Sustainable Aviation Fuel Market Summary

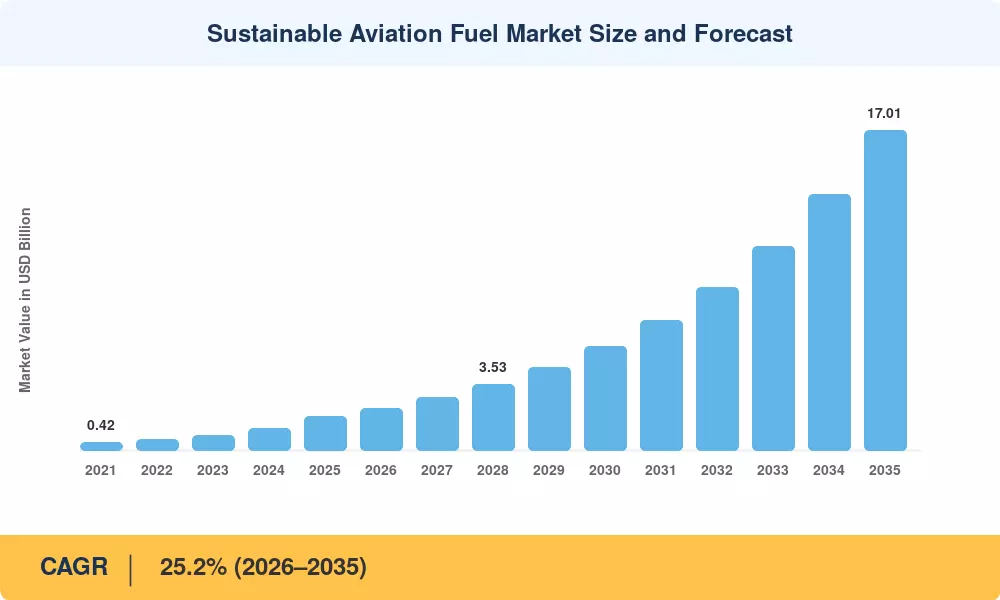

The Sustainable Aviation Fuel Market reached an estimated USD 1.80 billion in 2025 and is projected to grow from USD 2.25 billion in 2026 to USD 17.01 billion by 2035, registering a CAGR of 25.2% during the forecast period (2026–2035). Two catalysts are reshaping this trajectory: the European Union's ReFuelEU Aviation regulation, which mandates minimum SAF blending ratios starting at 2% in 2025 and escalating to 70% by 2050, and the U.S. Inflation Reduction Act's SAF tax credit of up to USD 1.75 per gallon for fuels achieving at least a 50% lifecycle emissions reduction [1][2].

A fundamental technology transition is underway. Conventional petroleum-derived jet fuel — the industry's near-exclusive energy source for seven decades — faces displacement by hydroprocessed esters and fatty acids pathways, gasification-based Fischer-Tropsch synthesis, and emerging electrochemical routes. Global airlines committed over USD 35 billion in SAF offtake agreements between 2022 and 2025, signaling that demand-side pull has shifted from voluntary pledges to binding procurement contracts [3][4].

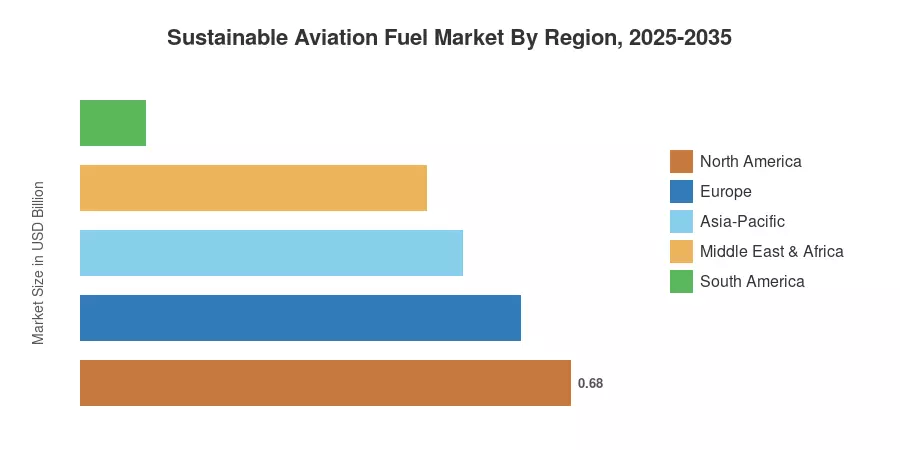

North America commands approximately 38% of the Sustainable Aviation Fuel Market, anchored by refinery conversions in the U.S. Gulf Coast and West Coast corridors. Asia-Pacific is the fastest-growing region with an estimated CAGR of 29.5%, propelled by Japan's Green Transformation (GX) bonds and India's draft SAF policy. Europe holds roughly a 34% share, driven by regulatory certainty from the EU Emissions Trading System's aviation scope expansion. By 2030, the Sustainable Aviation Fuel Market will likely see production capacity exceed 10 million metric tons per year as new biorefineries and power-to-liquid facilities reach commercial scale [5][6].

Key Report Takeaways

• By Technology

- HEFA pathways account for approximately 62% of the Sustainable Aviation Fuel Market in 2025, reflecting mature refining infrastructure and feedstock availability.

- Fischer-Tropsch synthesis is growing at a CAGR of roughly 31.4% through 2035, driven by municipal solid waste gasification projects.

- Power-to-liquid routes, while holding the smallest share today, attracted over USD 4.2 billion in announced project investments between 2023 and 2025.

• By End User

- Commercial aviation represents USD 1.30 billion in 2025 demand, the largest application segment within the Sustainable Aviation Fuel Market.

- Military aviation programs, including the U.S. Department of Defense's operational energy strategy, are expanding SAF procurement at an estimated CAGR of 28.3%.

• By Region

- North America leads the Sustainable Aviation Fuel Market with a 38% share in 2025, underpinned by production tax credits and refinery conversion investments.

- Asia-Pacific is set to exceed USD 4.8 billion by 2035, driven by national decarbonization roadmaps across Japan, South Korea, and India.

Market Size and Forecast (2021–2035)

Market sizing combines bottom-up production capacity tracking with top-down demand modeling from ICAO, IATA, and national aviation authority databases. Historical figures (2021–2024) reflect verified SAF production volumes and average delivered prices. Forecast projections (2026–2035) integrate announced capacity expansions, policy-driven blending mandates, and feedstock supply curve analysis [7][8].