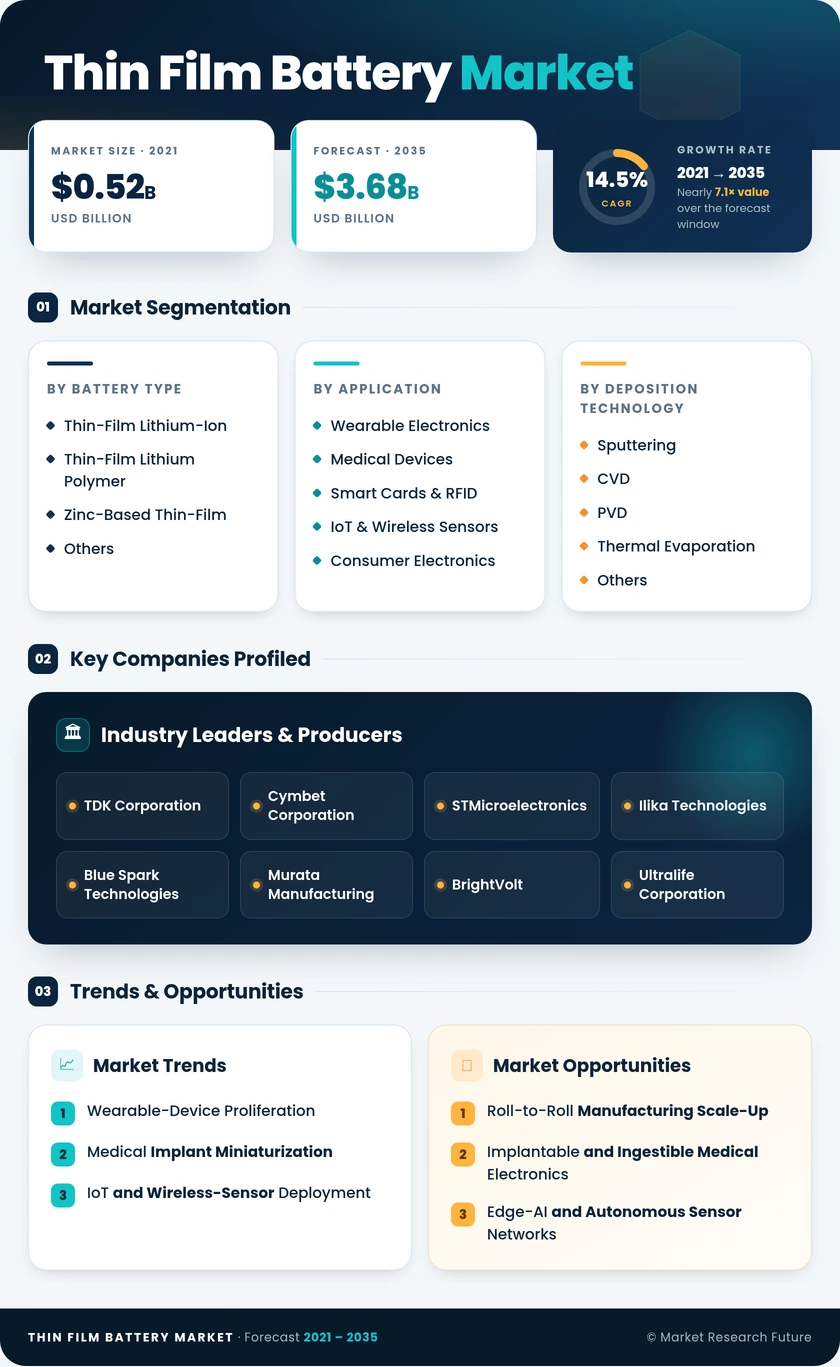

SEGMENTATION QUICK REFERENCE

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| By Battery Type | Thin-Film Lithium-Ion, Thin-Film Lithium Polymer, Zinc-Based Thin-Film, Others | Thin-Film Lithium-Ion (48% share) | Thin-Film Lithium Polymer (CAGR 16.1%) |

| By Application | Wearable Electronics, Thin Film Battery Markets, Smart Cards & RFID, IoT & Wireless Sensors, Consumer Electronics, Others | Thin Film Battery Markets (22% share) | IoT & Wireless Sensors (CAGR 16.4%) |

| By Deposition Technology | Sputtering, CVD, PVD, Thermal Evaporation, Others | Sputtering (52% share) | CVD (CAGR 15.3%) |

MARKET SEGMENTATION OVERVIEW

By Battery Type

| Sub-Segment | Key Trend |

| Thin-Film Lithium-Ion | Mature fabrication; OEM-qualified across smart cards and RFID |

| Thin-Film Lithium Polymer | Flexible substrates enabling curved wearable designs |

| Zinc-Based Thin-Film | Non-toxic, biodegradable profiles for disposable medical patches |

| Others (Solid-State Oxide, NiMH) | Niche industrial and high-temperature sensor applications |

Thin-film lithium-ion cells remain the backbone of the market due to well-established sputtering processes and a broad base of qualified OEM integrations. Lithium polymer variants are closing the gap as roll-to-roll manufacturing matures, especially for wearable and flexible form-factor applications.

By Application

| Sub-Segment | Key Trend |

| Wearable Electronics | Smartwatch and fitness-band miniaturization is demanding sub-mm power sources. |

| Thin Film Battery Markets | Implantable monitors and transdermal patches require biocompatible cells. |

| Smart Cards & RFID | Biometric payment card migration is creating high-volume demand. |

| IoT & Wireless Sensors | Deploy-and-forget networks in agriculture, logistics, and utilities |

| Consumer Electronics | Ultra-thin laptops and earbuds using thin-film backup cells |

| Others | Defense soldier-wearable systems and aerospace sensor modules |

Wearable electronics and IoT sensors are the twin growth engines, each driven by the need for long-lasting, maintenance-free power in constrained physical spaces. Medical devices remain the highest-margin application due to stringent regulatory qualification and premium ASPs.

By Deposition Technology

| Sub-Segment | Key Trend |

| Sputtering | Industry-standard process for uniform electrolyte-layer deposition |

| Chemical Vapor Deposition (CVD) | Scaling for multi-layer architectures and compositionally graded films |

| Physical Vapor Deposition (PVD) | Cost-efficient for simpler electrode structures |

| Thermal Evaporation | Legacy method with declining share |

| Others (ALD, Sol-Gel) | Lab-to-fab transition in progress for next-generation chemistries |

Sputtering dominates because of its proven ability to produce pinhole-free electrolyte films at thicknesses below 1 micrometer. CVD is the most active area of manufacturing R&D, with pilot lines in South Korea and the U.S. demonstrating scalability for compositionally complex cathode and electrolyte stacks.