Surgical Lights Market Summary

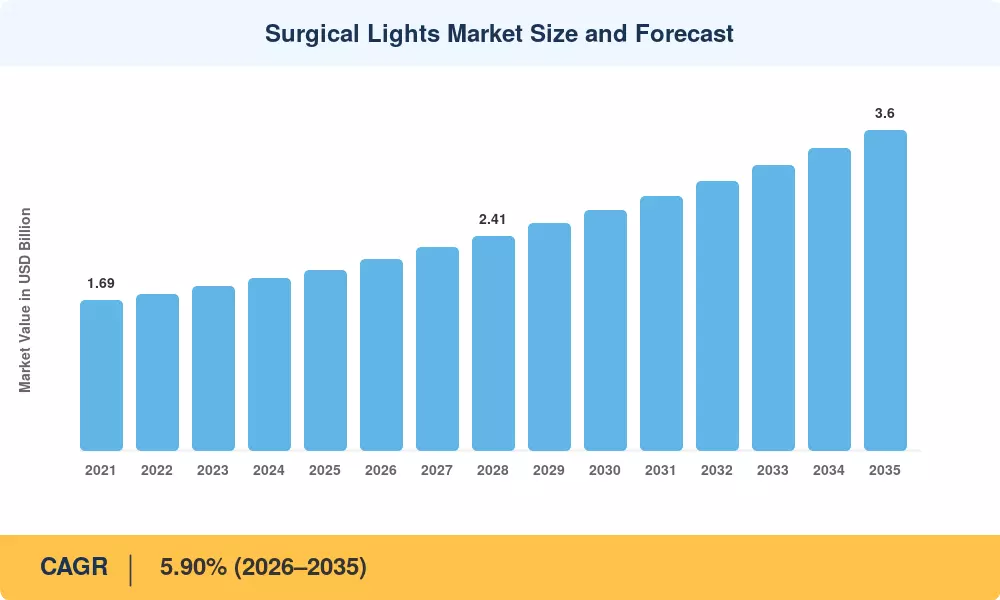

The Global Surgical Lights Market size was valued at USD 2.03 Billion in 2025, and the market is projected to grow from USD 2.15 Billion in 2026 to USD 3.60 Billion by 2035, registering a CAGR of 5.90% during the forecast period 2026–2035. Government capital programs targeting hospital infrastructure modernization — including the U.S. HRSA Community Health Center expansions and the EU4Health Programme allocating over EUR 5.3 billion for healthcare facility upgrades — have created sustained procurement demand that anchors this growth trajectory [1][2].

A generational technology shift defines this decade for the Surgical Lights Market. Legacy halogen luminaires, once standard in over 70% of installed surgical suites globally, are giving way to LED-based systems that deliver superior color rendering indices above 95 Ra, consume up to 60% less electricity, and generate minimal radiant heat in the sterile field. The World Health Organization's 2023 guidance on mercury-containing medical devices has accelerated phase-out timelines across 48 member states, driving a replacement cycle worth an estimated USD 420 million annually through 2030 [3][4].

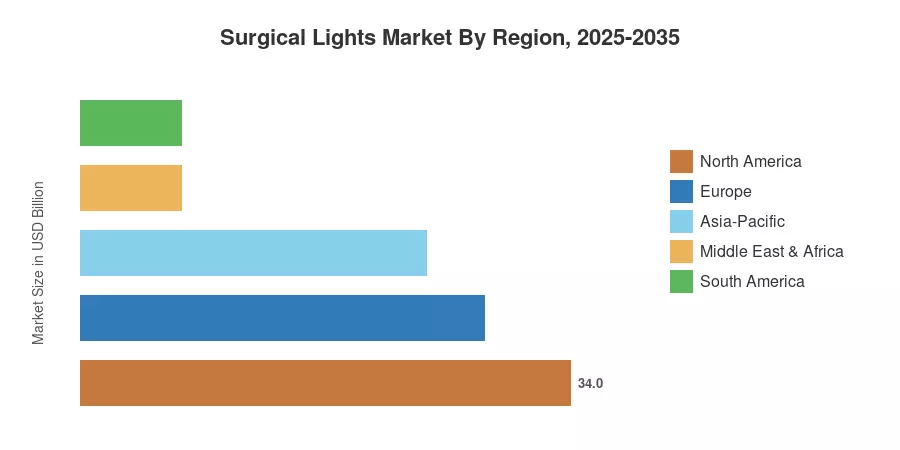

North America commands roughly 34% of revenue in the Surgical Lights Market, anchored by the concentration of hybrid operating suites across the United States. Asia-Pacific is the fastest-growing region with a projected CAGR of 8.66% through 2035, driven by large-scale hospital construction in India and China. Europe holds the second-largest share at approximately 28%, where sustainability mandates under the EU Medical Device Regulation continue to push the adoption of energy-efficient luminaires. The next decade will hinge on how quickly AI-enabled lighting calibration and 4K-integrated surgical visualization reshape procurement priorities worldwide.

Key Report Takeaways

• By Type

- LED lights captured approximately 57% of the Surgical Lights Market in 2025, supported by superior longevity, low thermal emission, and regulatory mandates phasing out mercury-based alternatives.

- Halogen lights continue to serve cost-sensitive facilities in developing economies, though their share is contracting as LED price premiums narrow below 15%.

• By Application

- Cardiac surgery procedures accounted for roughly 20% of the market share in 2025, reflecting the complexity and volume of cardiovascular interventions globally.

- Gynecological surgery is the fastest-growing application segment.

• By End User

- Ambulatory surgical centers represent the fastest-growing end-user segment, posting a CAGR of 8.28% through 2035 as outpatient procedure volumes climb.

- ASCs represent the most dynamic growth vector, with U.S. facility counts alone projected to exceed 7,000 by 2030 as payers and health systems shift eligible procedures to lower-cost outpatient settings.

• By Region

- North America generated an estimated USD 0.69 billion in Surgical Lights Market revenue during 2025, led by U.S. hospital system capital expenditures.

- Asia-Pacific is projected to expand at an 8.66% CAGR through 2035, fueled by government-backed healthcare infrastructure programs across India, China, and Southeast Asia.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary sizing framework triangulates bottom-up equipment shipment tracking, top-down healthcare capital expenditure analysis, and validated distributor channel data across 32 countries. Historical figures reflect audited data through 2024; the 2025 base year combines preliminary shipment records with facility commissioning databases.