Telecom API Market Summary

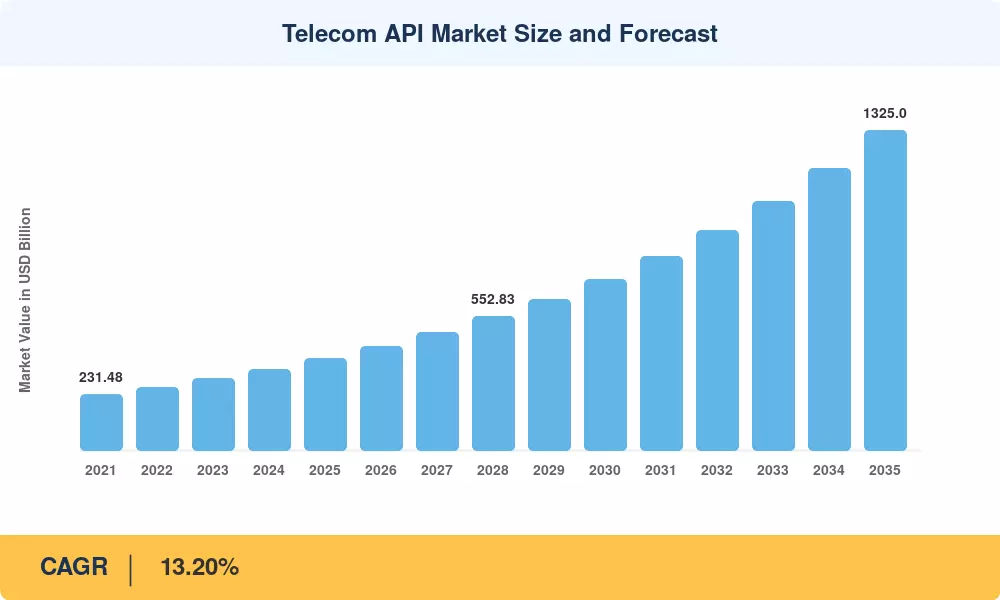

The Telecom API Market stood at USD 380.10 billion in 2025 and is forecast to reach USD 434.10 billion in 2026 before climbing to USD 1,325.00 billion by 2035 at a compound annual growth rate of 13.20% across the forecast window. This expansion is anchored by the GSMA Open Gateway initiative, which now federates CAMARA-compliant interfaces across more than 280 networks, and by aggressive 5G standalone rollouts that have unlocked programmable quality-of-service and network-slicing capabilities for third-party developers [1]. Regulatory mandates in the EU Digital Markets Act and India's TRAI open-access framework have accelerated carrier willingness to expose network functions through standardized endpoints [2].

A structural shift is underway as operators retire bespoke, point-to-point integrations in favor of platform business models that package location verification, carrier billing, number verification, and messaging as developer-ready services. Cumulative operator investment in API gateway infrastructure is projected to exceed USD 28 billion between 2024 and 2028, according to estimates, signaling a decisive move from connectivity-only revenue streams toward programmable network monetization.

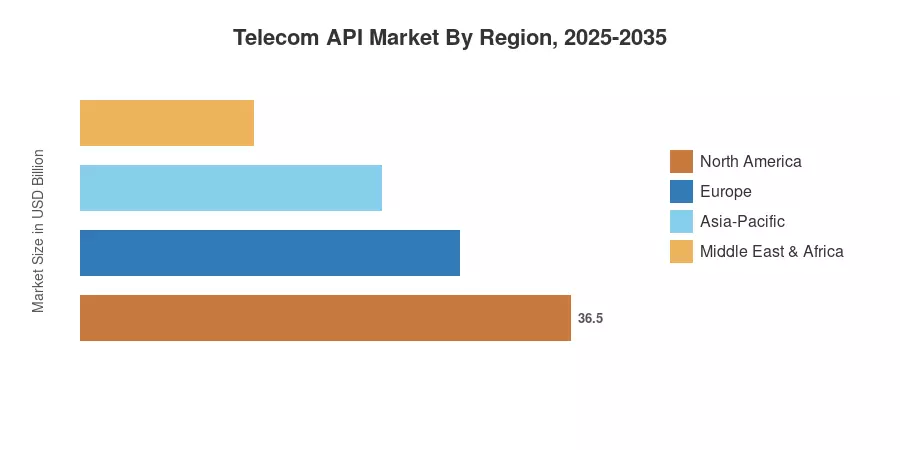

North America retained its position as the dominant region in the Telecom API Market in 2025, accounting for roughly 34% of global revenue, driven by mature CPaaS ecosystems and hyperscaler partnerships. Asia-Pacific is the fastest-growing region with a projected CAGR of 14.80%, fueled by Reliance Jio, China Mobile, and SoftBank exposing edge-computing and slicing APIs to their massive 5G subscriber bases. Europe held the second-largest share at approximately 26%, propelled by EU open-network regulations and the region's strong fintech-telco convergence. The Telecom API Market is poised to reshape how enterprises consume network intelligence over the coming decade.

Key Report Takeaways

• By Service Type

- Messaging APIs (SMS, MMS, RCS) captured 35.14% of the Telecom API Market in 2025, reflecting the enduring dominance of A2P messaging in authentication and customer engagement workflows.

- Payment APIs are forecast to record the strongest segment CAGR at 13.84% through 2035, driven by telco-fintech convergence and carrier billing adoption in emerging economies.

• By Deployment Type

- Hybrid architectures accounted for 52.84% of the Telecom API Market share in 2025, as operators balanced latency requirements with data-sovereignty constraints.

- Multi-cloud implementations are expanding at a 14.27% CAGR to 2035, gaining traction among operators pursuing vendor-neutral orchestration.

• By End-User

- Partner developers held 35.53% of Telecom API Market revenue in 2025, representing system integrators and ISVs embedding network functions into vertical solutions.

- Long-tail developers are projected to register the highest end-user CAGR at 13.93%, as self-service portals and sandbox environments lower the onboarding barrier.

• By Business Model

- Aggregator-led models commanded 43.45% of the Telecom API Market value in 2025, with platforms like Twilio and Vonage intermediating between carriers and developers.

- API marketplace and exchange architectures are growing fastest at a 14.15% CAGR, reflecting operator interest in direct monetization without intermediary margin erosion.

• By Region

- North America led the Telecom API Market with a 34% revenue share in 2025, anchored by US hyperscaler partnerships and mature enterprise demand.

- Asia-Pacific's 14.80% CAGR positions the region to narrow the gap significantly by 2035.

Telecom API Market Size and Forecast (2021–2035)

Market sizing draws on operator revenue disclosures, CPaaS vendor filings, GSMA intelligence datasets, and proprietary demand-side surveys covering more than 1,200 enterprise API consumers across 42 countries. Historical figures (2021–2024) reflect audited revenue; the base year 2025 is estimated from trailing four-quarter run-rates; and the 2026–2035 forecast applies a calibrated growth model validated against third-party benchmarks.