Stevia Market Summary

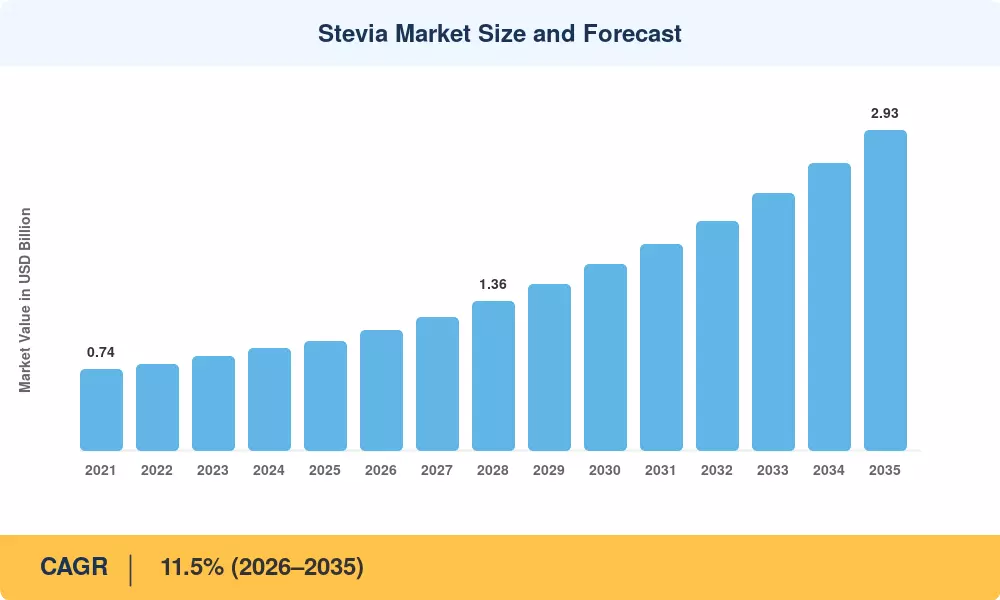

The global Stevia Market was valued at USD 1.00 billion in 2025 and is projected to reach USD 1.10 billion in 2026 before climbing to USD 2.93 billion by 2035, registering a CAGR of 11.5% during the 2026–2035 forecast period. This acceleration stems from tightening sugar taxes across more than 50 countries and a decisive consumer pivot toward low-glycemic ingredients in packaged food and beverages. Government health agencies in North America and Europe have expanded approved daily intake thresholds for high-purity steviol glycosides, giving manufacturers broader formulation latitude and fueling product launches at a pace not seen five years ago [1].

The Stevia Market is experiencing a technology shift as biotech fermentation is replacing traditional leaf extraction for premium glycoside fractions such as Reb M and Reb D. Fermentation-derived stevia now costs around 35-40% less per kilogram than field-extracted equivalents at comparable purity, according to industry estimates from the International Sweetener Consortium [2]. This cost advantage is drawing beverage corporations Coca-Cola, PepsiCo, Nestlé deeper into stevia-sweetened reformulations, with aggregate committed procurement surpassing USD 280 million through 2028 [3].

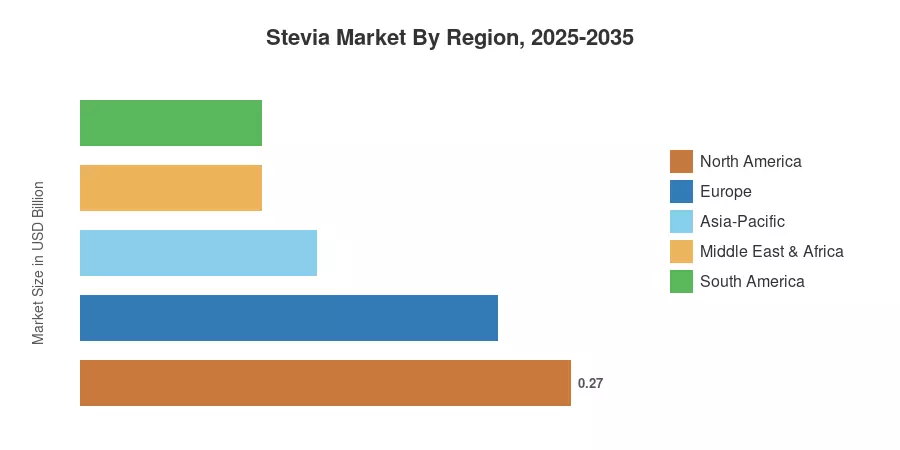

Asia-Pacific leads the Stevia Market, accounting for over 33% of the worldwide revenue, owing to the presence of China’s vertically integrated extraction capacity and Japan’s long-established regulatory acceptability. The region is also observing the highest CAGR at 12.9% to 2035. North America is the second-largest share at about 27%, supported by the FDA GRAS confirmations and active clean-label positioning by CPG brands. As fermentation scaling and taste-masking technologies improve, the Stevia Market is poised for a decade of compounded growth that will change the way the food sector thinks about sweetness.

Key Report Takeaways

• By Format

- Powder formats commanded the leading share of the Stevia Market in 2025, accounting for roughly 90% of global revenue.

- Liquid stevia formats are forecast to expand at a CAGR of 13.3% through 2035, driven by solubility innovations targeting ready-to-drink applications.

• By Ingredient Type

- Conventional stevia held approximately 84% of the Stevia Market in 2025, underpinned by cost efficiency and established supply chains.

- Organic stevia is positioned to grow at a CAGR of 12.1% over the forecast period as clean-label demand intensifies.

• By Application

- Beverages captured the largest application share in the Stevia Market at roughly 32% in 2025.

- Dairy applications are projected to register a CAGR of 11.8% through 2035, reflecting reformulation trends in yogurt and flavored milk.

• By Geography

- Asia-Pacific led the Stevia Market with a 33% share in 2025.

- South America is emerging as a high-growth corridor, expanding at a CAGR of 10.8% as domestic cultivation programs accelerate.

Stevia Market Size and Forecast (2021–2035)

Market Research Future (MRFR) uses a triangulated technique to estimate the market size. This includes supply side production quantities of stevia across major stevia producing countries and demand side consumption audit over 40 countries. MRFR’s patented trade flow model is also a part of the triangulation process. Historical values (2021–2024) are based on customs data and producer-level financial disclosures, while future values (2026–2035) are scenario-weighted growth assumptions tested against macroeconomic and regulatory inputs.

.webp?v=1783952227)