Succinic Acid Market Summary

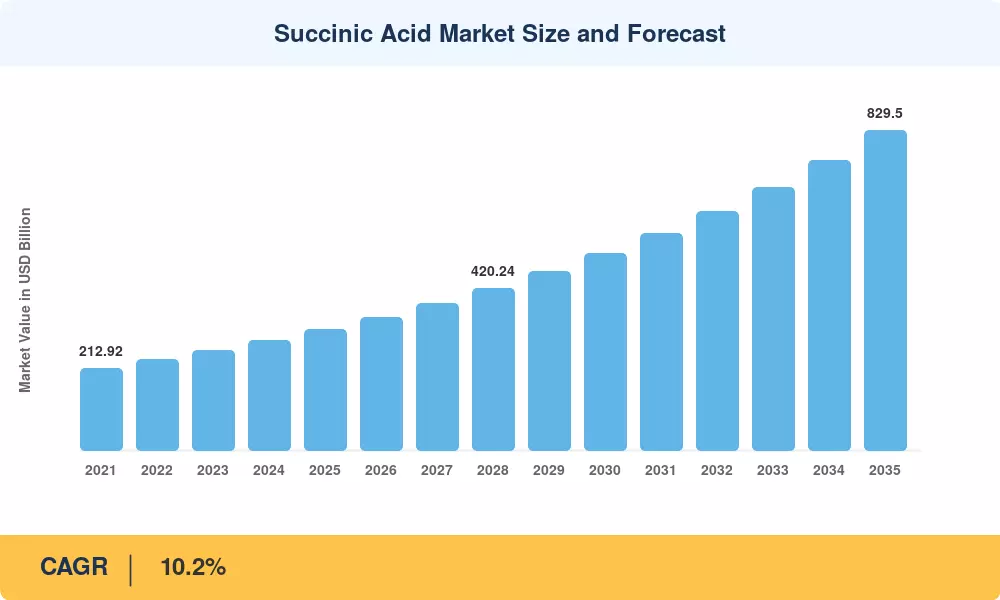

The Succinic Acid Market reached an estimated USD 314.0 Million in 2025 and is projected to climb from USD 346.0 Million in 2026 to USD 829.5 Million by 2035, registering a CAGR of 10.2% over the forecast period. This growth trajectory is anchored in the accelerating shift from petroleum-derived feedstocks toward bio based chemicals, fueled by tightening regulations on carbon-intensive manufacturing across the EU and North America. Corporate sustainability pledges and government-backed green procurement mandates are channeling investment into renewable chemical intermediates at an unprecedented pace[2].

The market for succinic acid is changing due to a fundamental shift in technology. Advanced fermentation-based chemical platforms that produce high-purity succinic acid from renewable sugars are gradually replacing legacy petrochemical synthesis approaches, which are based on the hydrogenation of maleic anhydride. Since 2022, the European Commission's Circular Economy Action Plan has allocated more than EUR 1.2 billion for research and development of green chemical compounds and biodegradable polymer materials, while the US Department of Energy's BioEnergy Technologies Office has set aside USD 180 million for industrial biochemicals scale-up grants in 2024 [3][4].

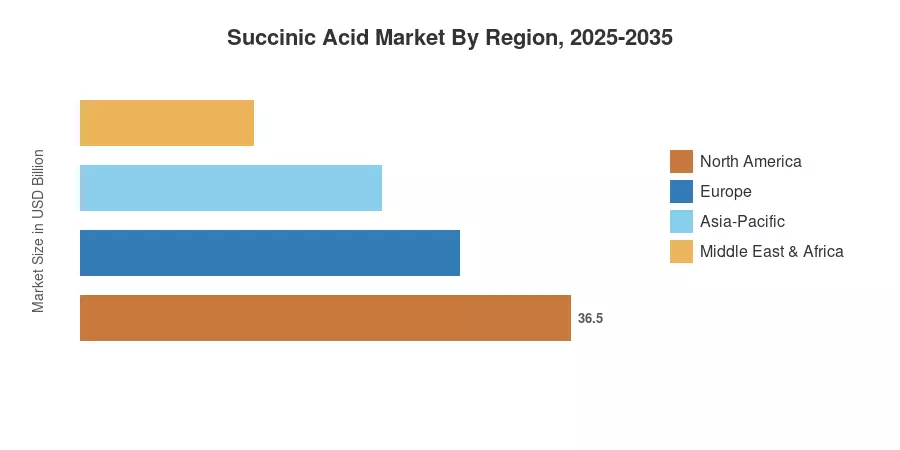

Due to its extensive network of specialized organic acid producers and well-established regulatory framework, Europe accounts for approximately 29.2% of the worldwide succinic acid market's sales. With a projected 11.1% CAGR through 2035, Asia-Pacific is the fastest-growing market thanks to additional fermentation capacity in China and India. Due to the high demand for chemical synthesis intermediates in packaging and automotive end uses, North America has the second-largest share, at around 26.5%. As sustainable polymer materials become more widely accepted in consumer and industrial supply chains, the next ten years should see faster adoption.

Key Report Takeaways

• By Product Type

- Petro-based succinic acid production accounted for approximately 54% of the Succinic Acid Market in 2025, reflecting entrenched petrochemical infrastructure.

- Bio-based production is forecast to expand at roughly 11.8% CAGR during 2026–2035, propelled by declining fermentation costs and corporate decarbonization targets.

• By Grade

- Industrial/technical grade represented about 33% of the Succinic Acid Market size in 2025, serving demand for chemical synthesis intermediates in plasticizers and coatings.

- Cosmetic grade is projected to grow at approximately 11.3% CAGR through 2035, driven by clean-beauty formulations using specialty organic acids.

• By Application

- Industrial chemicals held roughly USD 86.4 Million of the Succinic Acid Market in 2025, underscoring its role as a foundational renewable chemical intermediates platform.

- Personal care and cosmetics are advancing at an estimated 10.9% CAGR, reflecting rising consumer preference for eco-friendly chemical products.

• By Region

- Europe commanded approximately 29.2% of the Succinic Acid Market in 2025, supported by regulatory incentives for green chemical compounds.

- Asia-Pacific is set to register the fastest CAGR of 11.1% between 2026 and 2035, as China and India scale fermentation-based chemicals capacity.

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue analysis across 45+ countries with top-down validation using trade databases, company filings, and proprietary demand models. Historical figures (2021–2024) reflect audited industry data; the forecast (2026–2035) applies segment-level CAGRs calibrated against macroeconomic and regulatory scenarios.