Thin Film Battery Market Summary

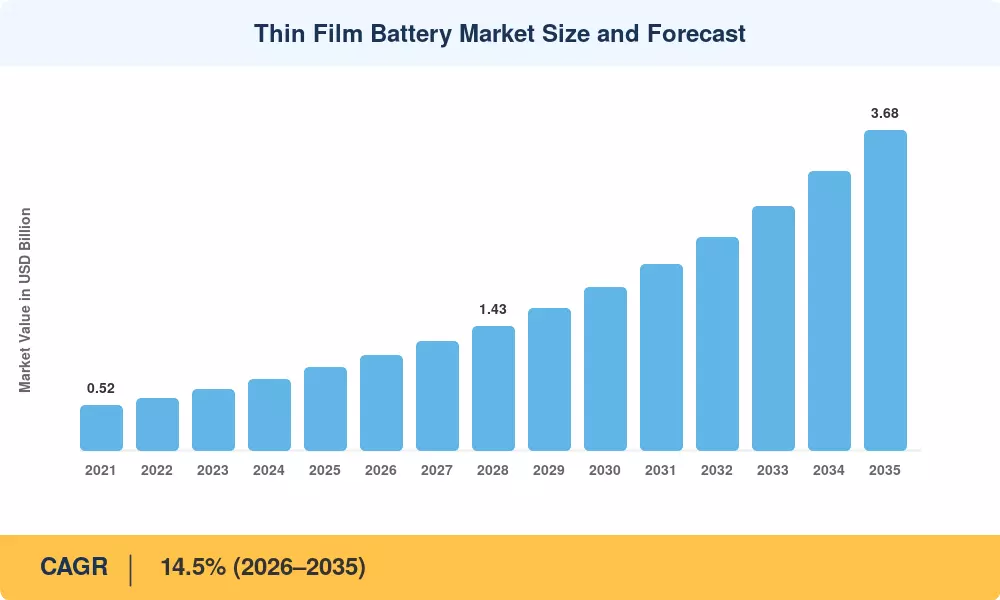

The global Thin Film Battery Market reached an estimated USD 0.95 billion in 2025 and is projected to grow from USD 1.09 billion in 2026 to USD 3.68 billion by 2035, registering a compound annual growth rate of 14.5% over the forecast window. Two catalysts stand behind this trajectory: the U.S. Department of Energy's USD 3.1 billion Advanced Energy Manufacturing initiative, which earmarks funding for next-generation energy storage R&D [1], and the European Commission's Battery Regulation (EU 2023/1542), which tightens sustainability and performance standards across the battery value chain [2]. Together, these policy levers are redirecting capital toward compact, high-density power sources that conventional cylindrical cells cannot serve.

There is a generational change in technology happening. Legacy coin-cell and button-cell batteries were the norm for hearing aids, smart cards and small sensors. They are being replaced by vapor-deposited thin film structures, offering higher energy density per unit area, longer cycle life and better form-factor flexibility. This shift is seen in corporate investment: the total venture and strategic investment into micro-battery startups was over USD 620 million in the 2022-2024 period, according to BloombergNEF tracking data [3].

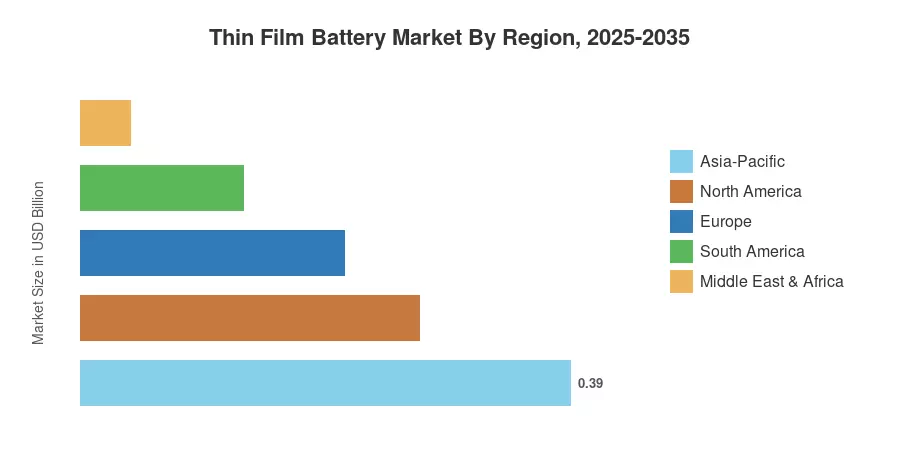

The Asia-Pacific region has around 41% of the thin film battery market due to the semiconductor fabrication facilities in Japan, South Korea and China. North America has 28% share, driven by demand from the defense and medical device sectors. Next is Europe at 22%, with its rapid growth shown in wearable health tech clusters in Germany and the Nordics. Looking to the future, the combination of miniature IoT networks and implantable medical electronics will drive the adoption of thin-film beyond its current niche position.

Key Report Takeaways

• By Battery Type

- Thin-film lithium-ion batteries held approximately 48% of the thin-film battery market in 2025, owing to mature fabrication processes and proven cycle-life performance.

- Thin-film lithium polymer cells are the fastest-growing type, recording a projected CAGR of 16.1% through 2035, fueled by demand for flexible and conformable power sources.

- Zinc-based thin-film chemistries accounted for an estimated USD 90 million in 2025, gaining traction in disposable medical patches.

• By Application

- Wearable electronics represent the fastest-expanding application segment in the Thin Film Battery Market, with a forecast CAGR of 15.8%.

- Medical devices contributed roughly 22% of total revenue in 2025, reflecting adoption in implantable cardiac monitors and drug-delivery patches.

- Smart cards and RFID tags generated an estimated USD 175 million in 2025, supported by contactless payment migration globally.

• By Geography

- Asia-Pacific accounted for 41% of the Thin Film Battery Market value in 2025.

- North America is projected to grow at a CAGR of 13.9% through 2035.

- Europe contributed approximately USD 0.21 billion in 2025.

Thin Film Battery Market Size and Forecast (2021–2035)

Market sizing is derived by a triangulation methodology that includes a bottom-up approach of revenue generated by company filings, a top-down approach of demand by application vertical, and a cross-validation of patent-filing velocity and capacity-expansion announcements tracked by MRFR analysts.