% through 2035. Europe is estimated to have a 24% share backed by fleet life-extension programs and cogeneration obligations under the EU Energy Efficiency Directive. North America is at about 22% share and benefits from the clean-energy tax incentives from the Inflation Reduction Act that stimulate CCGT conversions

.

Key Report Takeaways

• By Technology

- Combined-cycle configurations represent the largest revenue segment of the Steam Turbine Market, capturing roughly 48% share in 2025, as utilities pair gas turbines with heat-recovery steam generators.

- Cogeneration/CHP installations are the fastest-growing technology segment, expanding at an estimated CAGR of 4.5% through 2035.

- Conventional steam-cycle units contribute an estimated USD 6.3 billion in 2025 revenue, supported by coal-fired fleet maintenance in Asia.

• By End User

- The power-and-utility sector dominates the Steam Turbine Market with approximately 68% share, reflecting base-load and peaking plant demand.

- Industrial end users — petrochemical, pulp-and-paper, steel — are growing at roughly 3.8% CAGR, driven by on-site power and process-heat requirements.

• By Geography

- Asia-Pacific leads all regions with an estimated USD 7.35 billion in 2025 revenue.

- North America's Steam Turbine Market is projected to grow at 2.8% CAGR as CCGT conversions accelerate under federal incentives.

- Fleet refurbishment programs and district-heating expansion sustain Europe's share of approximately 24%.

Steam Turbine Market Size and Forecast (2021–2035)

Market sizing relies on a bottom-up methodology integrating OEM shipment data, utility CAPEX filings, customs trade databases, and validated third-party estimates from EPRI and IEA. Historical figures (2021–2024) draw on reported revenues; the base year (2025) reflects preliminary shipment trackers; and the forecast period (2026–2035) applies segment-level growth modelling tied to capacity addition pipelines and fleet retirement schedules.