Surgical Site Infection Control Market Summary

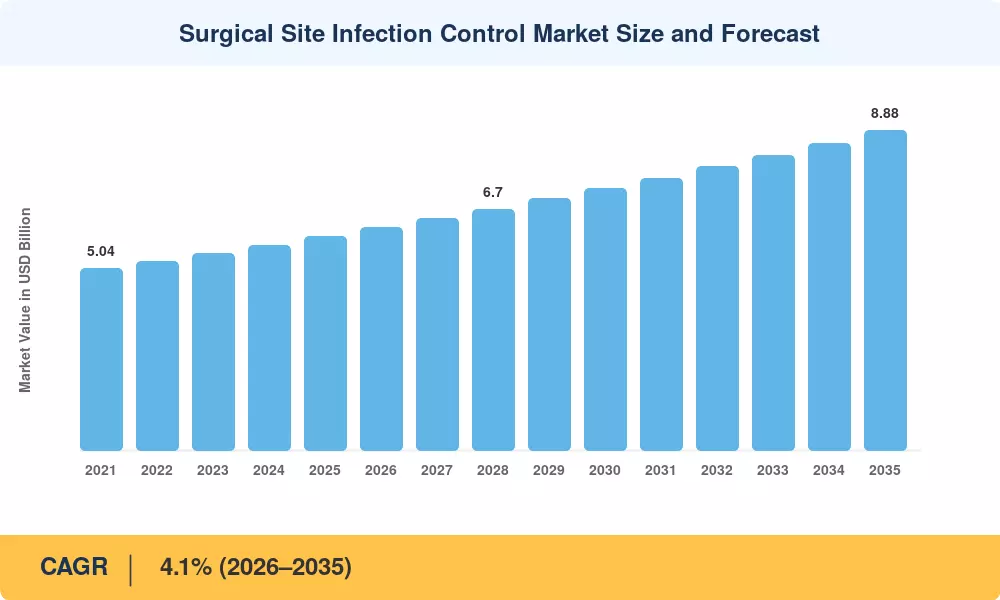

The Global Surgical Site Infection Control Market size was valued at USD 5.94 Billion in 2025, and the market is projected to grow from USD 6.18 Billion in 2026 to USD 8.88 Billion by 2035, registering a CAGR of 4.1% during the forecast period 2026–2035. This growth trajectory reflects intensifying global attention toward post-op wound infection prevention, spurred by tightened hospital accreditation standards and expanded government funding for healthcare-associated infection (HAI) surveillance programs. The U.S. Centers for Medicare & Medicaid Services (CMS) penalty framework — which withholds up to 1% of reimbursements from hospitals with elevated SSI rates — continues to push acute-care facilities toward comprehensive SSI reduction protocols [2].

A measurable technology shift is reshaping the Surgical Site Infection Control Market. Traditional manual reprocessing workflows and basic chlorhexidine scrubs are giving way to closed-loop automated disinfection systems, negative-pressure wound therapy devices, and AI-enabled surgical wound antisepsis monitoring platforms. The WHO's Global Guidelines on SSI Prevention, updated in 2024, allocated an additional USD 120 million in technical assistance for low- and middle-income countries to adopt evidence-based perioperative antibiotic prophylaxis bundles [3]. These mandates are accelerating procurement cycles for advanced sterile surgical field maintenance technologies across both public and private hospital networks.

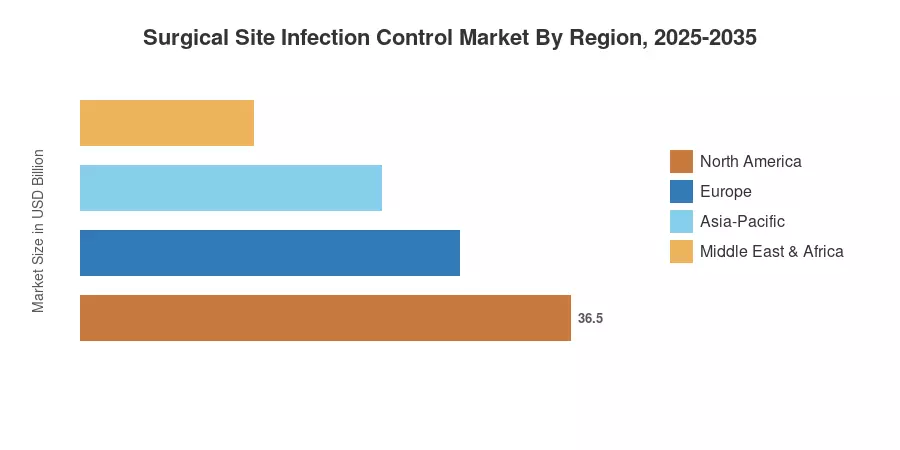

North America commands approximately 38% of the global Surgical Site Infection Control Market, anchored by robust payer incentive programs and high surgical volumes exceeding 50 million procedures annually [4]. Asia-Pacific stands as the fastest-growing region with an estimated CAGR of 5.3%, propelled by rising surgical caseloads in China and India and expanding hospital infrastructure investments. Europe holds the second-largest share at roughly 28%, driven by stringent EU medical device regulations and cross-border HAI reporting frameworks. The decade ahead will be defined by digital integration, reimbursement-linked quality metrics, and broader adoption of SSI reduction protocols in emerging economies.

Key Report Takeaways

• By Product

- Disinfectants account for the largest revenue share in the Surgical Site Infection Control Market, driven by universal demand for surgical wound antisepsis across all facility types

- Manual reprocessors solutions are growing at a CAGR of 3.6%, supported by cost-effective sterile surgical field maintenance in ambulatory surgical centers

- Antimicrobial sutures and wound-closure devices represent a USD 1.12 Billion segment, reflecting surgical teams' preference for built-in post-op wound infection prevention

• By Surgery/Procedure

- Cesarean section procedures hold the highest segment share in the Surgical Site Infection Control Market, given the sheer global volume — over 32 million C-sections annually — and corresponding perioperative antibiotic prophylaxis requirements

- Orthopedic surgery SSI prevention is expanding at the fastest pace, fueled by rising joint-replacement volumes among aging populations

• By Region

- North America leads the Surgical Site Infection Control Market with approximately 38% share, driven by CMS HAI penalty programs and high per-capita healthcare expenditure

- Asia-Pacific is forecast to register a CAGR of 5.3% through 2035, as governments invest in hospital infection-control infrastructure

- Europe accounts for roughly USD 1.66 Billion in 2025, supported by mandatory SSI reduction protocols under EU cross-border health directives

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue analysis from over 200 device manufacturers and distributors, triangulated with top-down macroeconomic indicators including global surgical volumes, hospital bed density, and infection-control budget allocation patterns from 45 countries. Historical data reflects actual reported revenues; forecast values apply a calibrated compound annual growth rate anchored to demonstrated adoption curves for perioperative antibiotic prophylaxis and sterile surgical field maintenance technologies.

.webp?v=1782976095)