Submarine Market Summary

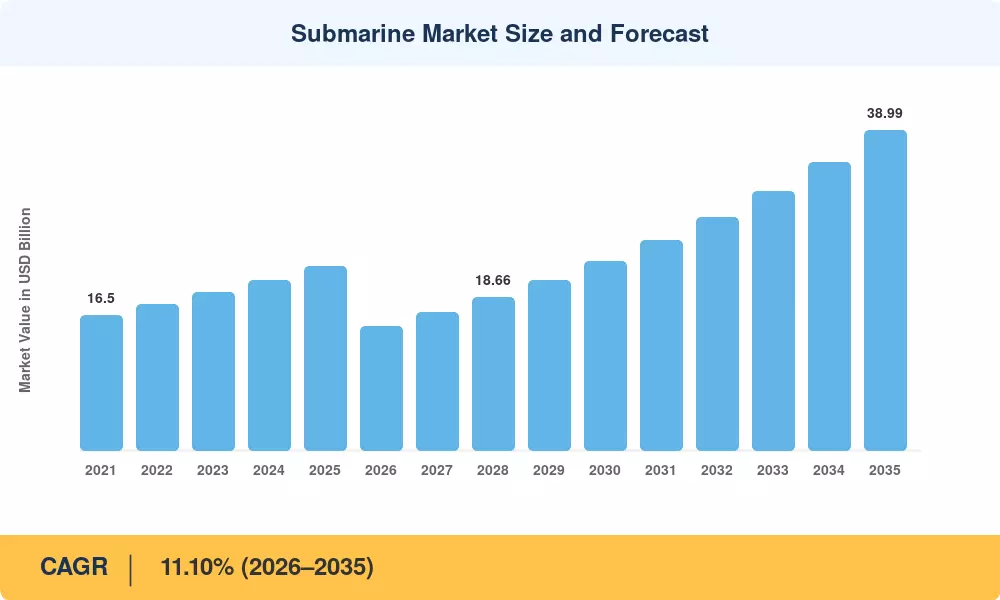

The global Submarine Market reached USD 22.46 billion in 2025, a figure inflated by several concentrated multi-hull contract awards across NATO and Indo-Pacific navies. As procurement cycles recalibrate in 2026, the market resets to an estimated USD 15.12 billion before climbing to USD 38.99 billion by 2035 at a compound annual growth rate of 11.10%. Two structural forces anchor this trajectory: parallel deterrence-renewal programs — Columbia-class in the United States, Barracuda-class in France, Type 212CD across Northern Europe — and a broadening policy consensus that subsea cable protection is critical infrastructure, not optional capability [1].

The technology space is changing in a big way. Short endurance traditional diesel-electric platforms are being replaced with air-independent propulsion versions and lithium-ion battery setups that double the duration of submerged patrols. Nuclear programs, by contrast, are seeing record investment with the U.S. Department of Defense requesting over USD 27.8 billion for submarine combatants within its FY2026 purchase budget alone [1]. France and the United Kingdom are running parallel nuclear-powered boat initiatives that will carry their construction pipelines into the 2030s.

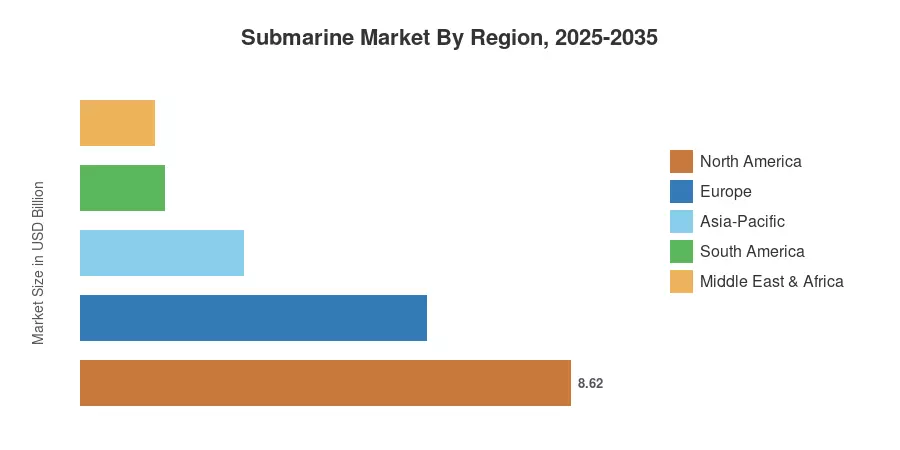

Columbia- and Virginia-class building helps North America to capture around 38.4% of the Submarine Market share by revenue. The Asia-Pacific is the quickest expanding region, with a predicted CAGR of 12.80%, on account of fleet augmentation in India, South Korea and Australia via the AUKUS trilateral pact. Europe has a share of about 27.1%, anchored by Franco-German and Scandinavian naval modernization. The pace at which these overlapping build cycles will translate budget commitments into produced hulls will shape the next decade.

Key Report Takeaways

• By Propulsion Type

- Diesel-electric platforms accounted for 51.2% of the Submarine Market in 2025, reflecting broad conventional fleet demand across mid-tier navies.

- Nuclear-powered submarines are projected to grow at a 13.10% CAGR through 2035, underpinned by U.S., UK, French, and Australian programs.

• By Combat Role

- Attack submarines represented 52.5% of the Submarine Market in 2025, driven by anti-submarine warfare and sea-denial mission requirements.

- Ballistic-missile submarines are forecast to expand at a 12.10% CAGR as nuclear triad renewal programs accelerate.

• By Displacement Class

- The 2,000-to-4,000-ton class captured 42.3% of the Submarine Market in 2025, the preferred displacement band for littoral and regional patrol missions.

• By Component

- Hull and structural modules led with 34.8% revenue share in 2025, while combat and electronic systems represent the fastest-growing component segment.

• By Region

- North America dominated the Submarine Market with 38.4% share in 2025.

- Asia-Pacific is projected as the fastest-growing region at a 12.80% CAGR through 2035.

Submarine Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on verified defense procurement databases, government budget submissions, shipyard order-book disclosures, and triangulated industry interviews. Historical values (2021–2024) reflect actual contract commitments adjusted for delivery timing; forecast values (2026–2035) apply the calibrated CAGR from the reset 2026 base.

.webp?v=1783077067)